NPS (National Pension Scheme) is one the very popular investment products in India. It is estimated that the Government employees contribute about 87% of the Rs. 2.3 lakh crore ($35 billion) overseen by the NPS, which started in 2004 and which was later opened to all citizens for voluntary contributions.

The Central Govt made NPS scheme mandatory for all the employees who joined the service on or after January 1, 2004. It has since been adopted by most state governments also. Currently, NPS has around 1.8 Crore subscribers with total Assets under Management (AUM) of more than Rs. 2.3 lakh crore.

The Government of India rolled out the National Pension Scheme (NPS) for all the citizens of India from May 1, 2009 and for corporate sector from December, 2011.

Types of NPS Accounts

National Pension System (NPS) offers two types of accounts – Tier I and Tier II.

The Tier 1 account is non-withdrawable till the person reaches the age of 60. Partial withdrawal before that is allowed based on certain rules. Income Tax benefits are available for Tier-1 accounts.

- Your NPS contributions of up to Rs 1.5 Lakh can be claimed as tax deduction u/s 80c.

- Latest Update : Contribution by government employees (only) under Tier-II of NPS will now be covered under Section 80 C for deduction up to Rs 1.5 lakh for the purpose of income tax provided there is a three-year lock-in period. This is w.e.f April, 2019.

- An additional tax deduction of Rs 50,000 u/s 80CCD (1b) is tax-exempt for Tier-1 deposits.

- If your employer also contributes to Pension Scheme, the whole contribution amount (10% of salary) can be claimed as tax deduction under Section 80CCD (2).

- Latest Update : The Centre will now contribute 14% of basic salary to their pension corpus, up from 10%. This is w.e.f April, 2019.

On the other hand, the Tier II National Pension Scheme account is just like a savings account and subscribers are free to withdraw the money as and whenever they require. Tier 2 NPS Account does not qualify for tax rebate under section 80C of the Income Tax Act. (The Govt/Public Sector employees can however claim contributions to NPS Tier-2 account u/s 80c up to Rs 1.5 lakh w.e.f 1st April, 2019.)

NPS Funds & Scheme Preferences:

Below mentioned three fund options (also known as asset classes) are available under NPS:

- Equity Fund (E)

- Government Securities Fund (G)

- Corporate Fixed Income Instruments other than Govt. Securities (C)

Recently a new fund category by name Alternate investment has been introduced.

The money invested in NPS is managed by PFRDA-registered Pension Fund Managers. At the moment, there are eight NPS pension fund managers:

- Birla Sun Life Pension Scheme

- HDFC Pension Fund

- ICICI Prudential Pension Fund

- Kotak Pension Fund

- LIC Pension Fund

- Reliance Capital Pension Fund

- SBI Pension Fund

- UTI Retirement Solutions

The govt employees’ NPS accounts and contributions are managed equally by three fund managers namely – LIC Pension Fund, SBI Pension Fund and UTI. Under this category, do note that up to 15% of corpus only can be invested in Equity fund. The rest of the corpus is allocated to Corporate Bonds and Govt securities. (There is a proposal to increase this cap to 50%.)

- Latest Update : W.e.f April 2019, on contributions made by the Govt employees, the equity component can be up to 50%. Also, the choice of Fund managers have been increased from current 3 to 8.

The pvt (corporate) sector employees and other individuals can also invest in NPS. The Equity fund threshold limit is 50% or 75% in this case. These individuals can select any of the two investment options to select scheme preferences.

- Active choice – Under this option, subscriber selects the allocation pattern amongst the three funds E, C and G. The Maximum allocation to Equity can be

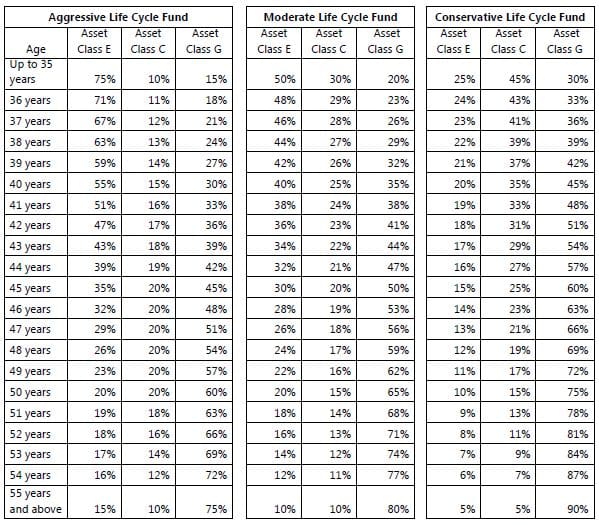

50%(increased to 75%) and 100% in Corporate or Govt securities. (Latest update (04-May-2018) : The proposal on increasing cap on equity investment in active choice to 75 per cent from currently 50 per cent has been approved by the PFRDA Board. However, it comes with a clause of tapering of the equity allocation after the age of 50 years.) - Auto Choice : Under this option, subscriber funds are automatically allocated amongst three funds E, C and G in a pre-defined portfolio pattern prescribed by PFRDA. When a subscriber chooses this option, it adopts a lifecycle-based approach, in which the allocation to different asset classes changes gradually as the person’s age increases.

- You will be given three types of funds to choose from –

- Moderate Life Cycle Fund (default option) – The “Moderate Life Cycle Fund” option provides you with the option of a Life Cycle fund with a reasonable risk profile, where the maximum equity allocation is kept at 50% up to the age of 35 years.

- Aggressive Life Cycle Fund – For “Aggressive Life Cycle Fund” maximum equity allocation is kept at 75% up to the age of 35 years.

- Conservative Life Cycle Fund – for “Conservative Life Cycle Fund” maximum equity allocation is kept at 25% up to the age of 35 years.

- With effective from 1st April 2017, NPS subscribers can change their investment option and asset allocation ratio ‘twice’ in a year. However, you can select the pension fund manager only once a year.

So, returns on your NPS investments are dependent on the type of Fund(s) who have chosen to invest.

Best Performing NPS Funds 2018 – Best NPS Fund managers 2018

Let us now analyze the best NPS Funds and their returns;

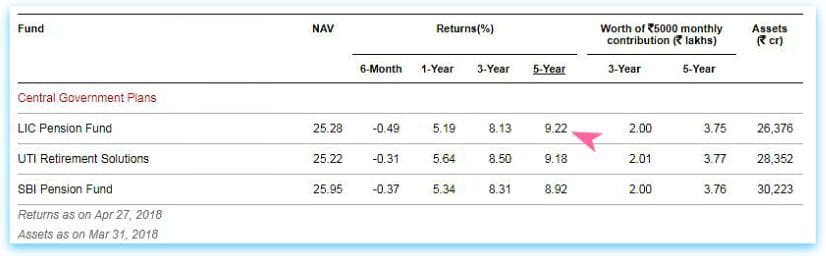

Best NPS Fund – Central Govt Plans

- The contributions to NPS Accounts by Central govt employees are equally managed by the three pension fund managers.

- The best NPS Fund manager based on the returns generated in the last 5 years is LIC Pension Fund. This fund has generated returns of around 9.2%.

- In terms of Assets under management, SBI Pension Fund is the biggest one with Assets of around Rs 30,223 cr.

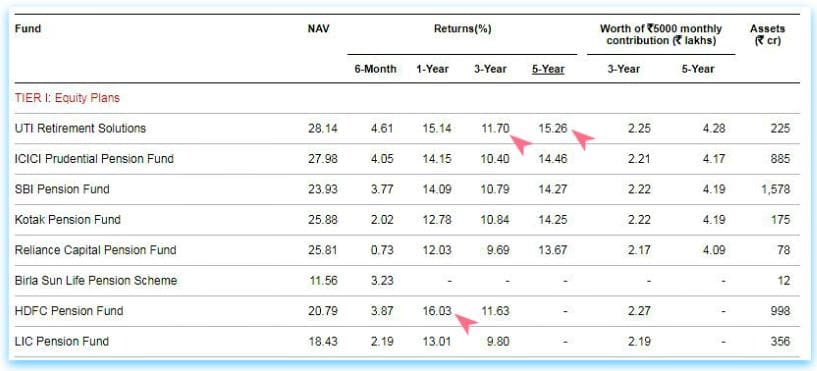

Best Performing NPS Tier-I Equity Funds Returns – Scheme E

- The best performing NPS Pension Fund manager under NPS Tier-1 Equity Plan is UTI Retirement Solutions. This scheme has generated returns of around 15.3% in the last 5 years.

- The UTI Retirement solutions fund – Equity plan has picked, Financials, Energy & Automobiles as top 3 sectors. Its portfolio comprises of 74 companies with highest exposure in Larsen & Toubro Ltd.

- The HDFC Pension Fund – Equity Plan has generated returns of around 16% for the last one year. The fund has been faring well based on the parameters of Returns, Downside risk and Consistency.

- The Equity plan offered by the SBI Pension Fund has the highest AUM of Rs 1,578 cr.

- The benchmark used for Equity plans is Nifty 50 Index.

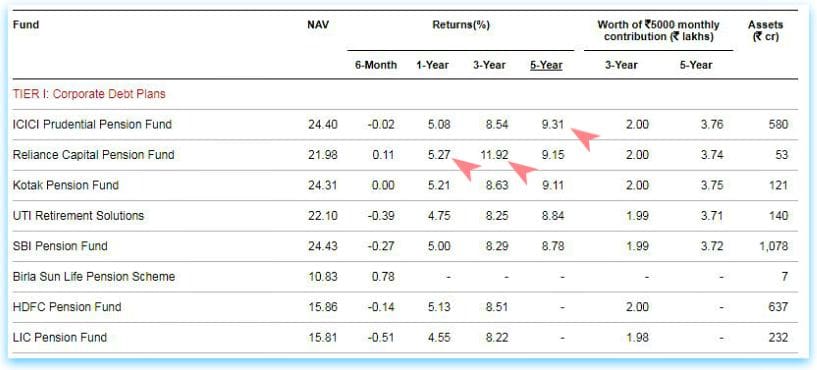

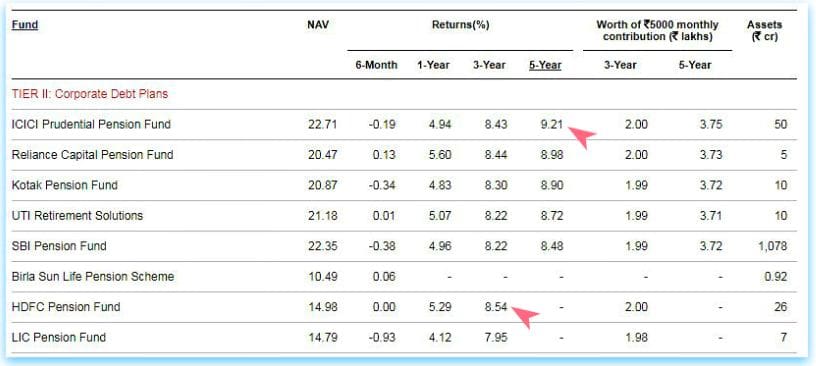

Top Performing NPS Fund Manager – NPS Tier 1 Funds – Corporate Debt Plans (C)

- The highest returns generated by NPS Funds under Corporate Fixed Income Plans are managed by ICICI Prudential and Reliance Capital Pension fund managers.

- The Kotak Pension Fund – Corporate Debt Scheme has also been performing well, based on the parameters of Returns, Downside risk and Consistency.

- SBI Pension Fund has the highest AUM of around Rs 1,078 cr.

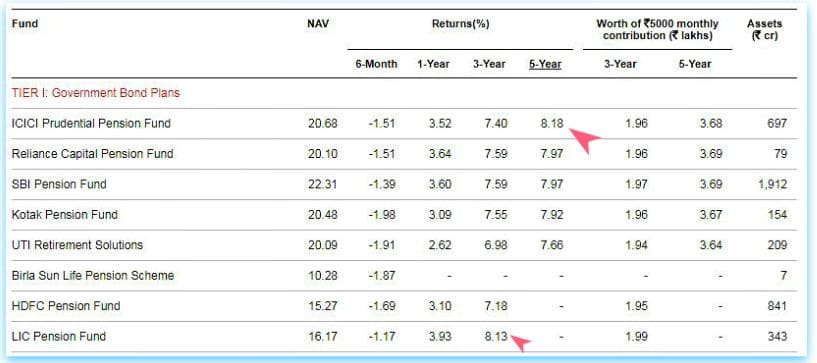

Top Performing NPS Tier-1 Funds Returns – Scheme G (Govt Securities)

- The Government Bond Plan offered by ICICI Prudential Pension fund has clocked returns of around 8.2% during the last 5 years.

Best NPS Pension Fund Returns – Tier II Account – Equity Plans (E)

- The Equity Scheme offered by UTI Retirement Solutions has generated returns of around 15.3% during the last 5 years. The fund’s portfolio has ‘financials’ sector with highest exposure. The top 3 stock picks are – L&T, Reliance industries & HDFC.

- Pension Fund manager HDFC’s Equity plan has also been performing well, with returns of around 12% in the last 3 years. This fund has been faring well based on the parameters of Returns, Downside risk and Consistency.

Best NPS Tier-II Funds Returns 2018 – Top Performing NPS Fund Manager Corporate Debt Plans (C)

- The highest returns generated by NPS Funds (Tier -II) under Corporate Fixed Income Plans are managed by ICICI Prudential, Reliance Capital Pension fund & HDFC Pension Fund managers.

Best NPS Pension Fund Returns – Tier II Account – Govt Bond Plans (G)

- The Tier-II Government Bond Plan offered by ICICI Prudential Pension fund has clocked returns of around 8.1% during the last 5 years.

NPS Funds Return Calculator

In case, you would like to do more analysis on the returns generated on various NPS Funds, you may visit NPS Trust portal. You have the option to download the NPS Funds returns data as well.

Besides Returns data, if you would like to do more research and analysis on other parameters like consistency of returns, standard deviation, Sharpe ratio, downside risk, up-side capture ratio, down-side capture ratio, Fund Asset allocation, risk-return matrix etc., you may visit ‘The Economic Times’ portal. Click here to access the details of Tier-1 Funds. You may visit this link to get the risk/return data of Tier-II Schemes.

Conclusion:

I believe that most of the investors opt for the NPS for two main reasons – i) for tax saving purpose & ii) No other choice than to invest as contribution to NPS has been made mandatory for the Govt employees.

Unfortunately, majority of the subscribers are not aware of ‘how NPS scheme works’ and invest in it just to save some taxes. Most of us are eager to know about the tax benefits that are being offered while contributing to NPS but are not worried about the applicable taxes at maturity (as per current tax rules).

Before you invest in NPS (if planning to invest), kindly understand the features of NPS, tax implications, withdrawal rules & mandatory clause to buy annuity product on maturity and then take a wise decision. If you have already invested in NPS, you may review your investment decision.

Given a choice between NPS and Mutual Funds, I would prefer investing in Mutual Funds to NPS.

Kindly share your views on NPS as investment choice? Have you invested in NPS? Which one do you prefer, NPS or MFs? Share your views, cheers!

Continue reading :

- How NPS Works? Features & Drawbacks of NPS Scheme

- Latest NPS Partial Withdrawal rules – 2018

- List of Best Investment options in India

- Best NPS Funds to invest in 2019-20

(Image courtesy of Mister GC at FreeDigitalPhotos.net) (References : Valueresearchonlne, NPS Trust portal & Economic Times) (Post first published on : 01-May-2018)

Join our channels

hi Srikanth

I am having my company tier 1 nps account , and also paying 50000 extra for tax benefit// ccd // ..sbi is the nps service provider chosen by me …

I am not aware of tier-2 benefits and use as well ? ..what is the benefit of having nps tier-2 account…going by your data ,I guess its a best way to park idle money instead of mutual funds as the expense ratio will be very less and the service provider is giving in equity about 15 percent returns ? that should be better than any balanced / debt fund returns .?

could you pls let know / correct my thoughts

thanks

thomas ,

Dear thomas,

If we keep the expense ratio aside, investing in mutual funds makes much more sense than in NPS.

If NPS Tier-1 is mandatory then you cant avoid it.

But, its prudent not to invest in NPS Tier-2.

Related articles :

* Is NPS a good investment avenue?

* NPS Withdrawals – Tax implications

I am ivesting in ICICI PRUDENTIAL PENSION FUND SCHEME TIER 1, from 2 years . The return I can see is just 0.02% which is 12 Rs per year.

Should I switch somewhere else?

What if I donot want to invest this year? Is it ok to donot invest every year?

Dear Sweta,

May I know the type of Fund you have chosen??

May I know your investment objective and time-horizon? And the reason for choosing NPS?

The current minimum contribution is Rs 1,000 per year. Earlier, a subscriber had to contribute at least Rs 6,000 in a financial year (April-March) to keep the Tier-1 account running.

Sir … I have Atal Pension yojana already,can i invest in NPS too with same PRAN…. is it allowed

Dear Nitin,

I believe that PRAN is an unique number. An individual is permitted to have only one PRAN which is unique, permanent and portable across jobs/employments and locations.

You can apply with same PRAN.

I HAVE INVESTED IN ATAL PENSION YOJNA SINCE LAST 4 YRS . CAN I GET DEDUCTION IN INCOME TAX ? IF YES, WHICH SECTION & HOW MUCH ?

ASHISH PANDEY

37 YRS

Dear Ashish,

The contributions to ‘Atal Pension Yojana’ are eligible for Tax Deduction under section 80CCD.

The max limit under all 80c series section is up to Rs 1.5 Lakh.

Related articles;

* Atal Pension Yojana (APY) – Govt’s Scheme – Details, Features & Benefits

* Income Tax Deductions List FY 2018-19 | List of important Income Tax Exemptions for AY 2019-20

Hi Sreekanth,

I am working with Private organisation kindly confirm me any law has been proposed for pvt company employee related to retirement please acknowledge me.

Dear HARINATH.. I am unable to get your query. Kindly re-phrase it!

Dear Sreekanth ,

i want to know about Retirement Age , in private company at which age employee can be retire from the company.

Dear Harinath,

The retirement age can vary from company to company.

There is no fixed retirement age for people working in private sector. It can generally be either 58 / 60 years.

However, as per Employees Provident Fund (EPF), on attaining 58 years of age, an EPF member ceases to be a member of PF automatically.

Hi Srikanth,

For retirement planning I’m investing in NPS and other goals like children’s education and loan repayments I’m investing mutual funds. I started investing in NPS after learning all the tax implications. I hope i’m doing the right kind of investment

Dear Raghuma,

If you are well aware of the features, withdrawal rules, annuity buying criteria, taxation rules of NPS etc and then taken the decision to invest in NPS, it is fine.

Related article : National Pension Scheme (NPS) – Why it is not a good Investment Option?

Hi thank for the article…bit confused though..Would you recommend investing in NPS for a person who is in early 30s and willing to add a corpus for his retirement instead of equity.?

Dear Gaurav,

May I know what is the confusion is about?

Given the current product structure which is complex and tax implications, may be it is prudent for someone who is in 30s to pick Mutual funds.

But, do note that NPS also work like mutual funds.

Thanks Sreekanth,

Thanks for your reply,

Actually I have heard about NPS many times in past and had a good study also about its working and return generated by it in past….The return generated by NPS has been very good comparing to fixed deposits, corporate deposits and Post office deposits…but while comparing with the Mutual funds which have more exposure in the equity, it lags behind a bit…but tax benefits make it more attractive to salaried class.

I was confused because my portfolio consists of fixed deposits, direct equity and MFs and I was thinking about closing the FDs and convert it into NPS…I am a NRI so not concerned about the tax I just need a reasonable return along with the bit more security than the open equity…was confused that should I go for the NPS or should I go for large cap MFs…

Thanks for the advise…will go for MFS..

Dear Gaurav,

Kindly note that Mutual Funds does not necissarily mean they invest only in equity.

We have different categories in mutual funds.

If the person who is paying NPS from past one year, unfortunately, died then what is the situation whether the scheme will continue? or what will be happening? Please advise.

Dear Raju,

In case of death of the subscriber, option will be available to the nominee to receive 100% of the NPS pension wealth in lump sum. In case, nominee is not alive legal heir to the subscriber can claim the corpus.

Withdrawal form needs to be submitted by all the nominees registered in CRA system. In case the nominee is a minor, Withdrawal form has to be submitted by the guardian along with the birth certificate of the minor.

ollowing documents are to be submitted alongwith the completely filled Withdrawal forms at CRA:

Covering Letter from the associated Nodal Office to be submitted alongwith the Withdrawal form.

Advanced stamped receipt need to be duly filled and cross-signed on the Revenue stamp by the Subscriber.

Original PRAN card OR affidavit in case of Non submission of PRAN card.

KYC documents (address and photo-id proof) attested by mapped Nodal Office.

‘Cancelled Cheque’ (having subscriber’s Name, Bank Account Number and IFS Code) or ‘Bank Certificate’ on Bank Letterhead having claimant’s name, Bank Account Number and IFS Code required to be submitted as bank proof. ‘Copy of Bank Passbook’ can be accepted, however, it should have claimant’s photograph on it and should be self attested by the claimant.

Original Death Certificate issued by the Local Authority.

In case of Nomineesdetails are not available in the CRA system, a legal heir certificate OR a certified copy of family member’s certificate issued by Executive Magistrate is required indicating the relationship of the claimant with the deceased as well as supporting documents is to be provided. If the all the legal heirs are not claiming the pension funds, Relinquishment deed to be submitted from all the legal heirs (except the Claimant) on a Stamp paper of Rs. 100/-alongwith the KYC documents (Photo ID proof and Address proof) of all the legal heirs duly attested by the mapped Nodal Office. Also an Indemnity bond needs to be obtained from the claimant stating the responsibility for claiming on behalf of all the legal heirs.

Nodal Office has to submit the Death IRA compliance certificate if the subscriber’s PRAN is Non-IRA compliant.

If we compare between EPF and NPS which one do you prefer.

NPS bad because of tax implications on maturity amount, withdrawal rules & mandatory clause to buy annuity product on maturity.

EPF is bad from return point of you.

I know I am not doing apple to apple comparison but most of the salaried people compare these two.

Thanks in advance.

Dear Hugar,

Let’s interpret like this;

Given a choice, I would invest in PPF/EPF and then pick Mutual Funds for my financial goals.

very true information about NPS fund

I INVESTED THREE INSTALLMENT FROM 2016 17 2017 18 & 2018 19 TOTAL RS 150000 & GOING TO ATTAIN 60 YEAR IN KOTAK DEBT FUND ON AUGIST 2018 WHAT IS WITHDRAWAL AMOUNT.RETERMENT ON AUG.2018

Dear VIPAN ji,

Did you invest in Tier-I or Tier-II account?