LIC Jeevan Utsav Single Premium (Plan No. 883) was launched in January 2026 as a single-premium variant of LIC’s non-linked, non-participating whole life plan. It offers guaranteed additions and a lifetime income option under a one-time premium structure.

It is being marketed as a “10% income for life” product. But what does that actually mean in terms of real returns? Is it truly a double-digit return product — or does the actual IRR tell a different story?

In this detailed review, we break down:

- How the plan works

- Key features and structure

- Real IRR (Internal Rate of Return) calculation

- Who should consider investing

- Who should avoid it

Let’s decode it step by step.

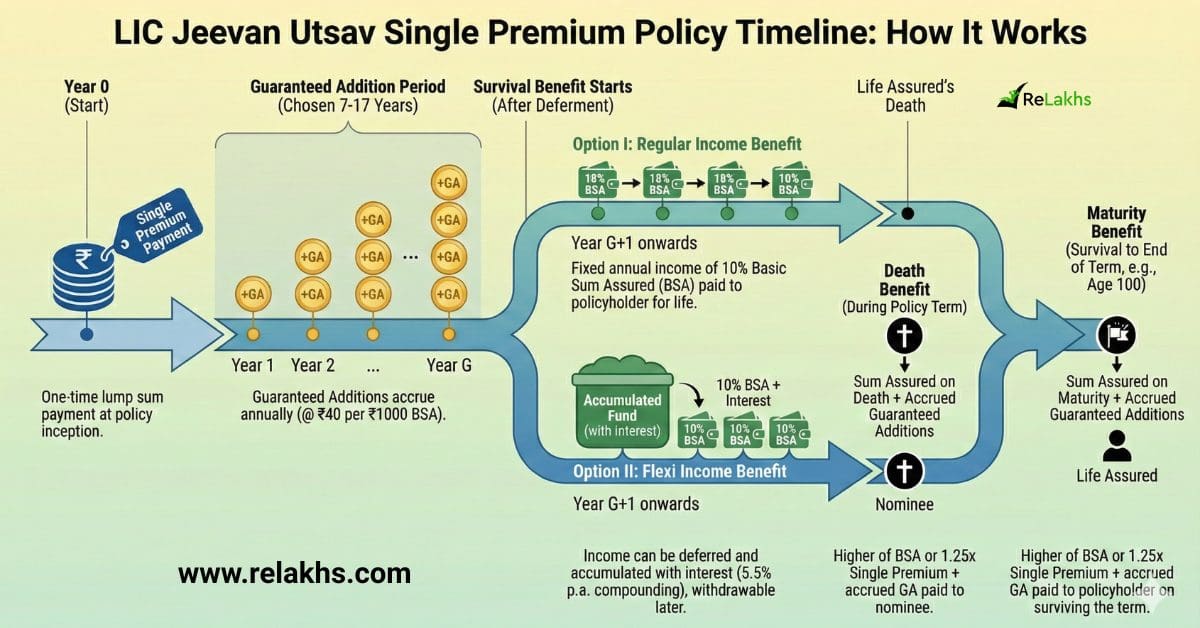

Key Features of LIC Jeevan Utsav (Single Premium)

- It is a Whole Life Plan (maturity at age 100)

- One-time single premium payment

- Guaranteed Additions (GA) of ₹40 per ₹1,000 Basic Sum Assured is payable during chosen Guaranteed Addition Period (7 to 17 years)

- Minimum Basic Sum Assured- ₹5,00,000

- Two Income Options;

- Option I – Regular Income

- 10% of Basic Sum Assured paid annually

- Starts after GA period ends

- Continues till death or age 100

- Option II – Flexi Income

- 10% of Basic Sum Assured accrues

- Accumulates at 5.5% p.a.

- Can withdraw partially upto 75% accumulated balance

- Balance payable at death/maturity

- Option I – Regular Income

LIC Jeevan Utsav – New Single Premium Whole-Life Plan – How it Works?

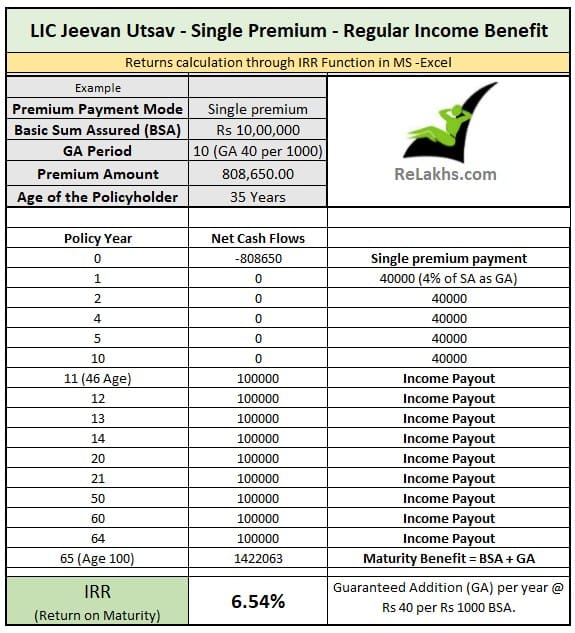

Let’s understand the structure using the brochure illustration. Assume a 35-year-old investor chooses a Basic Sum Assured of ₹10,00,000 with a Guaranteed Addition (GA) period of 10 years. The one-time single premium payable is ₹8,08,650. Under Option I (Regular Income Benefit), the policy pays 10% of the Basic Sum Assured — that is ₹1,00,000 per year — as annual income.

Since the GA period is 10 years, there is no income during the first 10 policy years. During this period, guaranteed additions accrue annually. The income starts from the end of Year 11 and continues every year thereafter.

The policy runs till age 100, which means a total term of 65 years in this example. At maturity (end of Year 65), the life assured receives the maturity benefit of ₹14,22,063, which represents the Basic Sum Assured plus accrued Guaranteed Additions.

So effectively, the cash flow looks like this: a single outflow of ₹8,08,650 at the beginning (Year 0), no inflows for the first 10 years, ₹1,00,000 per year from Year 11 onwards, and finally the maturity amount of ₹14,22,063 at the end of the 65th year (100 years of policyholder’s age).

LIC Jeevan Utsav Single Premium Plan – Real Returns Explained

Now comes the important part. Many people assume: ₹1,00,000 ÷ ₹8,08,650 ≈ 12.36%

But that is simple yield, not return.

A true IRR calculation properly accounts for the 10-year deferment period, during which no income is received despite the premium being fully paid upfront. It also considers the entire 65-year duration of the policy, right up to age 100 in this example. Most importantly, IRR factors in the time value of money, meaning that cash received decades later is worth less than money received today. Because of these three factors, the actual return is very different from the simple annual payout percentage often highlighted in sales conversations.

Below is the IRR calculation for the Regular Income Benefit option, assuming the policyholder survives until 100 years of age.

This confirms that for an individual entering at age 35 and holding the policy until maturity (age 100), the annualized return is approximately 6.54%.

Important Points to Ponder Before Investing

- Return depends on life expectancy: If survival is assumed till age 100, the IRR works out to roughly 6–6.5%. However, if life expectancy is closer to 80 years, the IRR falls meaningfully because the number of income payouts reduces and there is no maturity benefit at 100.

- 10% income is not 10% return: The plan pays 10% of the Basic Sum Assured as income, but this is not the return on your premium. Actual returns are much lower when calculated using proper IRR methodology.

- Guaranteed Additions do not compound: The GA accrues during the selected period, but there is no compounding on these additions. They accumulate in a simple manner, which limits overall growth.

- Tax implications must be reviewed: Since this is a single premium policy, recent tax rules may impact exemption eligibility depending on premium amount and overall structure. Check tax treatment carefully before investing.

- Avoid misleading yield calculations: Dividing annual income by premium (for example, ₹1,00,000 ÷ ₹8,08,650 ≈ 12%) is not a valid return calculation. A proper IRR must account for the deferment period and the time value of money.

- Consider opportunity cost: Locking money for decades at ~6% return means you may be foregoing higher long-term growth from diversified investments.

Who Can Consider Investing?

- Conservative investors who prefer predictable, guaranteed income and do not want exposure to market volatility.

- Retirees looking for fixed cash flow, especially those purchasing the plan at age 50 or above and seeking stable annual income.

- Investors who have already secured adequate term insurance, have equity investments for growth, and now want a guaranteed component in their portfolio for stability.

- Individuals considering estate planning, since the policy provides a death benefit and a maturity benefit payable at age 100.

Who Should NOT Invest?

- (Young) Investors seeking high growth, as a ~6% long-term return may not meaningfully beat inflation over decades.

- Individuals with inadequate term insurance, since investment-oriented insurance plans should not replace pure protection needs.

- Investors expecting 10–12% returns, because this is not an equity substitute and does not generate double-digit compounded returns.

- Liquidity-focused investors, as the money is largely locked in for the long term with limited flexibility.

- Those ignoring opportunity cost, especially younger investors who could potentially aim for higher long-term growth through diversified equity investments or growth assets.

LIC Jeevan Utsav Single Premium is best viewed as a long-term, guaranteed income product — not a high-return investment. While the “10% income” may sound attractive, the actual return works out to around 6–6.5% if one assumes survival till 100, and lower if life expectancy is shorter. The plan offers stability, predictability, and insurance cover, but at the cost of liquidity and long-term growth potential.

Before investing, align it with your overall financial plan — ensure adequate term insurance, understand the real return, and compare it with alternative investment options. The key is not whether the plan is good or bad, but whether it fits your financial goals and risk profile.

Continue reading:

- LIC Policy Returns in 2026: How Much Do LIC Policies Really Return?

- What’s in a Name? The Hidden Truth About Children’s Insurance Plans

- Best Mutual Funds for 2026: Picking “Consistency Kings” Over Performance

- List of 20 Best Central Government Schemes for Personal Finance | 2026

(Post first published on : 11-Feb-2026)

Join our channels