We receive income through different ways, it can be your Salary, Dividend income from mutual funds or stocks, commission, rent, interest on your Bank Fixed Deposits / Securities etc.,

The providers of these incomes (like your company / bank) can deduct a certain percentage of income as TDS (Tax Deducted at source) based on certain threshold limits.

TDS or tax deducted at source is a process of collecting Income Tax at source by the GOI (Government of India). It is a deduction of tax from the original source of income. It is essentially an indirect method of collecting tax which combines the concepts of “pay as you earn” and “collect as it is being earned.”

TDS is calculated and levied on the basis of a threshold limit, which is the maximum level of income after which TDS will be deducted from your future income/payments.

It is deducted as per the Indian Income Tax Act, 1961. TDS is controlled by the Central Board for Direct Taxes and it is a part of the Indian Revenue Service Department.

Let us understand about TDS with an example;

You book a Bank Fixed Deposit for Rs 10 Lakh for 1 year @ 10% pa interest rate. You will earn an interest income of Rs 1,00,000 after one year. Your Bank may deduct TDS at the rate of 10% i.e., Rs 10,000 (10% of Rs 1,00,000) and deposits this Rs 10,000 with Income Tax Department (on behalf of you). Bank issues you a TDS certificate which reflects this deduction. (Read : ‘Understanding your Form 16A‘)

Besides interest income earned on bank deposits, TDS is levied on various incomes & expenditures. Salary income, lotteries, interest income from post office, insurance commission, rent payment, early EPF withdrawals, sale of immovable property, rent payments on property etc., fall under the ambit of TDS.

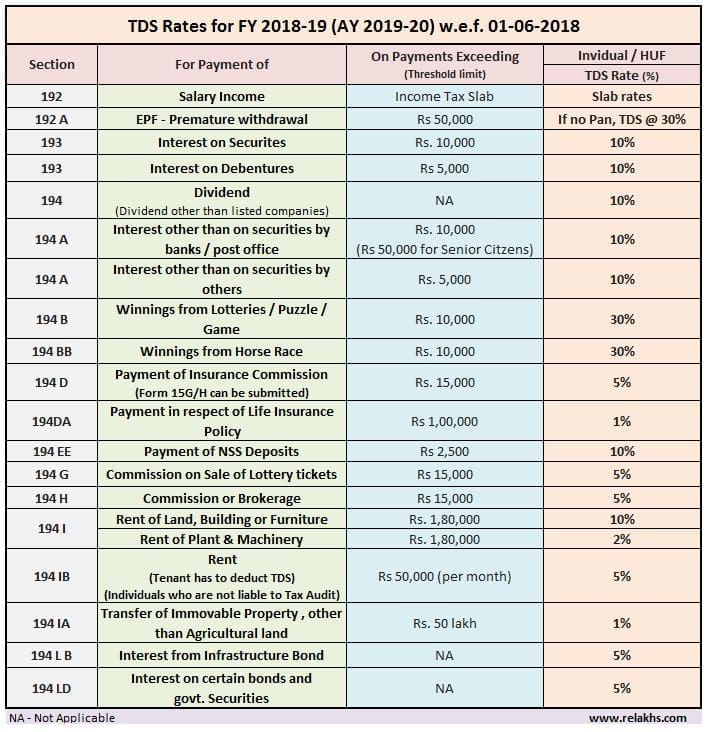

Latest TDS Rates Chart for Financial Year 2018-18 (Assessment Year 2019-20)

Based on the Financial Act 2018-19, following are the proposed / revised TDS threshold limits & rates of TDS applicable for the FY 2018-19 (AY 2019-20).

Kindly be aware of the below important points ;

- Budget 2018-19 has proposed to raise the threshold for deduction of tax at source on interest income of Bank / Post office / Co-operative Bank deposits for senior citizens from Rs 10,000 to Rs 50,000. This is applicable for FY 2018-19 / A 2019-20.

- Under Section 193, the exemption limit of interest paid on debentures is Rs 5,000. The thresh-hold limit of interest on 7.75% GOI savings (Taxable) bonds which has replaced the earlier 8% Savings (Taxable) Bonds, 2003 is Rs 10,000 (this amendment will be w.e.f 01-Apr-2018).

- Section 194 DA is applicable only where amount paid under a life insurance policy is not exempt u/s. 10 (10D).

- For Resident Indians, Health & Education Cess @ 4.0% shall be levied on Income Tax. For NRIs, Health & Education Cess @ 4.0% will be applicable on TDS in respect of all payments.

- TCS (Tax Collected at Source) is applicable on purchase of Motor vehicle worth more than Rs 10 Lakh. (Section 206 C – IF)

- 1% TCS on cash purchases of above Rs 2 Lakh has been removed. However, 100% penalty is now applicable on Cash transactions (including jewelry purchases) exceeding Rs 2 lakh (Related Article : ‘Rs 2 Lakh Cash Transaction Limit – Penalty Details & Examples‘)

(Difference between TDS & TCS : TDS = Tax Deducted at Source i.e. deducted by PAYER or BUYER. e.g. Employer making salary payment or buyer of immovable property or person paying interest or commission or rent would deduct TDS and pay to the IT department. TCS = Tax Collected at Source i.e. collected by RECEIVER or PAYEE or SELLER. e.g. A Car Dealer selling motor car can collect TCS and pay to the IT department.)

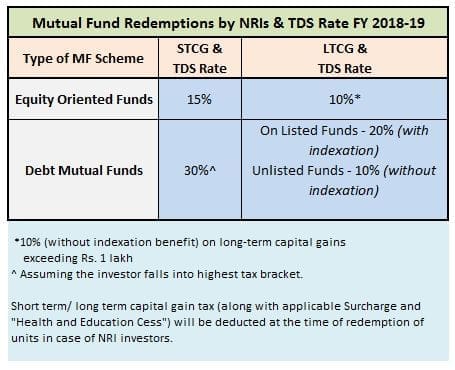

NRIs & TDS Rates

- Interest earned on Non Resident Ordinary Account (NRO) is taxable. A TDS of 30% is applicable on it. But interest earned on Non Resident External (NRE) accounts and Foreign Currency Non Resident (FCNR) accounts is not taxed in India. Therefore there is no tax deducted at source.

- NRI Investments in Shares / Mutual Funds -Below are the TDS rate applicable on MF redemptions by NRIs for AY 2019-20.

- An education cess of 4% is applicable to all the TDS.

- Under Section 195, when an NRI sells property, the buyer is liable to deduct TDS @ 20% on Long Term Capital Gains. In case the property has been sold before 2 years (reduced from the date of purchase) a TDS of 30% shall be applicable (on Short Term Capital Gains).

- The rate of TDS will be determined as per rules of Income Tax Act 1961 and DTAA with residence country of the policy holder if it has been signed. (Related Article : ‘What is Double Taxation Avoidance Agreement (DTAA)? | Is Income earned outside India Taxable?‘)

Misconceptions on Tax Deducted at Source (TDS)

One of the biggest misconceptions that exist in the mind of many honest taxpayers is that since they receive their salary/ other payment after deduction of Tax at Source (TDS) and thus they are not required to file their Income Tax return (ITR), assuming that their tax liability has been discharged. Following are some of the common misconceptions on TDS;

- No TDS means no Tax liability : There is a common misconception / myth that if there is no TDS then the schemes (or) investments are tax-free.

For example – If an employee withdraws his EPF money before 5 years of service and if the withdrawal amount is less than Rs 50,000 then TDS is not applicable.

But, this does not mean that the withdrawal is Tax-free. It is just that there is no need for an employer/EPFO (Deductor) to deduct TDS on these types of withdrawals. However, the onus of paying taxes (if any) on this EPF amount lies with the employee.

So, whether it is EPF withdrawals within 5 years or National Savings Certificates (5 year tenure) or any other investments, the interest income is taxed until and unless it is specifically mentioned that the income from that scheme is tax free. For example PPF enjoys tax benefit for which its interest is non-taxable. (Related Article : ‘Tax treatment of various financial investments‘)

- TDS deduction removes tax liability completely

- It’s a misconception that, if the employer has deducted TDS, you need not worry about filing your income-tax return. Your employer deducts TDS on your salary income only, whereas you may have income from other sources (like interest income from Bank Deposits, rental income etc.,) and you have to include those in your Tax Returns. (Related Article : ‘TDS deducted by Employer but not Deposited? How to check TDS details online?‘)

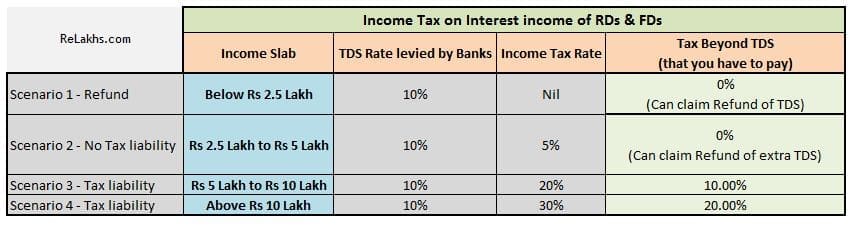

- Another misconceptions is – ‘No additional Income Tax is payable, if taxes are already deducted (TDS) on income’. Actually, depending on nature of income, TDS rates vary. On salaries, employers adjust the rate such that the entire tax liability of the employee is deducted by the year-end. On fixed deposit interest, banks charge TDS at 10%. But if the deposit holder does not provide his PAN, banks deduct tax at 20 per cent.

If your income tax slab rate is different to that of the TDS rate then you may have to pay the ‘balance tax’ or in some cases you can claim ‘refund’ too. It is advisable to be aware of TDS rates on various incomes that you have.

The TDS rate can be say 10% , whereas your are in the 20% tax slab, in this case you have to pay the differential tax (this can be Advance Tax or Self-Assessment Tax). If you are not a tax assessee then you can claim the TDS amount as refund by filing your Tax Returns. If you are in 10% tax bracket and the TDS rate is also 10% then there is no need to pay any additional tax.

Most of the Senior Citizens submit Form 15H to avoid TDS. In many cases, senior citizens feel if they have done this, they are not liable to pay tax. But if you have two or three fixed deposits in separate banks and you submit a Form 15G or 15H in all the banks, you will have to pay tax if the total interest from all the fixed deposits exceeds the taxable income limit.

Like most of us, the Government doesn’t like to wait for its money. It wants us to pay tax dues or at least a portion of it as and when we get our incomes. So, make sure you meet the compliance requirements which are related to TDS. Kindly note that false declarations for TDS avoidance can result in penalties and interest charges. So, kindly avoid doing it!

Continue Reading :

- List of Important Tax Deductions for FY 2018-19 / AY 2019-20

- Income Tax Slab Rates FY 2018-19 & Budget 2018 Key Highlights

- When to submit Form 15G & Form 15H?

- Income Tax Declaration & List of Investment Proofs

- Different Asset classes have different Tax implications – How Returns are taxed?

(Post published on : 20-March-2018)

Join our channels

Dear Sir,

Kindly guide me know about the TDS rules for a person winning some prize money through recognized sports championships . Organizer should deduct TDS or sportsman himself pay it?

Dear Ajeet,

“According to section 194B of the Income Tax Act 1956, ‘The person responsible for paying to any person any income by way of winnings from lottery or crossword puzzle or card game and other game of any sort in an amount exceeding ten thousand rupees shall at the time of payment thereof, deduct income tax thereon at the rates in force.”

There is no clear mention of SPORTs in the applicable IT section, hence there is no clarity.

You may kindly check with a CA as well.

Related links :

Link – 1

Link – 2

Dear Sir,

Thanks a lot for your prompt reply but CAs and Income tax commissioners are having different views on this issue . One CA from Goa deducted 30% TDS on the prize money given to the players of International Chess Tournament. Kindly again guide me about the TDS deduction while disturbing the prize money.

Dear Ameet,

Kindly note that I am not a taxation expert.

Also, there is no clear-cut information on the requested topic.

WHAT IS THE LIMIT OF EXEMPTION OF HOME LOAN PRINCIPAL AND INTEREST PAID

Dear Jayesh,

Principal u/s 80c : Max is Rs 1.5 Lakh

Interest u/s 24, under the head INCOME FROM HOUSE PROPERTY : max is Rs 2 lakh.

Related articles :

* Income Tax Deductions List FY 2018-19 | List of important Income Tax Exemptions for AY 2019-20

* Understanding Tax Implications of Income from House / Property

If we purchase water cooler for gift purchase. can we deduct the TDS on it. Supplier are saying that TDS will not deduct because we are counter selling.

please suggest me that TDS deducted or Not

Sreekanth Reddy SIR THANK YOU FOR CHART OF TDS BUT 194c THAT IS CONTRACT DEDUCTION SEC IS NOT FOUND IN CHART

Dear Dhwani,

Payment to contractors / sub-contractors (Section 194C) – TDS is going to be @ 2% for payments made to contractors who are not HUFs/individuals and 1% for payments made to contractors/sub-contractors who are HUFs/individuals

shall we allowed the tds privilage of 50000 on interest to Senior Citizens from 1st April 2018 itself ?

Dear ANANDAN ji .. Yes, Section 80TTB is applicable from FY 2018-19 / AY 2019-20.

Related article : FY 2018-19 Section 80TTB | Tax Exemption of Rs 50,000 on Interest Income to Senior Citizens

Hi,

In your TDS Chart, Heading shows that such rates are effective from 1st June 2018 whereas the same should be from 1st April 2018.

Dear Ritesh,

Generally the new TDS rates are applicable from June of the respective FY.

for the last diagrammatic representation, IT slab for Rs 2.5 L to Rs 5 lakhs is 5% not 10%….

Thank you dear shanmukh for pointing out this mistake.. I have corrected it!