It is surprising that how a simple question like – “Are you satisfied with your take-away salary?” can make 70% of the people answer in a resounding ‘NO’. They believe that even after working with a lot of dedication and perseverance, the pay they receive is demotivating. If you are one of those people too, you should remember that your salary structure and your take-home pay are based on what the firm offers with you having very little control. You can’t really help all those deductions, can you?

Well, things aren’t completely out of your control. Many companies now offer employees the flexibility to structure their salary. Salary restructuring could help employees reduce their tax liability, thus increasing their in-hand salary. So, yes, there are a lot of ways through which you could limit your deductions, increasing your overall net salary.

Excited already? Well, so let’s not waste your time anymore by making you day-dream about your increased salary, and let’s actually help you convert those dreams to reality. Read on to know the five practical tips that could boost your take home salary!

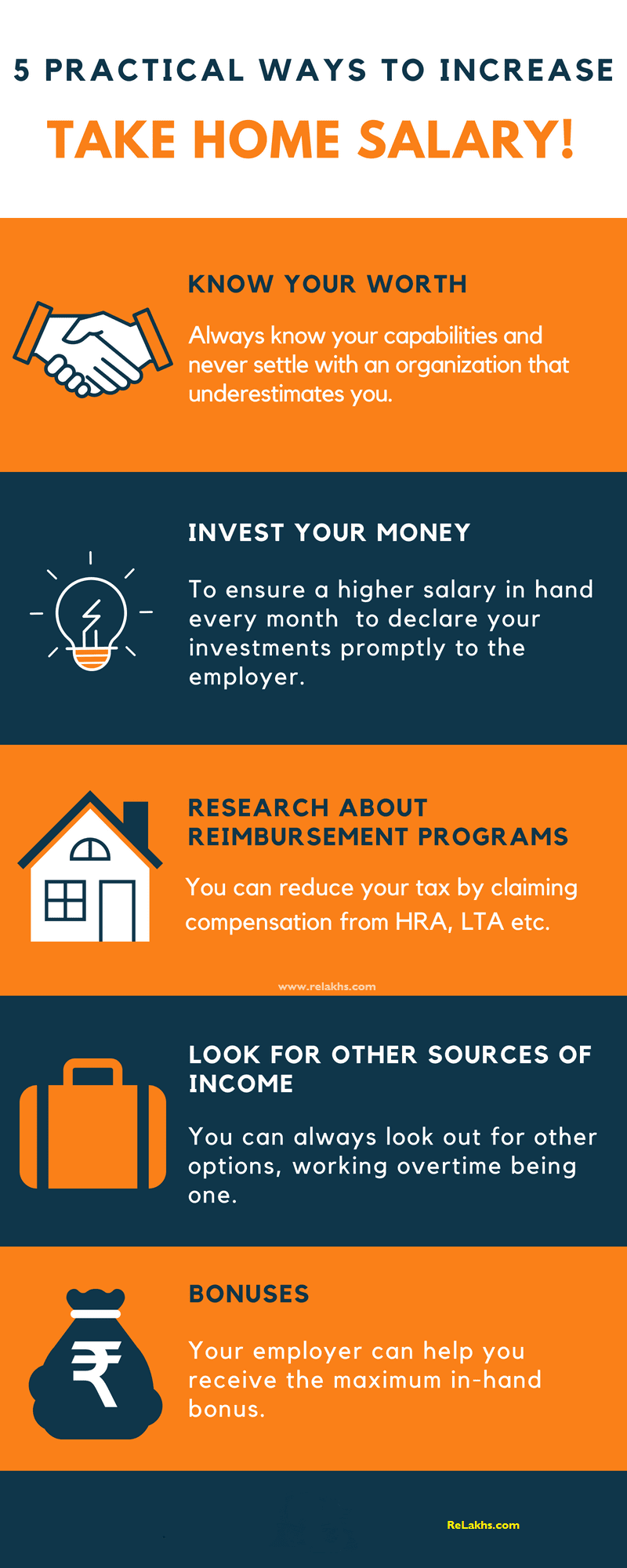

How to increase your Take Home Salary? (5 Practical ways)

Know your worth

Always know your capabilities and never settle with an organization that underestimates you. If you’ve been working with a company for over two years, and still not getting what you truly deserve, you seriously need to do some thinking. Frequent job changes no longer hold the same stigma they once did. If a job is not paying you a fair salary, don’t be afraid to switch jobs.

However, do not make and act on impulsive decisions. You could first look for a better position within the same company, or have a talk with your employer regarding your salary. Talk to your boss about what you can do to add more value, and quantify that value in terms of a salary increase. Do the extra work, and then ask for a meeting several months later to evaluate your progress

A merit raise will probably only boost your take home pay up to a limited amount. Landing a new position, however, is likely to increase your pay much more.

Take courses to improve your skill set. You can often get reimbursed for them by your company through its educational reimbursement program. By doing this you’ll put yourself in a position to qualify for a higher-paying job in the future.

Invest your money

Under the corporate model, employer’s contribution towards National Pension System (NPS) or EPF are eligible for tax deduction. The employer’s contribution to NPS of up to 10 per cent of basic plus DA is allowed for deduction under section 80CCD (2). This is in addition to the limit of Rs.1.5 lakh of section 80C as well as exemption up to Rs. 50,000 for self-contributions to NPS allowed under Section 80CCD(1B). Other schemes like PPFs (Public provident Funds) also help you axe tax and reap great benefits.

However, do not forget the basic rule: Invest only when you are not in debt and if it meets your investment objectives/goals. Hence, you should carefully prioritize your money. If you have an education loan running, paying it back should be your priority. You get a tax benefit under Section 80E for paying the interest back. Financial planners suggest prepaying a loan after the moratorium period rather than investing as there will be no prepayment charges.

One effective way to ensure a higher salary in hand every month is to declare your investments promptly to the employer at the beginning of the financial year. This will enable the employer to consider these investments before he arrives at your tax liability and the TDS deductible every month. This will help in a lower TDS every month ensuring a higher take home.

Related Articles :

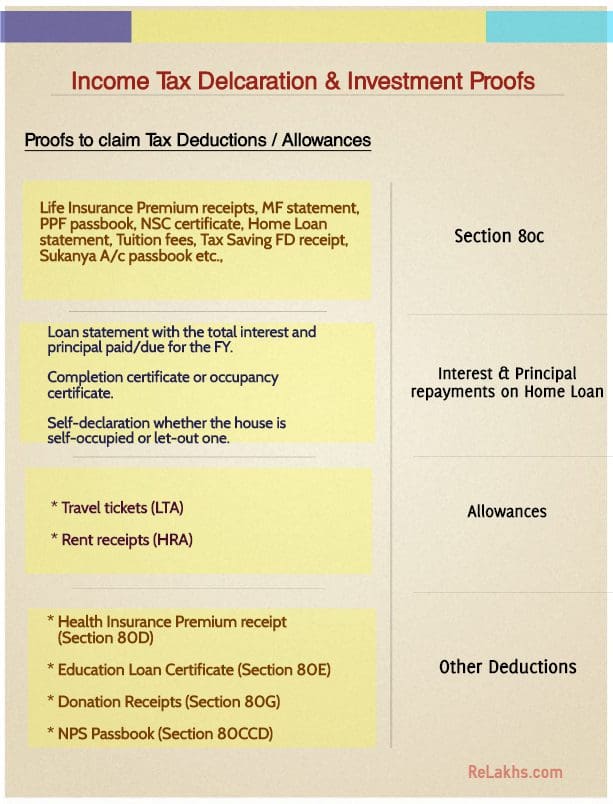

- Income Tax Declaration & List of Investment Proofs

- Income Tax Deductions List FY 2018-19 | List of important Income Tax Exemptions for AY 2019-20

Research about reimbursement programs.

Here are the components of your salary and how you can claim compensation on them to reduce paying taxes:

- House Rent Allowance or HRA

If you are a salaried employee and you pay rent on your house, you can claim HRA to reduce paying taxes on your house rent. Amount paid on house rent enjoy partial tax exemption. You can claim an exemption on paying taxes for both, your house rent as well as your home loan repayments (if any). If you are staying in a rented house and making repayments on another home/property, you can claim for tax benefits on both, even if both the houses are located in the same city. Furthermore, if you are paying rent to your parents for living in their house, you can claim HRA deduction for this rent if your parents own the house/property.

Related Article : Understanding Tax Implications of Income from House / Property

- Leave Travel Allowance or LTA

LTA is another component of your salary, and you can easily find it on your salary slip. This allowance can be used to reduce the amount of tax you have to pay. However, what you must remember here is that, LTA applies to travel within India only. If this component is available in your salary break-up, you can claim for LTA for 2 journeys in a span of 4 calendar years. To add to this, you should also understand how your salary slip works to maximise tax benefits & allowances.

- Reimbursements

You can lower your tax deductions significantly by claiming reimbursement for expenses incurred by you in the form of telecom expenses, fuel charges, driver expenses, purchases of books and periodicals necessary for your job, food coupons, etc.

Look for other sources of income

You can always look out for other options – working overtime being one. If you can manage well, working overtime also creates a good impression on your employer, boosting your salary at the same time.

Also, you could look for a side job (provided this is within the scope of your employment agreement). You could consider taking up your hobby and making it chuck in a few bucks for you. For an instance, if you are into designing, you could become a freelancer designer, working according to your own conditions. This will not only provide an escape from the daily office life, but will also give you time to pursue you passion. Moreover, if you’re also earning money along with it, does it not sound like a win-win situation?

Bonuses

More often than not, employers hand over any applicable bonus to employees after deducting the tax beforehand. Therefore, if you provide your employer with details of your tax-saving investment, they can help you receive the maximum in-hand bonus. If you do not follow this procedure, then you will have to claim for a refund on the tax paid on your bonus at the time of filing your Income Tax Return.

After going through all the tips, we are sure you’re getting restless to implement them and finally get an increased take-away salary! So, get going with all the good luck, and you can thank us later guys!

This is a guest post by Sanjeev Sharma of Sqrrl.in.

About the author:

This information piece has been written by Sanjeev Sharma, co-founder of Sqrrl Fintech, and having over 17 years of experience in the world of Finance. He’s had past stints with Franklin Templeton, AIG Investments, and PineBridge Investments, across strategy, sales, business development & advisory.

Continue reading :

- Resignation : Employee Benefits & Personal Finances – Checklist

- Leave Encashment & Tax Implications

- 13 FAQs on Gratuity Benefit Amount & Tax Implications

- Understanding your Form 16 & other Tax related forms (Form 16A & Form 26AS)

Kindly note that ReLakhs.com is not associated with Sqrrl Fintech. This is a guest post and NOT a sponsored one. We have not received any monetary benefit for publishing this article. The content of this post is intended for general information / educational purposes only.

(Post first published on : 03-July-2018)

Join our channels

Indeed a nice post to have come across, I must admit that you have done a great work

A another great option to double the income is to invest and trade in stock market specially in stock future segment. But as a beginner, gather proper knowledge and research about trading, and than slowly increase the profit and investment amounts.