LIC has launched a new joint-life guaranteed savings product called LIC New Jeevan Sathi – Limited Premium (Plan no 889) and is available for purchase from 1 June 2026.

This is a non-linked, non-participating, guaranteed return joint-life insurance plan where a married individual can buy a single policy covering both spouses.

It is marketed as a unique joint-life traditional savings plan designed specifically for couples (“Two lives, One promise, Secured together”).

This post takes a clear, numbers-first look at the plan using figures from the official brochure. It goes beyond the marketing to work out the exact IRR (Internal Rate of Return) and see whether it is worth adding to your portfolio.

Key Features of LIC New Jeevan Sathi

This plan is a Non-Participating, Non-Linked, Joint Life, Limited Premium Endowment Savings Plan.

- Joint Life Cover: Both you and your spouse are insured under a single policy.

- Limited Premium Payment Term (PPT): You do not need to pay premiums for the entire duration of the policy. PPTs are limited to options like 5, 10, or 15 years for policy terms extending up to 25 years.

- Guaranteed Additions (GA): The brochure highlights a “Guaranteed Addition of 7% on the total annual premium paid.” These accumulate every year and are paid out at the end of the term.

- Premium Waiver on First Death: If one spouse passes away during the premium paying term, all future premiums are completely waived. The surviving spouse remains fully covered until the end of the policy term without making further payments.

- Maturity Payout: Paid out as a lump sum at the end of the policy term if both or either of the lives survive.

LIC New Jeevan Sathi Policy | How it Works?

The official brochure provides two distinct sample illustrations for a couple where both individuals are 35 years old choosing a Basic Sum Assured of Rs. 10,00,000.

Option I: Longer Horizon (PT: 25 Years, PPT: 15 Years)

- Age of husband & wife: 35 years

- Annual Base Premium: Rs. 83,650

- Policy Term: 25 years

- Premium Payment Period (PPT): 15 Years

- Total Premium Invested: Rs. 12,54,750

- Maturity Benefit at Year 25: Rs. 27,61,669 (This includes the Rs. 10,00,000 Basic Sum Assured + Rs. 17,61,669 in accumulated Guaranteed Additions).

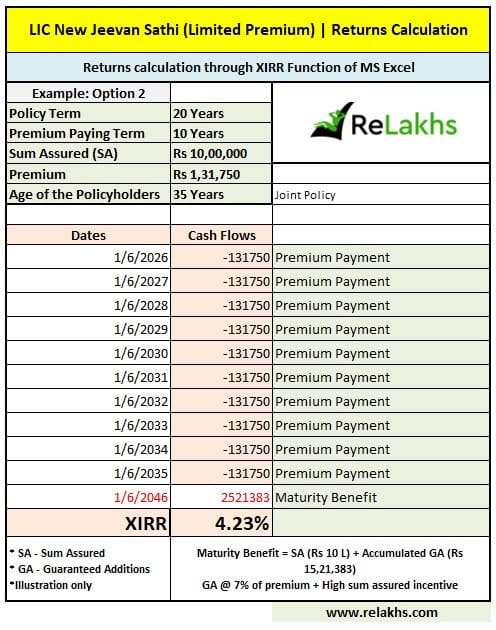

Option II: Shorter Horizon (PT: 20 Years, PPT: 10 Years)

- Age of husband & wife: 35 years

- Annual Base Premium: Rs. 1,31,750

- Policy Term: 20 years

- Premium Payment Period: 10 Years

- Total Premium Invested: Rs. 13,17,500

- Maturity Benefit at Year 20: Rs. 25,21,383 (This includes the Rs. 10,00,000 Basic Sum Assured + Rs. 15,21,383 in accumulated Guaranteed Additions).

LIC New Jeevan Sathi Limited Premium Plan – Real Returns Explained

While a headline of “7% Guaranteed Additions” sounds attractive, it is crucial to recognize that this 7% is calculated on the annual premium paid, not compounded on the total accumulated balance.

If we map out the exact year-by-year cash flows and solve for the Internal Rate of Return (IRR) using financial functions (assuming survival of both partners), the net compounded returns are as follows:

| Parameter | Option I (25-Yr Term) | Option II (20-Yr Term) |

| Premium Paying Term | 15 Years | 10 Years |

| Annual Outflow | Rs. 83,650 | Rs. 1,31,750 |

| Total Outlay | Rs. 12,54,750 | Rs. 13,17,500 |

| Final Lump Sum Return (Maturity Benefit with Guaranteed Additions) | Rs. 27,61,669 | Rs. 25,21,383 |

| Net Compounded IRR | 4.38% | 4.23% |

Who can buy LIC’s New Jeevan Sathi policy?

This policy may suit:

- Extremely conservative investors: People who dislike market-linked products, want guaranteed maturity, and feel more comfortable with the LIC brand.

- Couples looking for simple estate planning: A single policy for both spouses can make nomination, liquidity planning, and family protection a bit easier.

- People who want forced long-term savings: Because early surrender penalties apply, some investors use it as a disciplined savings tool.

Why you should be careful before buying a joint policy?

Joint-life policies may sound attractive, but they come with a few practical drawbacks. Husband and wife often have different incomes, liabilities, and retirement goals, so one combined policy may not fit both needs well. It also reduces flexibility, since separate policies are easier to stop, change, or replace if your situation changes.

Another issue is exit planning. If priorities shift, a separation happens, or one spouse no longer needs cover, a joint policy can become harder to manage. Many buyers also focus only on the maturity value and guaranteed returns, while overlooking surrender value, opportunity cost, and the impact of inflation.

Why LIC New Jeevan Sathi Limited Premium may not appeal to everyone

The bigger concern is returns. An IRR of around 4 to 5 % over 20–25 years may struggle to keep up with inflation. The policy also needs a long commitment and regular premium payments before it delivers meaningful value.

- Sub-inflation returns: An IRR of 4.2% to 4.4% is quite low for a 20–25 year horizon. Since long-term retail inflation is usually around 5% to 8%, returns below 5% can slowly erode your purchasing power over time.

- Low insurance cover: For an annual premium of Rs. 1.31 lakh under Option II, the life cover is only Rs. 10 lakh. For a primary earner, that amount may not be enough to support the family, repay debts, or fund children’s higher education.

- Poor liquidity: If you face a cash crunch and need to exit early, surrendering a traditional policy can be painful. In the early years, you may lose a large part of the premiums you paid.

What About the Single Premium Version of New Jeevan Sathi?

LIC has also introduced a Single Premium version of New Jeevan Sathi for investors who prefer one-time investment instead of paying yearly premiums.

LIC New Jeevan Sathi – Single Premium Illustration:

- Age : 35

- Single Premium Outflow (Base): ₹8,12,750

- Basic Sum Assured: ₹10,00,000

- Guaranteed Addition (GA) Rate: ₹70 per ₹1,000 Sum Assured per annum (Fixed ₹70,000 accrued yearly)

- Policy Term: 20 Years

- Maturity Payout: ₹24,00,000 (₹10 Lakh Sum Assured + ₹14 Lakh accumulated GA)

The expected IRR on single premium version is around 5.56%.

At 5.56%, the Single Premium option generates a structurally better yield than the Limited Premium variant (4.23%). This is because your entire investment amount gets the full 20 years to experience the fixed compounding effect, rather than trickling into the plan year-by-year.

The Single Premium variant may suit investors who have surplus lump sum money and want a one-time guaranteed product without future premium commitments. The Limited Premium version reduces upfront burden by spreading payments over multiple years. However, in both versions, investors should focus on actual returns, liquidity and long-term opportunity cost before investing.

Better alternatives to consider

Depending on your goal, there are often better options than a joint traditional policy.

Buy separate term insurance policies. Each spouse can take enough cover on their own, which usually gives lower cost, higher coverage, and more flexibility. Instead of putting Rs. 1,31,750 a year into LIC New Jeevan Sathi, you could use the same budget much more efficiently.

Step 1: Protection:

Buy two separate pure term insurance plans (if needed), one for each spouse. A Rs. 1 crore cover for a 35-year-old usually costs around Rs. 12,000–15,000 a year, so both spouses may get strong coverage for roughly Rs. 25,000–30,000 a year. That gives you around 10 times more insurance protection.

Step 2: Savings and investment:

Use the remaining Rs. 1 lakh+ for better wealth-building options.

- For guaranteed returns: Consider PPF, VPF, or long-term NSC.

- For long-term wealth creation: Invest in diversified equity mutual funds through SIPs. Over 20–25 years, even a 10%–11% CAGR can build a much larger corpus than a traditional endowment plan.

The key idea is simple: separate protection from investing. That usually gives you more cover, more flexibility, and better long-term growth.

Final Thoughts:

LIC New Jeevan Sathi is a conservative joint-life insurance plan for families who prefer guaranteed returns over high growth. While it offers simplicity and predictable benefits, it is essentially another low-yield traditional savings plan packaged with a “single policy for husband and wife” concept, which is likely to be aggressively marketed. Before investing, compare it carefully with term insurance plus separate investment options.

Continue reading:

- LIC Policy Returns in 2026: How Much Do LIC Policies Really Return?

- What’s in a Name? The Hidden Truth About Children’s Insurance Plans

- Best Mutual Funds for 2026: Picking “Consistency Kings” Over Performance

- List of 20 Best Central Government Schemes for Personal Finance | 2026

(Please note that this article is based on the limited available information and will be edited/updated, if required)

(Post first published on : 128-May-2026)

Join our channels