NPS (National Pension Scheme) is one of the very popular Pension oriented products in India. As on 31st October 2019, NPS has around 1.29 Crore subscribers with total Assets under Management (AUM) of more than Rs. 3.74 lakh crore.

NPS was started in 2004 for govt sector employees and which was later opened to all citizens for voluntary contributions from May 1, 2009 and for corporate sector from December, 2011.

As on 31st October 2019, it is estimated that the Government employees (Central / State) have contributed around Rs 2.37 lakh crore to NPS Scheme.

What are the Latest NPS Norms & Rules 2019

There have been significant changes done NPS structure over the last few years. Below are the latest NPS norms w.e.f April 2019.

- National Pension System (NPS) offers two types of accounts – Tier I and Tier II. Income Tax benefits are available on Tier-1 deposits only. However, contribution by the government employees (only) under Tier-II of NPS will also be covered under Section 80C for deduction of up to Rs 1.5 lakh for the purpose of income tax, provided there is a three-year lock-in period. This is w.e.f April, 2019.

- If your employer (Govt) contributes to Pension Scheme, the whole contribution amount (10% of salary) can be claimed as tax deduction under Section 80CCD (2). The Centre now contributes 14% of basic salary to their pension corpus, up from 10%. This is w.e.f April, 2019.

- W.e.f April 2019, on contributions made by the Govt employees, the equity component can be up to 50%. Also, the choice of Fund managers have been increased from 3 to 7.

- Earlier, 40% of the accumulated corpus utilized for the purchase of the annuity is tax-exempt. Of the remaining 60% corpus withdrawn by the NPS subscriber at the time of retirement, 40% is tax-exempt and 20% is taxable. The tax exemption is now extended to the entire 60%.

Types of NPS Funds, Scheme Preferences & Fund Managers :

The returns on your NPS investments are primarily dependent on the type of Fund(s) and Pension Fund manager that who have chosen to invest.

So, you need to know and understand the different types of NPS Funds.

Below mentioned four fund categories / Investment options (also known as asset classes) are available under National Pension System:

- Equity Fund (E)

- Government Securities Fund (G)

- Corporate Fixed Income Instruments other than Govt. Securities (C)

- Alternative Investments (Tier-1)

The money invested in NPS is managed by PFRDA-registered Pension Fund Managers. At the moment, there are eight NPS pension fund managers:

- Birla Sun Life Pension Scheme

- HDFC Pension Fund

- ICICI Prudential Pension Fund

- Kotak Pension Fund

- LIC Pension Fund

- SBI Pension Fund

- UTI Retirement Solutions

Reliance Pension Fund Manager has exited NPS in Aug 2019. If you had selected Reliance Pension Fund as your NPS Fund Manager, your funds are auto-migrated to LIC Pension Fund (or) you can actively choose any other Fund manager of your choice.

The govt employees’ NPS accounts and contributions are currently managed equally by three fund managers namely – LIC Pension Fund, SBI Pension Fund and UTI. The fund managers options will be increased to eight. Under this category, do note that up to 15% of corpus (optional 50% w.e.f. April, 2018) only can be invested in Equity fund. The rest of the corpus is allocated to Corporate Bonds and Govt securities.

The pvt (corporate) sector employees and other individuals can also invest in NPS. The Equity fund threshold limit is 50% or 75% in this case. These individuals can select any of the two investment options to select scheme preferences.

- Active choice – Under this option, subscriber selects the allocation pattern amongst the three funds E, C and G. The Maximum allocation to Equity can be 75% and 100% in Corporate or Govt securities. (However, there is a clause of tapering of the equity allocation after the age of 50 years.)

- Auto Choice : Under this option, subscriber funds are automatically allocated amongst three funds E, C and G in a pre-defined portfolio pattern prescribed by PFRDA. When a subscriber chooses this option, it adopts a lifecycle-based approach, in which the allocation to different asset classes changes gradually as the person’s age increases.

- You will be given three types of funds to choose from –

- Moderate Life Cycle Fund (default option) – The “Moderate Life Cycle Fund” option provides you with the option of a Life Cycle fund with a reasonable risk profile, where the maximum equity allocation is kept at 50% up to the age of 35 years.

- Aggressive Life Cycle Fund – For “Aggressive Life Cycle Fund” maximum equity allocation is kept at 75% up to the age of 35 years.

- Conservative Life Cycle Fund – for “Conservative Life Cycle Fund” maximum equity allocation is kept at 25% up to the age of 35 years.

- With effective from 1st April 2017 NPS subscribers can change their investment option and asset allocation ratio ‘twice’ in a year. However, you can select the pension fund manager only once a year.

Now that you are clear about the various NPS Fund categories/classes, let’s now look at the top performing NPS Schemes 2019-20.

Best NPS Funds 2020 – Best NPS Fund Returns – Top Performing NPS Scheme Fund Manager

Below are the best NPS Funds to invest in 2020-21;

Best NPS Fund Returns – Central Govt Scheme

- The contributions to NPS Accounts by Central govt employees are currently equally managed by the three pension fund managers.

- Under Central Govt Scheme, the equity exposure typically ranges from 8% to 12% of a fund’s portfolio.

- The best NPS Fund manager based on the returns generated in the last 5 years is SBI Pension Fund. This fund has generated returns of around 9.12%. The Fund’s current asset allocation (as on 29-11-2019) between Equity & Debt is around 10.63% : 88.37%.

- In terms of Assets under management, SBI Pension Fund is the biggest one with Assets of around Rs 45,100 cr.

Best NPS Fund Manager 2020 – State Govt Scheme

- The Funds’ Equity allocation ranges from 7% to 11%.

- The best NPS Fund manager based on the returns generated in the last 5 years is SBI Pension Fund. This fund has generated returns of around 9.18%. The current asset allocation between Equity & Debt is around 9.61% : 90.39%.

- In terms of Assets under management, SBI Pension Fund is the biggest one with Assets of around Rs 65,800 cr.

Top Performing NPS Tier-I Equity Fund Manager 2020

- The best performing NPS Pension Fund manager under NPS Tier-1 Equity Plan is HDFC Pension Fund. This scheme has generated returns of around 8.24% and in the last 5 years.

- The HDFC Pension fund – Equity plan has picked Financials as the top sector. Nearly 7.59% of the Fund’s Equity corpus has been invested in Reliance Industries stock, followed by ICICI Bank. It has an Equity : Debt allocation of around 95.99% : 4.11%.

- The HDFC Pension Fund – Equity Plan has been faring well based on the parameters of Returns, Downside risk and Consistency.

- The Equity plan offered by the SBI Pension Fund has the highest AUM of Rs 8,865 cr.

- The benchmark used for Equity plans is CNX Nifty 50 Index.

Best NPS Fund Tier-1 under Scheme-G Category (Govt Securities / Bonds)

- The Government Bond Plan offered by LIC Pension fund has clocked returns of around 10.23% during the last 5 years. The Fund has allocation of around 49% to GoI securities.

- SBI Pension fund Scheme G Plan has also been performing well.

Top Performing NPS Fund Manager – NPS Tier 1 Funds – Corporate Debt Plans (Scheme C)

- The highest returns generated by NPS Funds under Corporate Fixed Income Plans are managed by ICICI Prudential Fund Manager.

- ICICI Scheme C (Tier-1) has an allocation of around 96.76% to Debt securities, with a 49.7% sub-allocation to Debentures.

- The HDFC Pension Fund – Corporate Debt Scheme has also been performing well, based on the parameters of Returns, (better) Downside risk and Consistency.

- SBI Pension Fund has the highest AUM of around Rs 1,800 cr.

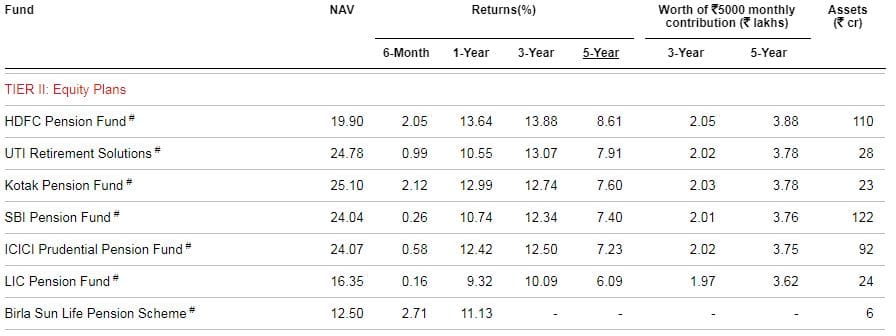

Best NPS Pension Fund Returns – Tier II Account – Equity Plans (E)

- The Equity Scheme offered by HDFC Pension Fund has generated returns of around 8.61% during the last 5 years. The fund’s portfolio has ‘financials’ sector with highest exposure, followed by the Energy & Technology sectors. The top stock pick is Reliance industries.

- The Pension Fund manager ICICI Prudential’s Equity plan has the highest exposure to Equity at round 99%. HDFC has around 96% exposure to equity.

Best NPS Pension Fund Returns – Tier II Account – Govt Bond Plans (G)

- The Tier-II Government Bond Plan offered by LIC Pension fund has clocked returns of around 10.43% during the last 5 years. It has an exposure of around 59% to GoI securities.

- SBI Pension fund has also been faring well based on the parameters of Returns, Downside risk and Consistency.

Best NPS Tier-II Funds Returns 2020 – Top Performing NPS Fund Manager Corporate Debt Plans (Scheme C)

- The highest returns generated by NPS Funds (Tier -II) under Corporate Fixed Income Plans are managed by ICICI Prudential & HDFC Pension Funds.

Who is the Best NPS Fund Manager 2020?

We now have fair idea on the best and top performing NPS Schemes to invest in 2020-21. So, who is the best NPS Fund manager? You may consider below fund managers while investing in NPS Scheme;

- The Fund managed by SBI Pension Fund Manager is the best one in case of Central / State Govt NPS Schemes.

- Under Scheme -E (Equity Funds), HDFC Pension Fund has been doing good job.

- For NPS Govt Bond Plans (Scheme-G), LIC Pension Fund has been able to perform consistently well.

- For NPS Corporate Bond Plans (Scheme-C), ICICI Prudential Pension Fund has been able to generate better returns.

How to calculate Returns on NPS Fund Scheme?

In case, you would like to do more analysis on the returns generated on various NPS Funds for a specific time-period, you may visit NPS Trust portal.

Besides Returns data, if you would like to do more research and analysis on other parameters like consistency of returns, standard deviation, Sharpe ratio, downside risk, up-side capture ratio, down-side capture ratio, Fund Asset allocation, risk-return matrix etc., you may visit ‘The Economic Times’ portal. Click here to access the details of Tier-1 Funds. You may visit this link to get the risk/return data of Tier-II Schemes.

You can find respective NPS Fund’s scheme portfolio details at this link..

Latest NPS Income Tax Benefits FY 2019-20 / AY 2020-21

There have been continuous efforts from the Govt to realign NPS to make it more tax-friendly for the investors. Hence, the NPS tax rules have been changing for the last few year. Below are the latest tax deductions an NPS investor can claim for FY 2019-20 / AY 2019-21.

My perspective on NPS:

I believe that most of the investors opt for the NPS for two main reasons – i) for tax saving purpose & ii) No other choice than to invest as contribution to NPS has been made mandatory for the Govt employees.

Unfortunately, majority of the subscribers are not aware of ‘how NPS scheme works’ and invest in it just to save some taxes. Note that NPS does not give you Pension. The subscriber has to re-invest the NPS Withdrawal corpus in an annuity insurance product.

Before you invest in NPS (if planning to invest), kindly understand the features of NPS, tax implications, withdrawal rules & mandatory clause to buy annuity product on maturity and then take a wise decision. If you have already invested in NPS, you may review your investment decision.

Given a choice between NPS and Mutual Funds, I would prefer investing in Mutual Funds to NPS.

Kindly share your views on NPS as an investment choice? Have you invested in NPS? Is NPS your preferred choice for tax saving? Which one do you prefer, NPS or MFs for your long-term retirement planning? Share your views, cheers!

Continue reading :

- How NPS Works? Features & Drawbacks of NPS Scheme

- Tax Implications of EPF, PPF & NPS Withdrawals (Full / Partial) & Maturity proceeds

- Income Tax Deductions List FY 2019-20 | List of important Income Tax Exemptions for AY 2020-21

- List of all Popular Investment Options in India – Features & Snapshot

- Top 15 Best Mutual Funds to invest in 2020 & beyond | Top Performing Equity Funds

(Image courtesy of Mister GC at FreeDigitalPhotos.net & Social media image source: The Economic Times) (References : Valueresearchonlne, NPS Trust portal & Economic Times. ) (Post first published on : 09-December-2019)

Join our channels

Dear Sreekanth,

I am private job employee, doing yearly contribution in Tier 1, of Rs 50k…I have selected the SBI for managing the fund,

Is this good option in terms of Fund manager or can i change it to HDFC..Please advice

Dear Rutushar,

Which Scheme have you selected? What is your allocation as of now?

I am a central govt employee of age 25.Right now my contribution is distributed in 3 fund managers equally under standard option.How can i get more return ,which option should i select.please provide guidance.

Dear Aman,

Under Govt employees category, do note that up to 15% of corpus (optional 50% w.e.f. April, 2018) only can be invested in Equity fund. The rest of the corpus is allocated to Corporate Bonds and Govt securities.

So, check your allocation to equity. If you can afford to take risk, can allocate it to max 50% to equity.

Sir i am a central government employee(Age 25) and my default scheme is currently active on nps tier-1 that is equal share of 33% has been divided among three fund manager(sbi,uti,lic).There is a option to change my preference through app under which there are two sections auto and active choice.

1.Auto choice gives me option to select sub scheme preference type that is moderate or conservative auto choice followed by selection of fund manager(ALL 8 fund manager).

2.Active choice gives me option to select the fund manager followed by their scheme which is only scheme G of the fund manager(ALL 8 fund manager).

Sir i would like to know about these two options and how can i increase my returns.Which fund manager would be suitable for me?

Dear aman,

Under active choice, you dont have the option to choose Equity allocation??

Active choice gives me option to select the fund manager followed by their scheme which is only scheme G of the fund manager(ALL 8 fund manager).

I dont know if i click on sbmit button then may be i should get equity allocation option.but i am not sure so i did not go forward.I have screen schots to share but there is no option available here.if you can give me alternative way to provide screenshots?

Dear Aman,

Suggest you to check with your employer (HR/Fin Dept) if they can guide you or check with any of your collegues if they have opted for higher equity allocation??

Hi Sreekanth, Really Nice. You have put the points very Well.

Valuable info sreekanth garu!

Best option is to invest in equity MF for equity portion and in NPS for debt portion.

just wanted to know what happens if you join the NPS after 35? Would they not allow you to have the 75% equity option?

Dear Smit,

You can opt for ‘Active choice’ while investing in NPS.

Active choice – Under this option, subscriber selects the allocation pattern amongst the three funds E, C and G. The Maximum allocation to Equity can be 75% and 100% in Corporate or Govt securities. (However, there is a clause of tapering of the equity allocation after the age of 50 years.)

Thanks Sreekanth