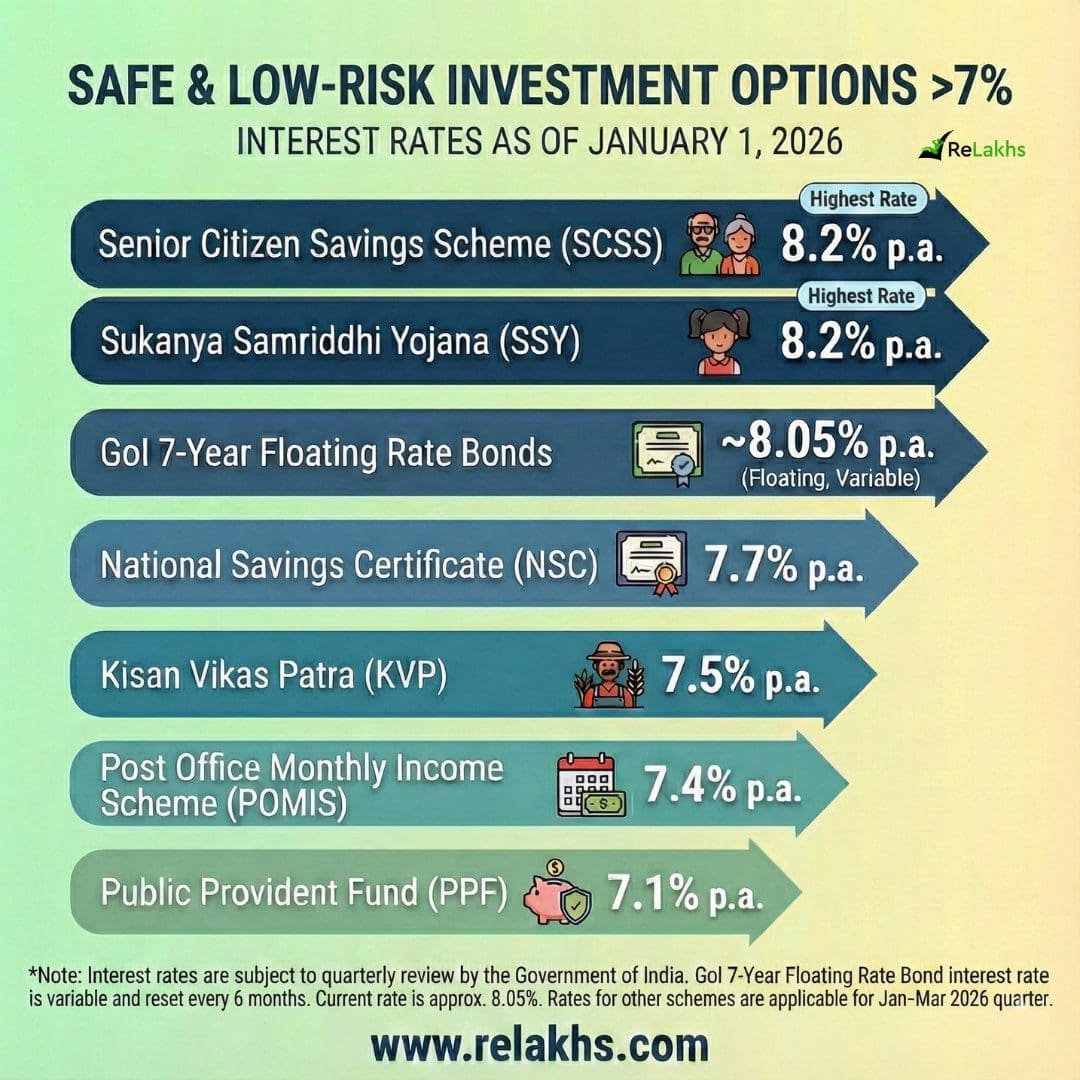

The other day, I shared a post on safe and low-risk, government-backed investment options for conservative long-term investors, along with the latest interest rates as of January 2026.

Soon after, I received a very common and important question from one of my followers:

“If the government reviews small savings interest rates every quarter, does that mean the interest on all these schemes keeps changing every quarter?”

It’s a completely valid doubt.

We often hear that small savings schemes (PPF/NSC/Sukanya Samridhi etc.,) rates are reviewed quarterly, and it’s easy to assume that every scheme’s return will go up or down whenever the government revises rates. But that’s not how all schemes work.

Here’s the important part most investors miss 👇

While rates are reviewed every quarter, the impact of those changes depends on the type of scheme you invest in.

- Some schemes lock the interest rate on the day you invest and stay unchanged till maturity.

- Others continue to change, and any rate revision applies even to your existing balance.

This difference can completely change how predictable your returns are — especially if you’re investing for stable income or long-term planning.

So I thought it would be useful to write this article and clearly explain:

- Which small savings schemes offer fixed returns

- Which ones have variable returns

- And how quarterly rate revisions actually affect your money

Let’s break it down in simple terms.

Do Small Savings Interest Rates Change Every Quarter? Fixed vs Variable Returns Explained

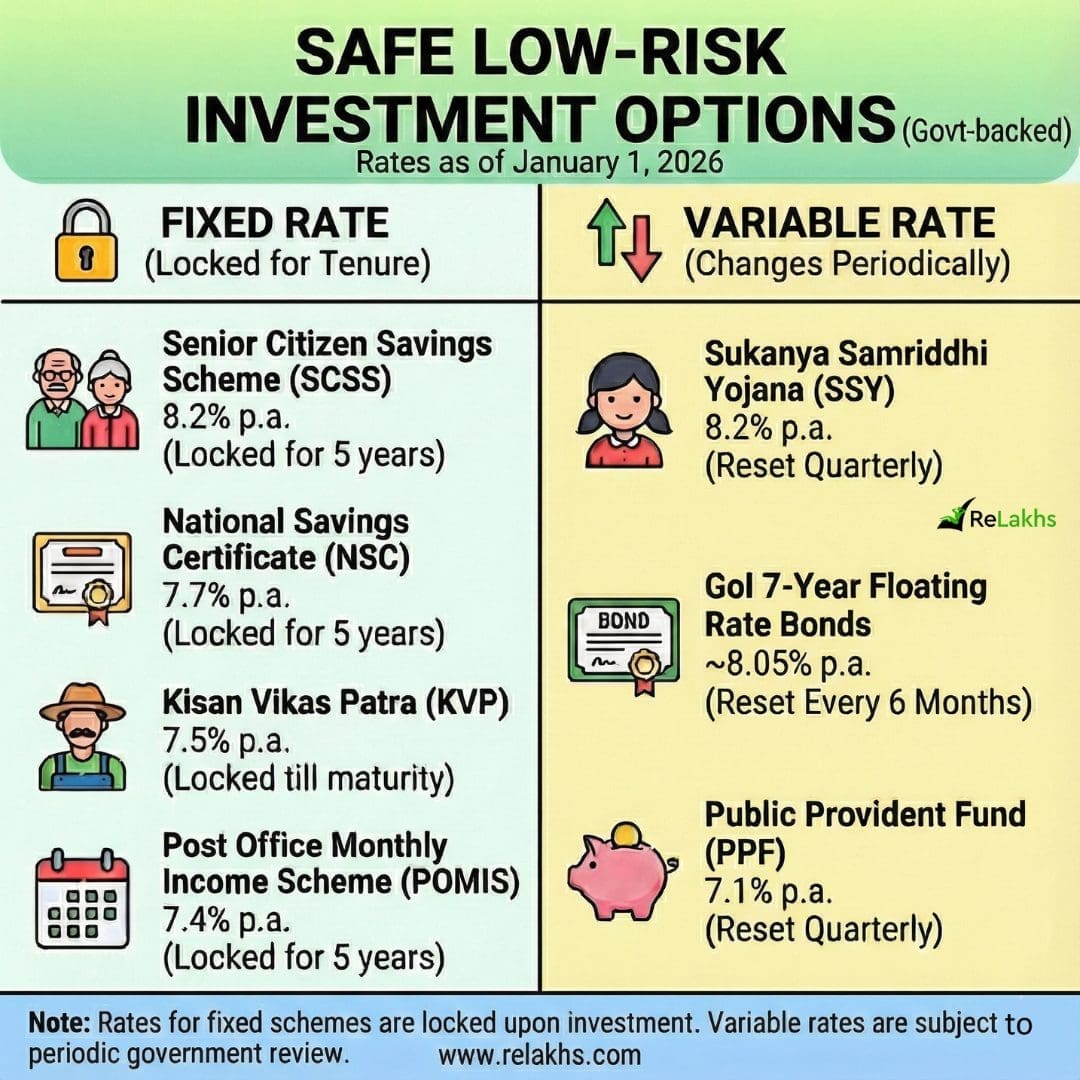

We can broadly divide government-backed small savings schemes into two categories based on how their interest rates behave after you invest:

- Variable-rate schemes – Rates can change even after opening the account

- Fixed-rate schemes – Rates are locked at the time of investment

Variable Rate Small Savings Schemes

In these schemes, the interest rate is not locked. The government reviews the rate periodically, and any change applies to your existing accumulated balance as well.

- Public Provident Fund (PPF)

Reviewed every quarter. Any rate change applies to the entire accumulated corpus. - Sukanya Samriddhi Yojana (SSY)

Also reviewed quarterly. Like PPF, revisions impact the full balance. - GoI 7-Year Floating Rate Bonds

- Rate resets every 6 months (Jan 1 & Jul 1).

- The interest is always 0.35% above the prevailing NSC rate.

- As of January 2026, the rate is 8.05% p.a. (7.7% NSC + 0.35%).

In short: Your return moves up or down with government rate changes.

Fixed Rate Small Savings Schemes

Here, the interest rate applicable on the day you open the account is locked for the entire tenure. Future rate cuts or hikes do not affect your investment.

- Senior Citizen Savings Scheme (SCSS)

Rate locked for 5 years. - National Savings Certificate (NSC)

Rate locked for 5 years. - Kisan Vikas Patra (KVP)

Rate locked till maturity (~115 months). - Post Office Monthly Income Scheme (POMIS / MIS)

Rate locked for 5 years.

In short: What you lock is what you earn.

| Low-Risk Investment Option | Interest Type | Reset Frequency |

|---|---|---|

| Senior Citizen Savings Scheme (SCSS) | Fixed | Locked for 5 years |

| National Savings Certificate (NSC) | Fixed | Locked for 5 years |

| Kisan Vikas Patra (KVP) | Fixed | Locked till maturity |

| Monthly Income Scheme (POMIS) | Fixed | Locked for 5 years |

| PPF | Variable | Quarterly review |

| SSY | Variable | Quarterly review |

| GoI Floating Rate Bonds (7 years) | Variable | Every 6 months |

Real-Life Example: ₹10 Lakh — Fixed vs Variable Interest Rate

Let’s assume you invest ₹10 lakh on January 1, 2026.

Case 1: Fixed-Rate Scheme (Post Office MIS joint account at 7.4%)

- Investment: ₹10,00,000

- Interest rate locked: 7.4% p.a. for 5 years

- Annual interest: ₹74,000

- Monthly income payout: ~₹6,167

Even if the government cuts MIS rates to 6.8% next quarter, your monthly income remains ₹6,167 for the entire 5-year tenure.

So, you’ll get predictable income every month with no impact from future rate changes since your interest rate is locked in for the full 5-year tenure.

Case 1: Variable Interest Rate Scheme (Public Provident Fund @ 7.1% pa)

- Investment: ₹10,00,000

- Starting rate (Jan 2026): 7.1% p.a.

- Interest for Year 1: ₹71,000

Now assume government revises rates as follows:

- Year 2: 6.9%

- Year 3: 7.3%

Your interest changes every year, and each new rate applies to the entire accumulated balance.

With PPF, you benefit if interest rates rise in the future since your contributions lock in higher rates applicable at the time of deposit. However, returns effectively fall when rates are cut, as newer investments earn less and there’s no upward adjustment on past balances

To sum it up;

- Looking for stable income or predictability → Fixed-rate schemes like SCSS, MIS, NSC & KVP

- Investing for long-term wealth and tax efficiency → Variable-rate schemes like PPF, SSY

- Need stable income (semi-annually) → Variable-rate → Govt of India Floating Rate Bonds

Understanding this distinction will help you choose the right product for your goals, instead of being surprised by future rate changes.

Continue reading:

- New EPF Withdrawal Rules 2025-26 | Big Relief, Bigger Responsibility for 30 Crore Subscribers

- LIC Fixed Deposit Scheme? Awareness Post (Does LIC offer a fixed deposit scheme?)

Interest rates mentioned are applicable for the January–March 2026 quarter and are subject to government review.

(Post first published on : 5-Dec-2026)

Join our channels