If you have followed Budget 2016 proposals, one of the major news-making item (especially for the salaried persons) was about providing an one-time portability option from EPF (Employees Provident Fund) to NPS (National Pension System).

Till date, there has been no major announcement on this proposal. But here comes the latest news on ‘transfer of EPF to NPS‘.

If you have been contributing to EPF or Superannuation Account, you now have the option of transferring your PF or Superannuation funds to NPS. Kindly note that this is allowed only one-time.

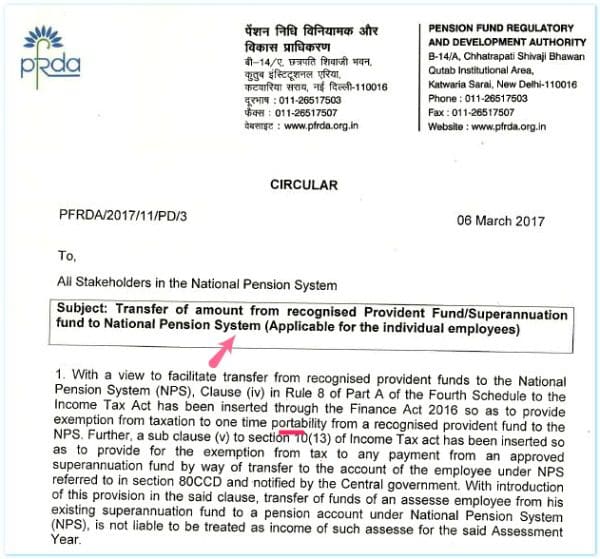

The Pension Fund Regulatory and Development Authority (PFRDA) has issued broad guidelines for giving effect to transfer of PF amount to NPS Scheme.

Transfer of EPF or Superannuation funds to NPS : Latest guidelines

In case you are interested in transferring your EPF account balance to NPS, below are the guidelines;

- To transfer funds from PF to NPS, it is mandatory to have NPS Tier 1 account. The subscriber can open NPS account through his/her employer, Points-of-Presence (i.e, banks or any entities registered as PoPs with PFRDA) or through eNPS portal.

- The member of Recognized EPF or Superannuation Fund trust has to submit the transfer request through his/her employer.

- Based on your (EPF member / employee), the EPF / Superannuation trust may initiate the transfer of balance from EPF to NPS.

- Recognized PF / Superannuation fund trust may issue the cheque effecting the transfer.

- Transfer of EPF to NPS by a Govt employee ;

- The employee should request the PF/Superannuation fund to issue a letter to his present employer mentioning that the amount is being transferred from the fund to be credited to the NPS Tier-1 account of the employee.

- The present employer or Point of presence (POP) i.e., the nodal office while uploading the fund has to mention the transfer from PF/superannuation fund in the remarks column while uploading.

- Transfer of EPF to NPS by a Private sector employee ;

- In case of private sector employees, the employees should request the recognized PF/superannuation fund to issue a letter to the present employer/PoP as the case may be mentioning that amount is being transferred from the PF/Superannuation fund to be credit in the NPS account of the employee/individual Tier-I account.

- The POP will get the amount collected and the same has to be uploaded in the NPS account of the subscriber

Transfer of funds from EPF to NPS & Income Tax implications

- PFRDA in its circular has clearly mentioned that as per the provisions in the Income Tax Act, the amount transferred from Recognised PF / superannuation fund to NPS will not be treated as Income of the current financial year and is hence not taxable.

- It has also been pointed out that the employee can not make income tax claim on the transferred amount under section 80CCD.

My opinion

Personally, I believe that NPS with its current product structure, may not be a great investment avenue. If your employer offers only NPS, then you do not have choice but to contribute to NPS.

In case, you are currently contributing to EPF, should you switch to NPS? If you have the option to pick EPF or NPS, which one is better?

My pick would be EPF. Why? Kindly read this article @ ‘Why NPS is not a great investment option?‘

Given a choice, I will consider EPF as part of Debt allocation and would prefer investing in Equity oriented Mutual funds for my Retirement goal.

(This article is based on limited available information, the above details can be modified or updated soon) (Image courtesy of Mister GC at FreeDigitalPhotos.net) (Source & Reference : PFRDA Circular) (Post first published on : 07-March-2017)

Join our channels

Hi Sreekanth,

Comparing LIC Superannuation and NPS Tier 1, which one is best? I had opted LIC Superannuation which I can’t come out, is it better to switch that to NPS which will better return that LIC Superannuation?

Dear Thothathiri ..Need to go through some more details of your scheme before I could advice.

What is their suggested annuity rates? May I know your current age and expected retirement age??

Hi Sreekanth,

Thanks for your time

My scheme is Group LIC Superannuation plan which I opted from Year Sep 2010. My current age is 44 and retirement age is 58. I don’t know the annuity rate of LIC superannuation.

Dear Thothathiri Ji,

As you have around 14 years investment time-frame, may be NPS could be a better choice (though personally I do not like NPS as an investment avenue, but compared to Superannuation plan, may be its a better choice).

i am central government employee contributing to pen.tier 1 of NPS near about 50000 rs . what u think should i have to transfer 50000 rs to pen tier 2 .and get tax benefit of 150000 under 80c and 50000 under ccd 1b.

Dear yogesh ..Kindly note that Tier II does not give you any tax benefits.

Hi Sreekanth,

Thanks for your information about switching the superannuation to NPS.

Am having EPF and superannuation (LIC) for the past 6.5 years which is payed through my Salary by my employer.

Is it good option to Switch only LIC superannuation to NPS?

Am already having NPS Tier1 Account.

Thanks & Regards

Thothathiri S

Dear Thothathiri ,

Kindly read : NPS is not a great investment option with its current features??

Dear Sreekanth,

I have opted to pay Rs. 5000 per month in NPS Tier-1 account.

Can I change this to a smaller amount later ?

Thanks & regards,

Afzal

Dear Afzal ..I believe that it is possible.

Kindly note that minimum contribution for NPS Tier 1 account is Rs.500 and Rs.1, 000 for Tier 2 a/c.

Thank you !

Your message on PF to NPS transfer is good , but I want to know how is stop the deduction of EPS from pf if there is any way then guide us as EPS scheme is one of the worst scheme run by govt.

Hi Sreekanth, I m a private employee and contribute to both EPF and superannuation fund through the employer on monthly basis. Is it possible to divert only superannuation fund to NPS. What I understood that we can only transfer cumulative superannuation amount one time only.

Dear Ash,

I believe it is possible to transfer only superannuation and yes it can be done only one time.

Henceforth, your contributions will be made to NPS, I guess.

But let’s wait for more clarity on this topic.

What is best option to get money in hand if thinking of retiring @55 Years of age?

What Annuity exactly means and how it will help me when I am alive?

Dear Vinod,

Best option? – It depends on the current age of the investors 🙂

Annuity means – Regular pension that is payable to annuitant.

You may go through below articles to understand about annuity;

NPS – Review.

HDFC Click2Retire plan – review.

Hello Mr Sreekanth

I am a govt employee who is under NPS scheme and is now planning to resign. My total accumulated value in NPS is around 5 lakh. And I know it will now be treated as premature withdrawal of the whole amount. So I need to purchase an annuity of 80% and rest 20% I’ll receive as lumpsump. So, in this case as buying an Annuity is compulsory for me as I don’t have any other option of investment from the amount I get from NPS. I am 37 now and according to you what type of annuity plan should I purchase as I have to choose between the following Annuity providers:

Life Insurance Corporation of India

SBI Life Insurance Co. Ltd.

ICICI Prudential Life Insurance Co. Ltd.

HDFC Standard Life Insurance Co Ltd

Bajaj Allianz Life Insurance Co. Ltd.

Reliance Life Insurance Co. Ltd.

Star Union Dai-Ichi Life Insurance Co. Ltd.

Also which annuity option should I should from the below mentioned ones:

1) Annuity/ pension payable for life at a uniform rate.

2) Annuity payable for 5, 10, 15 or 20 years certain and thereafter as long as the annuitant is alive.

3) Annuity for life with return of purchase price on death of the annuitant.

4) Annuity payable for life increasing at a simple rate of 3% p.a.

5) Annuity for life with a provision of 50% of the annuity payable to spouse during his/her lifetime on death of the annuitant.

6) Annuity for life with a provision of 100% of the annuity payable to spouse during his/her lifetime on death of the annuitant.

7) Annuity for life with a provision of 100% of the annuity payable to spouse during his/ her life time on death of annuitant. The purchase price will be returned on the death of last survivor.

I have also heard that option 6 is the default annuity option.

Thanks & Regards

S.Kumar

Dear Kumar,

It really does not matter much regarding selection of annuity provider. In India, the annuity rates provided by most the insurers are on lower side only.

Is it possible for you to get annuity rates for these options?

As you are young and at this stage of your life, these options really matter much. But as you say, you gotto pick one. May be point 5 looks fine (if married).

Hi Sreekanth,

My previous employer had superannuation scheme. When I left issued ICICI Pru bond for accumulated amount and receiving yearly twice as payout. Bond value is 75000/- and getting payout of 2450/- twice in year.

Is there any possible to shift this amount to NPS?

Which one is better NPS or existing one ?

Thanks & regards

Suresh Kotapati

Dear Suresh,

May I know if you have resigned or retired? Looks like they have issued you a Pension which pays you annuities.

I believe that it is not possible to move this amount to NPS.