Effective April 1, 2026, India’s taxation landscape undergoes a historic transformation with the implementation of the Income Tax Act, 2025 (replacing the 1961 Act) and the Income Tax Rules, 2026. These reforms aim to simplify compliance, rationalize rates, and modernize the tax structure.

At first glance, you might think, “Oh no, new tax rules again?” But the truth is, this change isn’t about paying more tax. It’s about bringing in a new structure and a smarter compliance system that makes things easier for both taxpayers and authorities.

The new income tax rules effective from April 1, 2026 introduce a simplified tax system under the Income Tax Act, 2025. Key changes include the replacement of Assessment Year with Tax Year, revised compliance structure, updated PAN and reporting limits, simplified TDS/TCS provisions, and clearer capital gains rules. While tax slabs remain largely unchanged, the focus is on improved transparency, easier filing, and stricter reporting.

Let’s understand what’s really changing, in simple terms.

New Income Tax Rules 2026: What You Must Know

1. The “Tax Year” Concept

Earlier, we had two confusing terms — Previous Year (when income is earned) and Assessment Year (when it’s filed). From April 1, 2026, this distinction is gone. Now, there’s just one term — the Tax Year.

For example, income earned between April 1, 2026, and March 31, 2027, will fall under Tax Year 2026–27.

2. Revised Exemptions for Salaried Employees

Good news for employees — many outdated allowance limits under the old regime have finally been updated to match today’s cost of living.

- Children’s Education Allowance: Hiked from ₹100/month to ₹3,000/month per child.

- Hostel Expenditure Allowance: Increased from ₹300/month to ₹9,000/month per child.

- Meal Vouchers: Tax-free limit on corporate meal cards or coupons raised from ₹50 to ₹200 per meal.

- Corporate Gifts: Tax-free threshold for gift cards or vouchers now ₹15,000 per year.

- Home-to-Office Commute: Daily commute provided or reimbursed by the employer will no longer be taxed as a perquisite.

- Medical Loans: Interest-free or concessional loans provided by employers for medical treatment are now tax-exempt up to ₹2 Lakh (previously ₹20,000).

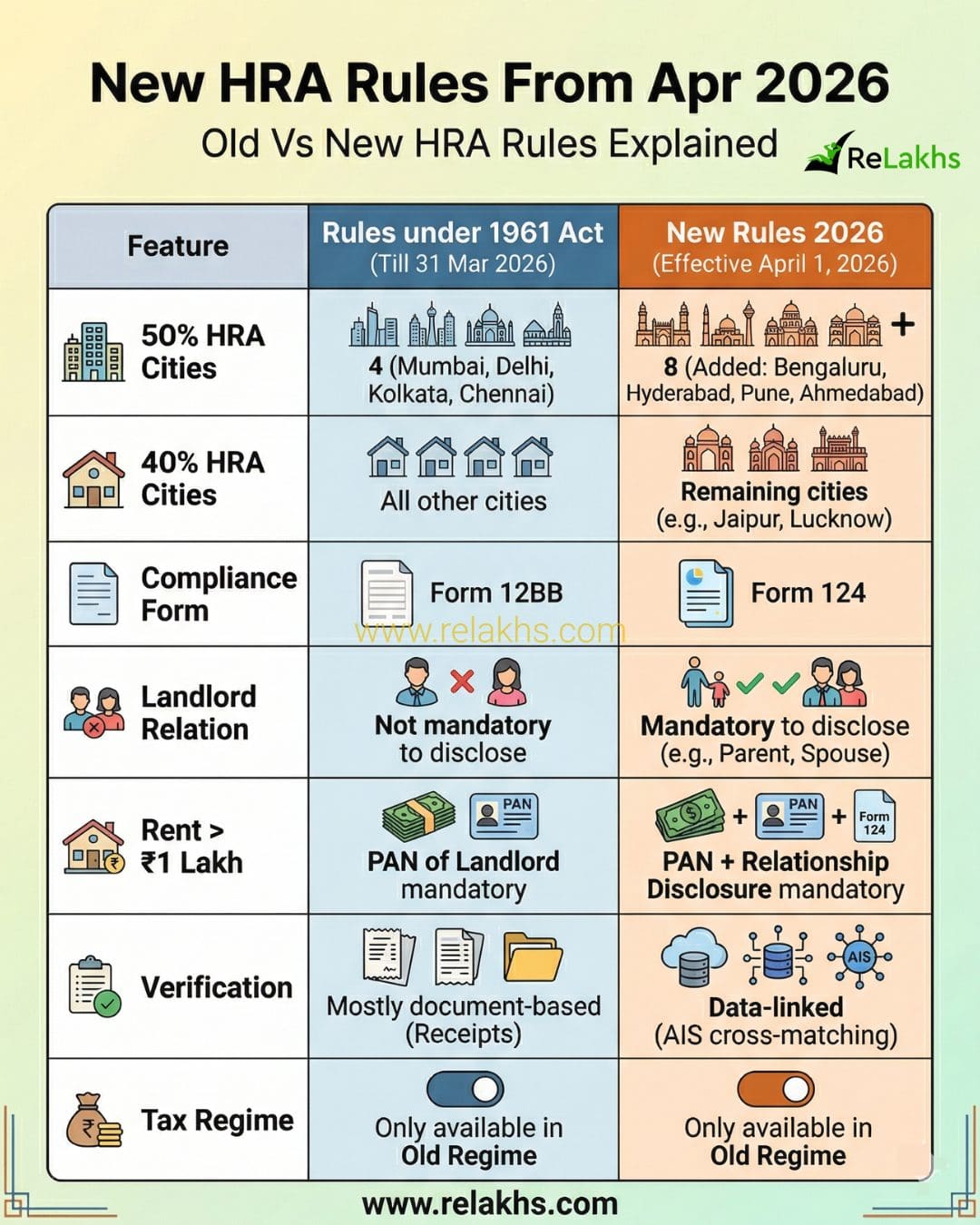

3. Salaried Employees & HRA New Rules

While the standard deduction (₹50,000) and Section 80C limits (₹1.5 lakh) remain unchanged, HRA rules have seen a major expansion (under the Old Tax Regime):

- New “Metro” Cities for HRA: The 50% HRA exemption (previously limited to Delhi, Mumbai, Kolkata, and Chennai) has been extended to four more tech hubs: Bengaluru, Pune, Hyderabad, and Ahmedabad.

- Mandatory Relationship Disclosure: When claiming HRA, you must now disclose your relationship with the landlord in the new Form 124. This is specifically targeted at those paying rent to parents or spouses to ensure the transaction is genuine.

4. ITR Filing & Compliance Relief

- The new system also makes filing and corrections more flexible. For individuals with business or professional income (filing ITR-3 or ITR-4 without audit), the due date has been extended from July 31 to August 31. For salaried taxpayers filing ITR-1 or ITR-2, the deadline remains July 31.

- You’ll also get more time to fix mistakes — 12 months instead of 9 — from the end of the Tax Year to file a revised return. However, a small fee will apply if you revise it after the initial 9-month window.

- Another welcome move: a one-time 6-month window for residents, including relocated NRIs and students, to voluntarily disclose small foreign assets or income that might have been missed earlier, without severe penalties.

5. No SFT Reporting for Mutual Funds (₹10 Lakh)

In a major relief for the mutual fund industry and investors, the requirement for Mutual Fund Houses (AMCs) to report transactions under the Statement of Financial Transactions (SFT) has been revised.

- The Change: Previously, MF houses were required to report any investor who invested ₹10 lakh or more in a financial year. Under the new rules notified on March 20, this specific reporting requirement for mutual fund investments has been removed.

- The Intent: This is aimed at reducing the compliance burden on AMCs and the volume of “routine” data flowing to the tax department.

- Note: While the AMC might not report the transaction under this specific ₹10 lakh SFT trigger, your investment details are still captured via your PAN and will continue to appear in your Annual Information Statement (AIS) through other depository and banking channels.

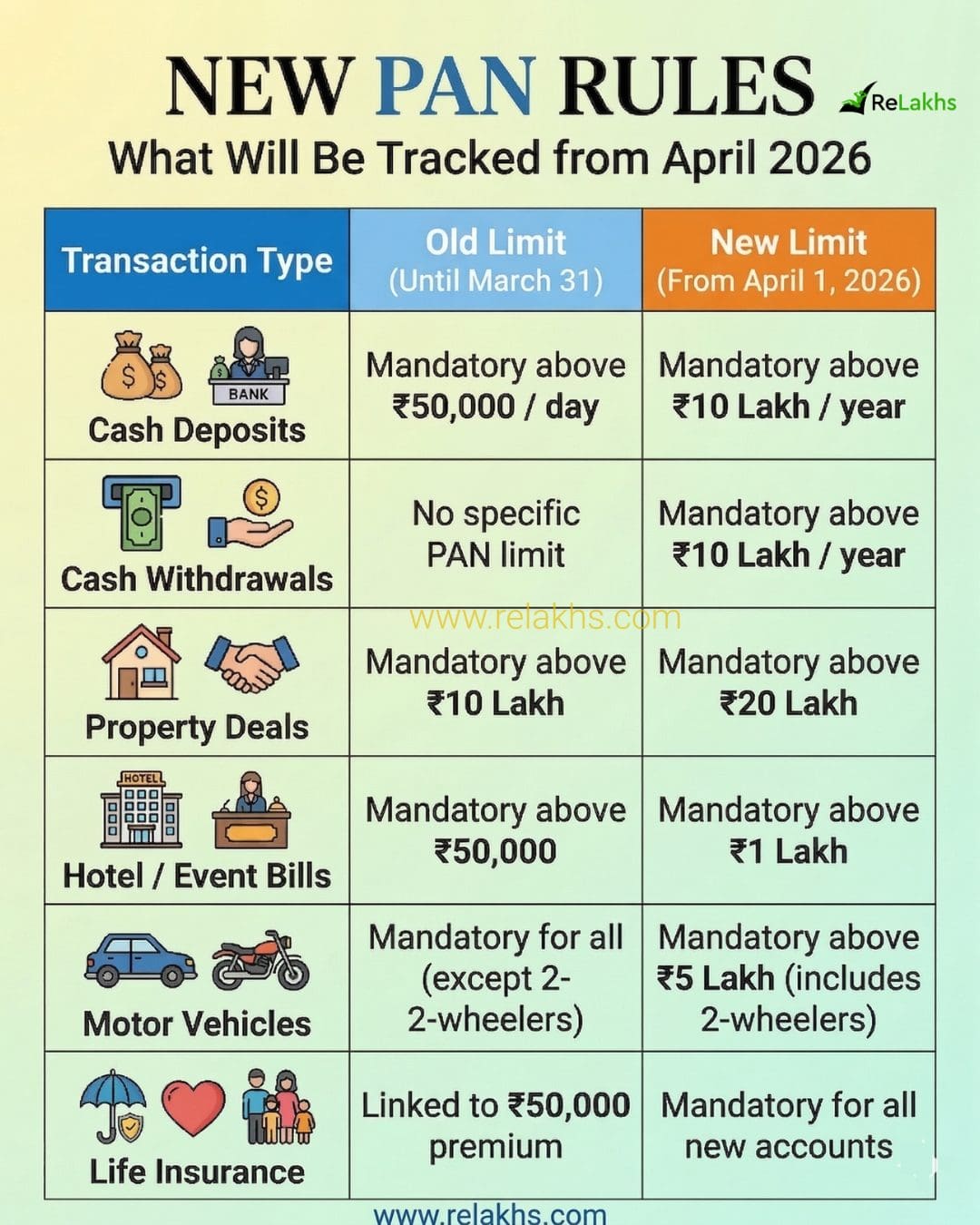

6. New PAN Limits

To ease compliance, the government has revised several thresholds for quoting PAN and reporting high-value transactions under SFT (Statement of Financial Transactions).

- Cash Transactions: PAN will now be required only if your total cash deposits or withdrawals exceed ₹10 lakh in a financial year, replacing the older ₹50,000 per day rule.

- Property & Vehicles:

- Immovable Property: PAN requirement increased from ₹10 lakh to ₹20 lakh.

- Motor Vehicles: PAN is mandatory only for vehicles priced above ₹5 lakh, unlike earlier when it applied to all cars.

- Hotels & Travel: PAN requirement for cash payments raised from ₹50,000 to ₹1 lakh.

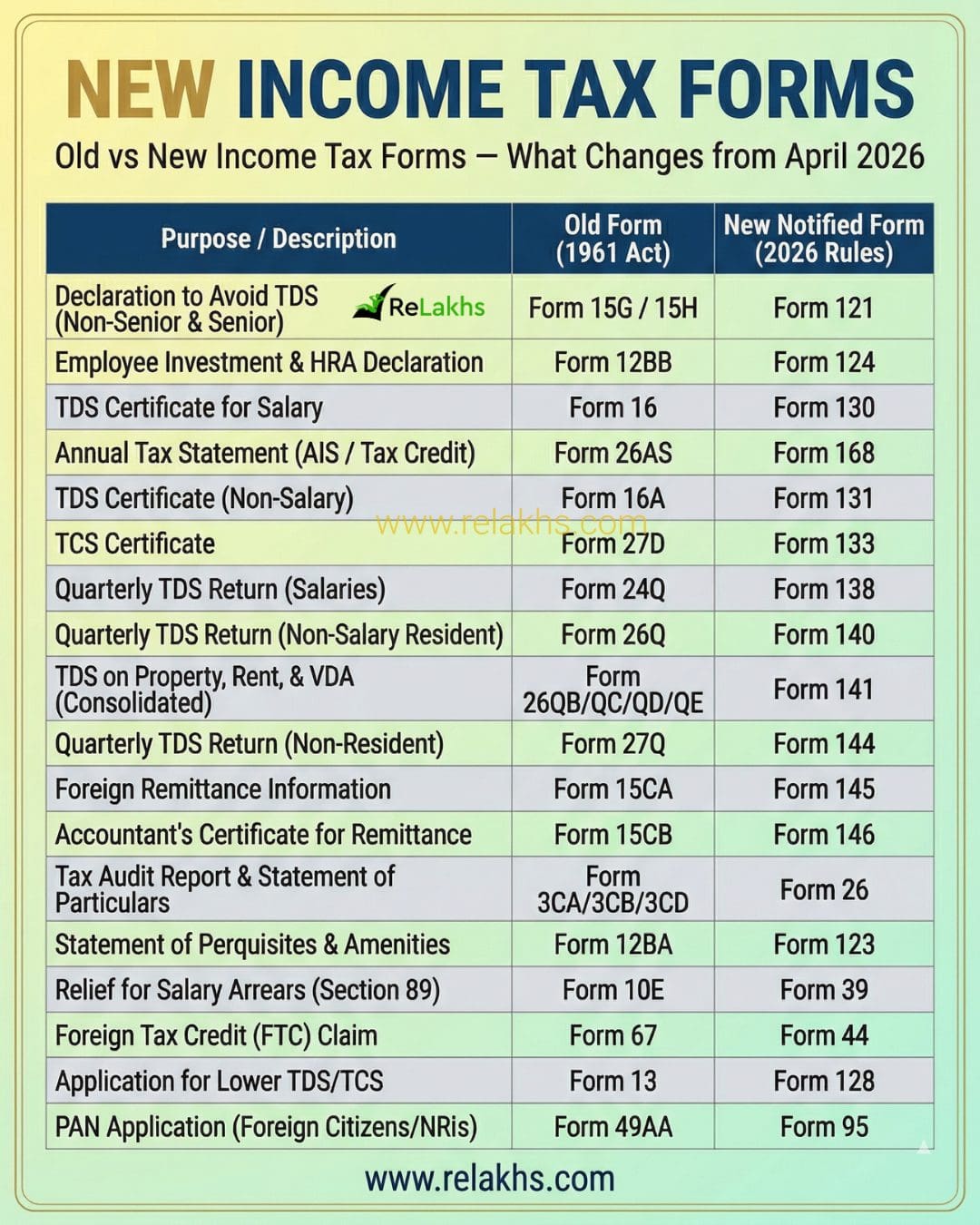

7. Renumbered Forms | New Tax Form Names

Familiar forms have been renamed under the new Act to streamline the database:

8.TCS (Tax Collected at Source) Rationalization

The TCS rules have been eased in a few important areas. For LRS remittances made for education or medical treatment, the TCS rate on amounts above ₹10 lakh has been reduced from 5% to 2%, bringing down the upfront cash outflow for families.

Also, for overseas tour packages, a flat 2% TCS will now apply across the board, replacing the earlier slab-based system with different rates and thresholds, and making the rules simpler to understand and comply with.

9. Investment & Capital Gains Changes

- Share Buybacks: Proceeds from a share buyback will now be taxed as Capital Gains in the hands of the shareholder, rather than as “deemed dividends.”

- No Interest Deduction on Dividends: You can no longer deduct interest expenses (previously capped at 20%) incurred to earn dividend or mutual fund income. This income will now be fully taxable at slab rates.

- STT Hike on Derivatives: Securities Transaction Tax (STT) on Futures increases to 0.05% (from 0.02%) and on Options to 0.15% (from 0.1%).

- Holding Period Clarity: For converted securities (like debentures converted to shares), the holding period will now include the duration of the original instrument, potentially helping you qualify for Long-Term Capital Gains (LTCG) sooner.

- Sovereign Gold Bonds (SGB): Capital gains exemption on SGBs is now restricted to original subscribers who hold the bonds until maturity.

10. Property Purchase from NRIs

The new tax rules effective April 1, 2026, introduce a major simplification for residents purchasing immovable property from Non-Resident Indians (NRIs). The most critical update is the removal of the mandatory Tax Deduction Account Number (TAN) requirement for buyers.

If you’re buying property from an NRI, you no longer need to apply for a TAN just to deduct TDS. You can simply use your own PAN to deduct and deposit the TDS, which cuts down a lot of paperwork and compliance hassle. This update also brings the process in line with property purchases from resident sellers, where using PAN has always been enough.

Tax rules keep changing every few years, but this time the shift is more about transparency than taxation. You’re not being asked to pay more, but you are expected to report better. So don’t panic — just stay informed and adapt to the new system.

If you found this article helpful, consider bookmarking it for future reference and sharing it with someone who might need this clarity.

Continue reading:

- Latest TDS Rates Tax Year 2026-27 – Complete Chart

- New PAN Rules from April 2026: Limits & Impact

- New HRA Rules from April 2026: What You Must Know

- New Income Tax Forms 2026: Full List & Form Numbers Explained

(Post first published on : 2-March-2026)

Join our channels