If you’ve ever bought a LIC policy — or are thinking about buying one — you’ve probably heard lines like:

“It’s safe.”

“You’ll get good returns.”

“At least you’ll get something back.”

Over the last 10+ years, I’ve interacted with thousands of investors and policyholders. And one thing keeps coming up again and again—Most people don’t actually know how much their LIC policy returns. Not the maturity amount, not the bonus figure, but the actual annual return.

So in this article, let’s talk about that — calmly, with numbers, not sales talk.

For this analysis, I’ve considered all traditional LIC plans available for purchase as of Jan 2026.

I’ve intentionally excluded term insurance plans (as they don’t have an investment component) and ULIPs (since their returns are market-linked and difficult to estimate reliably).

I’m using XIRR for this analysis, as it captures the real annualized return by considering both the timing of premiums and the final payout.

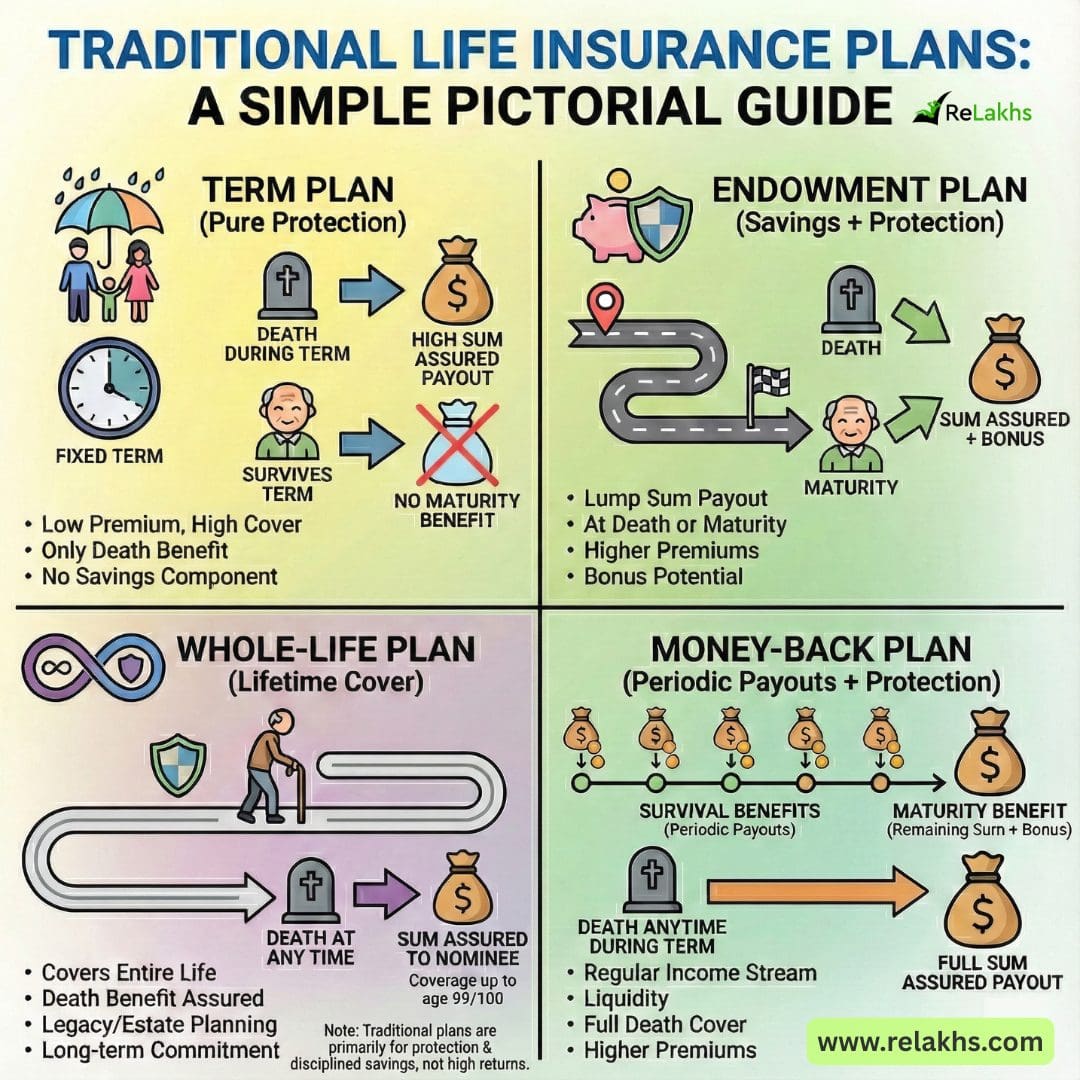

In case you’re not fully clear about what traditional life insurance plans are, here’s a quick recap. Below are the popular types of conventional or traditional life insurance policies in India;

- Money-back Life insurance plans

- Endowment life insurance policies

- Whole-life plans

What is an Endowment plan? – An endowment plan combines insurance and savings. The policyholder receives a lump sum along with bonuses (if any) on maturity or on death during the policy term.

What is an ‘Whole-Life Insurance Plan’? – It is a life insurance policy which is guaranteed to remain in force for the insured’s entire lifetime. The Sum assured is paid to the Policyholder’s nominee in the event the insured dies.

What are Money-back policies? – Money-back policies provide life cover during the policy term and pay maturity benefits in installments through periodic survival benefits.

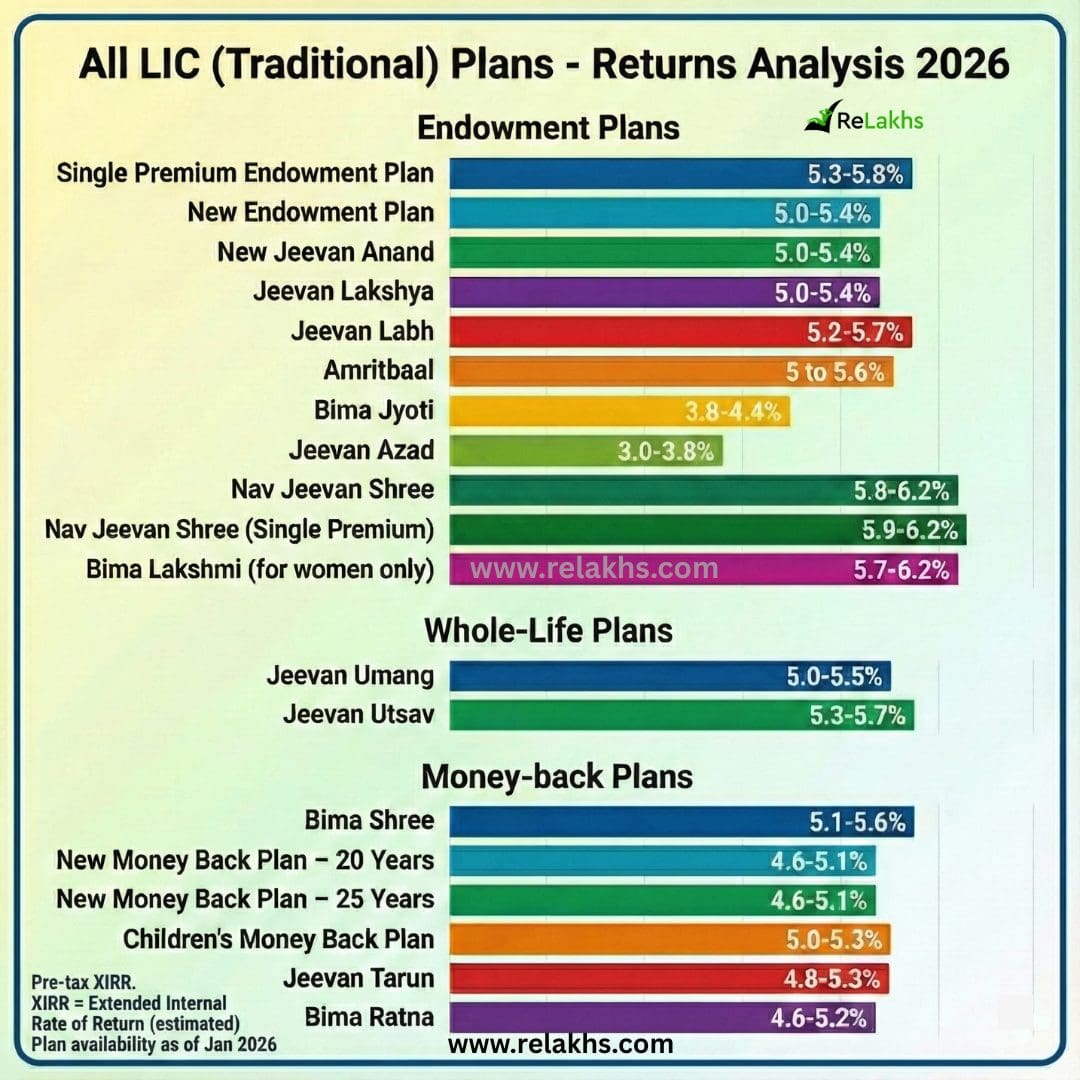

All LIC Plans Returns Analysis 2026

So..How Much Do LIC Policies Really Return?

Based on current LIC illustrations, prevailing bonus trends, and realistic assumptions (non-smoker, regular premium, full term), here’s what most policyholders are likely to earn as of Jan 2026.

| LIC Plan Name | Plan Type | Most Likely XIRR (%) |

|---|---|---|

| Single Premium Endowment Plan | Endowment Plan | 5.3 – 5.8 |

| New Endowment Plan | Endowment Plan | 5.0 – 5.4 |

| New Jeevan Anand | Endowment Plan | 5.0 – 5.4 |

| Jeevan Lakshya | Endowment Plan | 5.0 – 5.4 |

| Jeevan Labh | Endowment Plan | 5.2 – 5.7 |

| Amritbaal | Endowment Plan | 5.0 – 5.6 |

| Bima Jyoti | Endowment Plan | 3.8 – 4.4 |

| Jeevan Azad | Endowment Plan | 3.0 – 3.8 |

| Nav Jeevan Shree | Endowment Plan | 5.8 – 6.2 |

| Nav Jeevan Shree (Single Premium) | Endowment Plan | 5.9 – 6.2 |

| Bima Lakshmi (for women only) | Endowment Plan | 5.7 – 6.2 |

| Jeevan Umang | Whole-Life Plan | 5.0 – 5.5 |

| Jeevan Utsav | Whole-Life Plan | 5.3 – 5.7 |

| Bima Shree | Money-back | 5.1 – 5.6 |

| New Money Back Plan – 20 Years | Money-back | 4.6 – 5.1 |

| New Money Back Plan – 25 Years | Money-back | 4.6 – 5.1 |

| Children’s Money Back Plan | Money-back | 5.0 – 5.3 |

| Jeevan Tarun | Money-back | 4.8 – 5.3 |

| Bima Ratna | Money-back | 4.6 – 5.2 |

Please Keep These Tax Rules in Mind

Before looking at returns, it’s important to understand how tax rules can change your actual, in-hand XIRR.

For all traditional life insurance plans (excluding ULIPs), if the total annual premium across all your policies exceeds ₹5 lakh, the maturity proceeds become taxable as per your income tax slab. This taxation can reduce your effective, in-hand XIRR by 1–2%, depending on your slab.

Many single premium plans (for example, the Single Premium Endowment Plan – 717) typically offer life cover of only 1.25× the premium. Because of this, the maturity amount becomes taxable under Section 10(10D). To keep the maturity tax-free, the policy must provide minimum life cover of 10× the premium — for example, by choosing Option 2 (10× cover) in plans like Nav Jeevan Shree.

Want to calculate how much your money-back or endowment policy is really earning? I’ve written detailed articles that explain exactly how to calculate the returns yourself.

So, Does That Mean LIC Policies Are Bad?

Not really. But they are often misunderstood — and mis-sold.

LIC’s traditional policies can make sense in certain situations, especially if:

- You’re looking for guaranteed, low-risk returns, tax-free maturity benefit (in most cases, subject to premium and cover conditions).

- You prefer discipline and predictability over chasing higher returns.

- You’re comfortable knowing that returns will be low to modest.

However, they may not be the right fit if:

- You’re aiming for long-term wealth creation.

- You believe insurance itself is an investment.

- You haven’t compared them with a combination of term insurance and separate equity/debt investing.

The key isn’t whether LIC policies are “good” or “bad” — it’s whether they match your expectations and goals.

Try calculating the XIRR of your own policy or before making your next insurance or investment decision. Use this analysis as a reference — not a recommendation.

Continue reading:

- LIC Fixed Deposit Scheme? Does LIC offer FD Scheme?

- Calculate Rate of Return on Investments using XIRR function

- Term Insurance : Is it just a waste of your money?

- Why (NOT) to buy Return of Premium Term Life Insurance Plans?

Disclaimer: Returns shown are estimated maturity XIRR based on current LIC illustrations (Jan 2026). Actual returns may vary depending on age at entry, policy term, bonus rates, Sum Assured amount and premium payment mode. Money-back plans typically deliver a lower effective IRR due to intermittent payouts.

(Post first published on : 9-Jan-2026)

Join our channels