Term insurance is the simplest and most fundamental insurance product. Term insurance plans are designed to ensure that in the event of the policyholder’s death, the family gets the sum assured (the cover amount).

Term plan provides risk coverage for a certain period of time (policy term/duration). If the insured dies during the time period specified in the policy and the policy is active (or) in force, a death benefit will be paid. It is the cheapest form of Life insurance in terms of premium.

Almost each and every insurer now offers Term insurance plan(s). HDFC Life’s Click 2 Protect Plus is one among the very popular term insurance plans that are currently available in the market. HDFC Life has recently launched a new version of this plan, with more options, called as ‘ HDFC Life Click 2 Protect 3D Plus ’. As per HDFC Life, this new plan provides cover for 3Ds – Death, Disease and Disability.

In this article, let’s understand the key features, benefits, options and pros/cons of HDFC Life’s new term insurance plan – Click 2 Protect 3D plus.

HDFC Life Click 2 Protect 3D Plus – Key Features

- Plan Options: This new Term insurance plan offers you a choice of 9 plan options.

- Waiver of Premiums : All future premiums are waived on Accidental Total Permanent Disability (available under all options) and on diagnosis of Critical Illness (Available with 3D Life and 3D Life Long Protection options).

- Whole-life Protection : Protect yourself for whole of life with lifelong protection option. (Available under Life long protection option & 3D Life Long Protection Option)

- Life Stage Protection: This feature offers you to increase insurance cover on certain key milestones without medicals. This is available for all 9 plan options. Under this feature, you have the option to increase the basic Sum Assured without underwriting on any of the below specified events in the life of the Life Assured ;

- 1st Marriage : 50% of Sum Assured subject to a maximum of Rs. 50 lakh

- Birth of 1st child : 25% of Sum Assured subject to a maximum of Rs. 25 lakh

- Birth of 2nd child : 25% of Sum Assured subject to a maximum of Rs. 25 lakh

- The Life Assured has to be less than 45 years of age at the time of the above mentioned events.

- This option will be available only for a period of six months from the date of the above specified events.

- An additional premium will be charged for an increase in the Sum Assured.

- This option shall be available only if no claim has been made under the policy, eg. Waiver of premium on ATPD, Critical Illness etc. (or) under any rider.

- Top-up option : This plan offer you a flexibility to increase your cover every year through top-up option. This option can be exercised only at the policy inception. The increased benefit will continue till earlier of the increased Sum Insured becomes 200% of the Initial Sum Insured (or) happening on Claim event. (An additional premium will be charged for the increase in the Sum Assured. The incremental cover as well as the incremental premium, both, will apply prospectively. The policyholder has the option to exit this option at any time during the remaining policy term.)

- Special premium rates for female lives

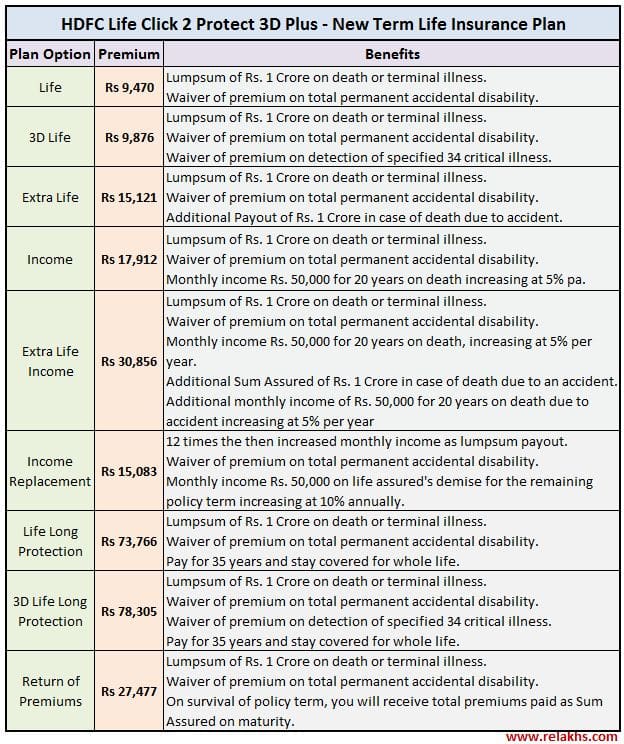

Options under HDFC Life’s new Term insurance Plan – Click 2 Protect 3D Plus

The options under this new Term life insurance plan can be divided as below ;

- Lump sum payment on death or on diagnosis of terminal illness

1) Life Option : Under this option your nominee gets a Lumpsum Benefit on death or diagnosis of Terminal Illness. Your future premiums are waived upon Accidental Total Permanent Disability (ATPD). (What is Terminal Illness ? – A life assured shall be regarded as terminally ill only if that life assured is diagnosed as suffering from a condition which, in the opinion of two independent medical practitioners’ specializing in treatment of such illness, is highly likely to lead to death within 6 months.)

2) 3D Life Option : In addition to the benefits under Life Option, you will receive an additional benefit of waiver of your future premiums upon diagnosis of Critical Illness. (Kindly refer to product brochure for the list of 34 Critical illnesses that are covered under this plan)

3) Extra Life Option : In addition to the benefits under Life Option, your nominee will get an additional Extra Life Sum Assured upon death due to Accident.

- Lump sum Income payment and/or Monthly Income payment on death or on diagnosis of terminal illness. The Minimum income term is 1 month and upto a maximum of 20 years can be chosen. The income period shall commence immediately on death and continue for the chosen income period.

4) Income Option : This plan option is ideal if you wish to provide your nominee with a Lump sum benefit and a level or a increasing stream of Income in your absence. Also, your future premiums are waived upon Accidental Total Permanent Disability (ATPD).

5) Extra Life Income Option : In addition to the benefits under Income Option, an additional Lump sum & Income benefit is paid upon death due to accident. Also, your future premiums are waived upon Accidental Total Permanent Disability (ATPD).

6) Income Replacement Option : Under this option, your nominee would receive 12 times the then increased monthly income as lump sum death benefit and will also receive level or increasing income stream. Also, your future premiums are waived upon Accidental Total Permanent Disability (ATPD).

- Fixed Premium Paying Term and whole-life protection. Under these options, you need to pay premium for fixed term and the life cover is provided for whole-life. (Premium Paying Term = 65 – Age at entry)

7) Life long protection option : You are protected for your entire life. Your nominee gets a Lump sum Benefit on death or diagnosis of Terminal Illness. Also, your future premiums are waived upon Accidental Total Permanent Disability.

8) 3D Life long protection option : In addition to the benefits under Life Long Protection Option, you will receive an additional benefit of waiver of your future premiums upon diagnosis of Critical Illness.

9) Return of Premium Option : Under this plan option, you will get back all your premiums if you survive till the end of the Policy Term. On death/ diagnosis of Terminal Illness during the Policy Term a Lumpsum benefit will be paid to your nominee. Also, all your future premiums are waived upon ATPD.

HDFC Click2Protect 3D Plus Policy Options & Indicative Premium Quotations

Let’s now understand the applicable premium rates and benefits under different plan options with an example.

The below premium quotes are for a 30 year old male Policyholder (non-smoker), for Sum Assured of Rs 1 crore with 30 year policy term. The Premium payment term for Life long Protection & 3D Life Long Protection options is 35 years (PPT = 65-30 years, policyholder’s current age).

Accidental Death benefit of Rs 1 cr has been considered for options ‘Extra Life’ & ‘Extra Life Income’. All Income Options have been considered with Rs 50,000 per month as monthly income on death, with an increasing rate of 5% per year for 20 year income period. Under Income Replacement option, the rate of increase of income is fixed at 10%.

My views on HDFC Life Click 2 Protect 3D Plus Plan

If you are planning to buy a life insurance plan with an adequate life cover (sum assured) at affordable premium rate then Term insurance plan is the best choice. There is no doubt about this! But do we need to have these many options under a Term insurance plan. Is n’t it a simple life cover option enough?? Yes, a term plan with just a basic cover is more than enough to meet your life cover requirement.

Below are some of the points to ponder upon when considering Click 2 Protect 3D plus policy;

- More Options, More complexity : To be frank, I have spent good amount of time to go through all the options & scenarios available under this plan and to comprehend these options. If you are considering to buy this plan, you have to carefully go through all the rules and eligibility conditions that are applicable under each option / feature.

- No Comprehensive Plan option : If you notice the above Plan option table, none of these plan options has all the available features.

- More Features, Higher Premium Rates : If you look at the above premium quotes, a basic life cover option ‘Life Option’ (or) 3D Life option is available at affordable premium rates, whereas, if you would like to have more features to the base plan, you need to pay more.

- Fixed Premium Term : The premium term is fixed under Life long protection & 3D Life Long Protection plan options. The policyholder has to pay the premiums till he/she attains 65 years of age.

- No Comprehensive Permanent Disability Cover : Kindly note that this plan has an in-built feature of ‘waiving of premiums on Accidental Total Permanent Disability’ under plan options. But, no lump sum benefit or fixed regular amount is not payable on total permanent disability. I believe that one should not only consider a Term plan with adequate life cover but also should take a comprehensive Personal Accident Policy, which provides Accidental Death Benefit and also covers Accidental Total Permanent Disability. So, either you need to add a separate Accidental Death Benefit Rider to this plan or has to take a stand-alone Personal Accident Insurance policy. (Read : ‘Best Personal Accident Insurance plans‘)

- No Comprehensive Critical Illness cover – Same as the above point. You may have to take a separate CI rider or CI plan. Also, Critical illness feature is available only with 3D Life option and 3D Life Long option, subject to certain conditions.

- Monthly Income Options : You need to select the monthly income (quantum) and its term (income period) at the inception of the policy itself. An individual’s life can not be predicted in advance. It’s not prudent to fix a monthly income / period now and pay premiums as per this selection.

- Preferred Options : Term insurance plan from any life insurance company should be ok. You need to just opt for a base cover as per your requirements / affordability and disclose all the required information in proposal form accurately. In case, you have shortlisted HDFC Life as your preferred insurer, you may consider Life Option or 3D Life Option of Click 2 Protect 3D Plus plan.

Continue reading :

- If Life is unpredictable, INSURANCE can’t be optional!

- Traditional Life insurance plan – a terrible Investment option?

- Best Term insurance plans – Comparison & Review

- Is Term insurance a waste of money?

(Image courtesy of fantasista at FreeDigitalPhotos.net.) (Reference & Courtesy : HDFC Life Click 2 Protect 3D Plus product brochure) (Post first published on : 25-May-2017)

Join our channels

Dear Sir,

In the HDFC Life Click 2 Protect 3D Plus Plan– 3D life option accidental death is not covered and critical illiness is covered?. Does it means that; if a person who has brought the plan dies due to an accident then his family will not get any benefit even after taking the plan?

How does insurance companies classify death? What is a natural death as per insurance companies? What is the difference between natural death and other form of death as per insurance companies?

Dear Arun,

If death happens due to accident, the nominee of the policyholder will get the insurance cover under basic plan. The accidental death rider benefit will not be available, if not opted for.

Life Insurance plans provide financial benefit covering all causes of death excluding suicide (which may be covered after waiting period). Accidental death insurance provides financial benefit covering death exclusively caused due to an unforeseen and unfortunate accident.

Life insurance provides death benefit even if you die months or years of getting a disease or illness. Accidental insurance provides benefit if you die instantly or within specific period of an accident usually 180 days.

Dear Sreekanth, I am a diabatic, can I take HDFC 2 click 3D policy? Will it benefit for me..

Thanks

Dear Sudheer,

The insurer may load the premium considering your health history.

You may opt for a basic life cover.

In case, you are also planning for a health insurance cover – kindly go through this article @ Are you suffering from Diabetes or Hypertension? Let Health insurance take care of your worries

Thank a lot Mr.Sreekanth..

Hi

I am in armed force. Would like to know whether this policy will be valid due to death in war (declared or not declared) while fighting for country? Or the policy will be cancelled due to act of war?

Pls help me. I have to do a term insurance of 1 Cr.

Dear rakesh ..

Kindly go through this link (section : Conditions where Death benefit will not be paid).

Advisable to get written confirmation on this from the Insurer also. Kindly contact them.

can I choose term insurance with limited premium payment option. I am currently 42 years old. can I choose 10 year of limited premium payment option which will cover entire 75 years of my age protection

Dear arumugam ..If the product/plan offers such option, you may opt for it.

I want good term insurance plan annual income 800000 /increase term insurance cover excluding lic

Dear Jayant..Kindly read : Best online term insurance plans..

Yes, sir there is a option in HDFC life where you can opt for the limited premium payment.If you are interested to know about it than fell free to call on this number

Rakesh Kumar Singh

7696750577

yes it saves the policy costing

Dear Sreekanth,

You might wish to use this information to keep your audience well-informed:

1. SBI is about to launch a term insurance that might give its competitors a run for their money: it is slashing its existing term insurance rates by a third. Here is a link to the news:

https://goo.gl/Fx6oTf

2. LIC is specifically targeting cancer in the new avatar of its term insurance plan . Interesting because now there is about one in eight chance of developing cancer in one’s life. Here is a link to the news:

https://goo.gl/RDsnjL

Dear Srikanth,

It a very good information,

can you help me little bit further,

I am NRI working in Oman, Through policy bazar i received advice to choose a term Plan.

1. PNB MetLife Mera Term Plan: Secure your family, (Single Plan for Me and My Wife)

2.HDFC Life’s new Term insurance Plan – Click 2 Protect 3D Plus (Separate Plans for Me and My Wife)

which one can I go for Me and my My Wife Term Plans or any other term plans better than these?

Waiting you feedback

Ravi Kumar

9866152710

Hyderabad

Dear Ravi,

May I know if your wife is an earning member of your family? Your age profiles?

Dear Sreekanth,

My Wife is a HouseWife, My age 36, and my wife 31,

Thanks in Advance

regards

Ravi

Dear Ravi,

Ideally, life insurance is not required for an individual who is not an earning member of a family and do not have any financial liabilities.

In case, you believe that life cover is required for your spouse as well, you may go ahead with joint-life cover of any insurance company, based on your affordability and payout conditions.

Suggested readings :

Article – 1

Article – 2

Dear Sreekanth,

Thank you for your valuable feedback,

Yes your right, for Individual who is not an earning member, life insurance is not mandatory, but from one of your article and my research I found reviews that, In my absence or in later stages of life, when a time spouse require to have a Life cover then the premiums are high, so better to have a life insurance at right time!

Regards

Ravi Kumar

Dear Ravi,

Each family has their own set of requirements.

God forbids, if anything happens to you, if you have an adequate life cover then your spouse/nominee would receive the claim amount right.

With that they (family) can continue same standard of living and achieve the set financial goals/obligations.

Hi SreeKanth,

i have recently started studying ur blogs. these r really helpful n i understood the importance of insurances.

as i have commented earlier also i’m planning for Term insurance, Accidental cover n health cover (Term, accidental can be clubbed based on policy).

My concern is i want to take policies after proper analysis,study n i was planning to buy all 3 covers simultaneously to get the best of covers. but it is taking more than the expected time. i could hardly go through 2,3 policies last week.

this way it will take months.

plz guide me how shd i proceed.

Dear Divya,

Suggest you first take a Term plan with basic cover from any life insurance company of your choice.

You may then shortlist a stand alone personal accident cover with Disability cover.

After which you can shortlist a Health insurance plan.

Hi Sreekanth,

i have a 9 yrs old LIC policy on my name and i was thinking that it would be enough for the name of insurance policy.

so i was planning a new LIC policy for my kid but some of your articles has guided me correct.

now, i want to have an insurance policy asap. as i’m 31 yrs old and in private sector.

i have few doubts and need your guidance:

* as i understood till now that we need to have 3 type of covers for max security of our dependents future- basic life cover, accidental cover & a health cover for critical illness. plz correct me here if required.

* is it a good decision to dissolve my current LIC and plan for one of the covers at this time. i have LIC jeevan saral for 18 years with 36k yearly premium (8 premiums already given)

* please share few other links for life, health covers .

Dear Divya,

1 – Your understanding is correct. Health insurance can be a for a normal cover not necessarily a Critical illness cover.

2 – If you do not have adequate life cover and/or health cover, you may buy these and then can discontinue your existing policy.

Kindly read :

If life is unpredictable, insurance cant be optional

Traditional life insurance plan – a terrible investment option

How to discontinue unwanted life insurance policy?

Best Term insurance plans

Best portals to compare health insurance plans

Dear Sir,

I am 28 years old & married from last 1 year. I want to buy a term plan.

I am comparing ICICI Life plus plan & HDFC life plan.

Please tell the major difference between this two plans & suggest which is the best.

As my DOB is 24th june, I’m planning to buy term plan before this date.

Regards,

Sachin

Dear Sachin,

Term plan from any insurance company should be ok..

Kindly read :

ICICI Term plan – review

Best Term insurance plans

icici pru iprotect smart is the best product which provides all the benefits in a single policy . even you can opt for critical illness cover which covers 34 major illness

I just bought Max Life with 1 cr cover + accidental death option and waiver of premium applicable till 75 years of age. Almost all products cover all possibilities but they are making more complex now day by day.. Your article is really nice.. one piece of advice is always never club ur insurance needs and investment needs.. Unfortunately Insurance companies are selling investment plans in the form of insurance…

Dear Asnagpal,

The insurance buyers want more features like return of premium, income replacement etc., so insurers are coming up with more features.

It can be other way also, insurers want to get more revenues from term plans by offering more features…

A simple basic life cover which is affordable can be enough. Personal Accident cover can be bought as a standalone product. Health insurance / Critical illness cover can be bought depending on ones requirements and affordability.

Hi Sreekanth ,

This has been very well explained . I have a question regarding the same . I am holding a HDFC Life Click 2 Protect Plan for 50 lakhs for around 5 years. I want to go for 1 crore now.

So in that case, should I but another term insurance policy for 50 lakhs or should I cancel the existing one and go for fresh one for 1 crore.

Please suggest

Dear Rahul,

We may keep seeing new products with many features and may be more affordable in future too..but we cant keep churning our insurance portfolio.

Suggest you to apply for a second term insurance plan.

Kindly read : Best term insurance plans..

Although return of premium option seems to be expensive by 18k or so in comparison with LIFE option, there is a benefit of getting back the premium amount paid on maturity (of course with no interest).

Is this a better term plan compared to the rest of the plans out there, which don’t have this option?

Isn’t this a better term plan compared to the rest of the plans out there, which don’t have this option?

Dear Phani,

My suggestion would be a basic option can meet the requirements of getting adequate cover at very affordable premium rate.

One can invest the differential premiums in better investment avenues instead waiting for ‘getting back the premiums’ after many years.

Hello Sreekanth,

Thanks for sharing this article with us. Today I learned new thing about Insurance policy. Its really helpful.

Thanks You

good one!

Hi Sreekanth

Is there an option for NRI’s to buy Term insurance?

Dear Jiju ..Yes, most of the insurers do offer term plans for NRIs.

Your review so informative. HDFC insurance schemes are explained very well by you. The list of detailed aspects in the review cover all the pros and cons like whether to go for a premium one or not. If we need more features, there is a need of the scheme, we need to pay high in the form of premium.

Hi Sreekanth,

very nice explanation and very good article. I request you to put one highlighted sentence at the end ” HDFC life claim amount settled ratio is very bad and has gone worst over last 5 years.”. Let the buyers at least think once again before buying it, because its the question of life of their dependents. You are very right in saying MORE OPTIONS, MORE COMPLEXITY. This policy is mainly designed to increase the revenue and profit of its company.

regards

RAJ

Dear Raj,

I am sure you are aware of Section-45 of the Insurance Act – “If your policy is 3 years old, no matter what happens, the life insurance company will not be able to deny the claims. So, your life insurance company has only 3 years in hand to reject the policy based on any mis-representation or mis-statement. Once 3 policy years are completed then the life insurance company has to settle the claims and can not reject them.”

So, claim settlement may not be THE FACTOR to watch out for anymore….