The Indian Finance Minister has tabled today, the Union General Budget 2021-22 in the Parliament.

One of the key amendments in the Finance Bill 2021 is related to EPF and VPF (Provident Fund) contributions.

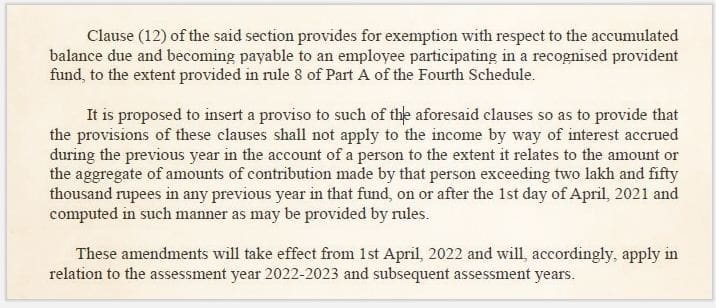

As of now (FY 2020-21), the interest income earned on contributions to EPF made by the employee is completely TAX-FREE.

However, with effective from 1st April, 2021, no more tax free interest on more than Rs 2.5 lakh a year contribution towards EPF/VPF (only employee contribution).

This limit does not include the employer’s contribution. The new rules will also apply to the GPF (General Provident Fund).

Interest on EPF Contributions above Rs 2.5 lakh is Taxable

From 1st April 2021 onwards, the interest on any contribution above Rs. 2.5 lakh by an employee to a recognized provident fund is taxable as per the provisions of the Finance bill 2021.

- If employee contribution is more than Rs 2.5 lakh, the interest earned on the excess amount is taxable wef 1st April 2021 onwards.

- Your past EPF balance as on March 31, 2021 will always remain tax free.

- Example – If employee share EPF + VPF is Rs 4.5 lakh in FY 2021-22 then the interest earned on excess Rs 2 lakh (Rs 4.5 L – Rs 2.5 L) will be taxable in FY 2021-22 / AY 2021-22.

- You will then need to determine the interest amount corresponding to the excess, that is Rs. 2 lakh and declare it as income and pay tax as per applicable income tax slab rate.

- Note that the additional interest on this amount (Rs 2 lakh) in subsequent assessment years may not be taxable. (Let’s wait for more clarity on this aspect)

This new rule will impact the salaried individuals who make large contributions to EPF or VPF account.

Latest News (23-March-2021) : The Central Govt has capped the threshold limit to Rs 5 Lakh for earning tax-free interest on employees contribution to PF. However, it’s meant only for Defense Personnel and few other Govt employees where employer is not contributing into EPF.

The previous Budget 2020 has restricted the tax-exempt superannuation, NPS and EPF account contribution by the employer to maximum of Rs 7.5 lakh in a financial year. Further, any interest or gains earned from the excess contribution is be taxable in the hands of an employee. This amendment is applicable for FY 2020-21 (AY 2021-22) itself.

Latest news (March 2021) : EPF interest rate for 2020-21. The Central Board recommends 8.50 % rate of interest to its subscribers for the year 2020-21. EPFO notifies 8.5% as interest Rate on EPF for the year 2020-21.

The previous FYs EPF interest rates are as below;

- FY 2019-20 : 8.50%

- FY 2018-19 : 8.65%

- FY 2017-18 : 8.55%

- FY 2016-17 : 8.65%

- FY 2015-16 : 8.80%

- FY 2014-15 : 8.75%

- FY 2013-14 : 8.75%

- FY 2012-13 : 8.50%

Continue reading:

- 15 Important Budget 2021 Proposals related to your Personal Finance | W.e.f AY 2022-23

- EPF Interest Income & Withdrawals | Tax Implications | Is EPF Interest taxable?

- Why should you Withdraw Old EPF Account Balance? | In-operative EPF A/c Timeline

- EPF a/c interest calculation : Components & illustration (Employees’ Provident Fund)

(Post first published on : 01-February-2021)

Join our channels

Sir,

My question is

This new rule is applicable from 1st April 2021 onwards, suppose PF+VPF=25000/pm=3L/yr. so excess amount is 50k. Now everywhere i can see 50000*8.5%= Rs.4250(the employee to has to pay tax as per his incometax slab, this i understood. But my question is who will deduct, is it employee itself, will deduct as part of Monthly Tax computation or EPFO itself –> if so, in the same year or next consecutive year). Becoz EPF interest for the previous year is announced in the subsequent year and also interest will be credited in 2022-2023 for PF outstanding till Mar 2022.

Dear Sathiyaraj,

I believe that the formal rules on computation are yet to be issued by the Govt. But initial indications are that taxpayers would need to add the interest accrued every year to their income-tax Statements. Central Board of Direct Taxes (CBDT) chairman Mr. PC Mody has indicated that the interest on excess PF contribution will be taxed like that of bank fixed deposit interest. The interest portion is calculable on a year-to-year basis, and that will go on an accrual basis so that it is taxable on your computation of income in that year.

Suggest you to go through this article….

Hi Sreekanth,

I need suggestion for this issue. i had applied for full pf withdrawal but due to IFSC mismatch got rejected, but consulted my previous organisation to digitally sign bank statement(correct IFSC code). its been already 1 month, they are not signing due to some reason.

i’m unable to contact pf office contact number, their contact not in service and unable to visit pf office due to lock-down. please suggest me how to digitally sign my bank document and PAN through other solutions instead of organisation and apply for pf full withdrawal.

with regards,

Megha

Dear Kasi,

I believe that PPF is not included in this amendment.

Thank you

Hi,

Thank for update.

My question is say if employee contribuation in FY 21-22 is 6 lakh this year then interest on 3.5 Lac will be taxable. Now

“Note that the additional interest on this amount (Rs 2 lakh) in subsequent assessment years is not taxable.”

Now interest earn on this during FY 22-23 is taxable or tax free. My view is its taxable. I think accumulated fund will be seen.

Regards

Dixit Ranka

Dear Dixit,

Let’s wait for more clarity on ‘taxation aspect for subsequent years’..

Dear Sreekanth Reddy,

Thank you for your response to my query dated 2-Feb-2021.

From 1-Apr-2021 onwards, is there any restrictions while contributing to NPS (self and employer ), PPF?

Thanks

Does PPF and DSOP (Defence services officers Provident fund) comes under this. Request to pls clarify

Dear Kasi ji,

I believe that PPF is not included in this amendment.

I am not sure on DSOP.

Thank you

Sir

Could you help for the below scenario.

A person has total outstanding cumulative PF amount as Rs 10 Lakhs as on 01.04.2021.

He deposited as employee share Rs. 7 lakhs for year 2021-22.

By end of FY 2021-22 he will get interest for the 17 lakhs at 8.50℅ as Rs. 144500.

How much amount he should declare as taxable interest?

Dear Arun,

The taxable EPF contribution would be Rs 4.5 lakh (Rs 7 L -Rs 2.5 L).

The interest amount on this Rs 4.5 lakh is a taxable income and taxed at applicable slab rate.

Dear Sir,

A person with substantial PF balance already say 50 Lakhs who used to regularly invest around 1L per month, is it worth to switch to non-guaranteed MF/NPS investments for non-linear appreciation? Or is it advisable to continue in VPF and pay the income tax for the interest of 9.5L (12L – 2.5L) and get guaranteed returns?

Dear Ramesh,

It depends on ones financial goals, investment objectives, asset allocation n risk profile..

Dear Sreekanth

Is the below example correct?

Annual salary : 50 Lakhs

Basic (50%) : 25 Lakhs

PF (12% of basic) = 3 Lakhs

Interest on extra 50,000 = 4,250 (@8.5%)

So taxable amount is 4,250

Tax = 1275 (if 30% slab)

Dear Rajesh,

Yes, your understanding is correct!