On February 26, 2026, the Securities and Exchange Board of India (SEBI) introduced major mutual fund reforms to ensure schemes remain “true to label.” The new rules include the launch of Life Cycle Funds, discontinuation of Solution-Oriented schemes, a higher 80% minimum equity requirement for select categories, stricter portfolio overlap limits, and a phased implementation timeline through 2026–2029.

Not dramatic.

Not sensational.

But structurally important.

If you look closely, this circular isn’t about introducing new products—it’s about correcting course. Over the years, the boundaries between fund categories began to blur, and names gradually turned into marketing labels rather than true reflections of strategy. Some so-called “equity” funds quietly reduced their equity exposure, while certain “solution-oriented” funds morphed into little more than static hybrids.

SEBI’s new move is essentially an attempt to restore that lost alignment and bring clarity back to fund classifications. If you invest in mutual funds — or plan to — this update directly affects you.

Let’s break it down in simple terms.

SEBI 2026 Mutual Fund Rules & Reforms

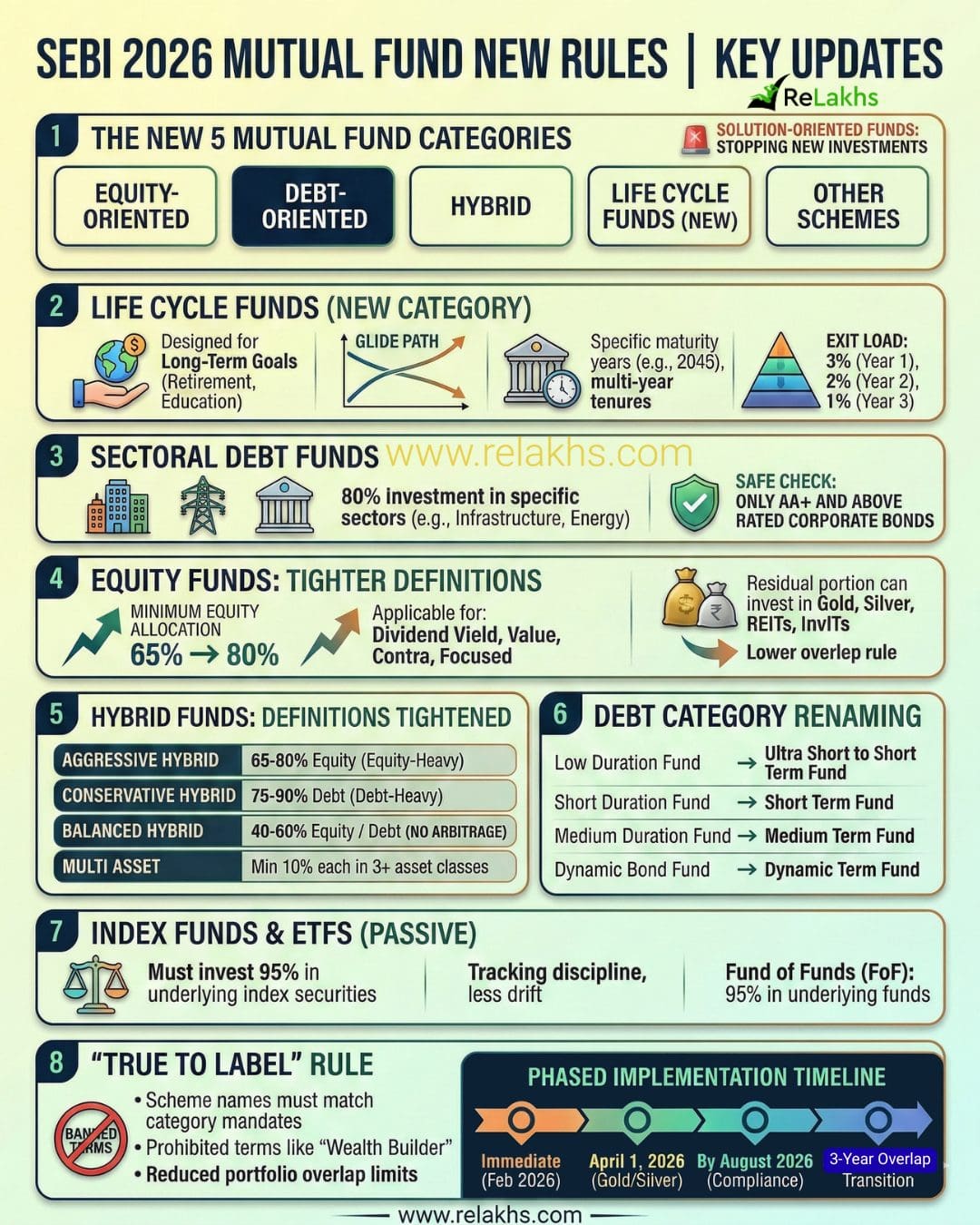

1. The New 5 Broad Mutual Fund Categories (2026 Framework)

SEBI has now grouped all mutual fund schemes under five major buckets:

- Equity-Oriented Schemes

- Debt-Oriented Schemes

- Hybrid Schemes

- Life Cycle Funds (New)

- Other Schemes (Index Funds, ETFs, Fund of Funds)

The biggest change is in two parts: SEBI is bringing in Life Cycle Funds and shutting down Solution-Oriented Funds.

Solution-Oriented schemes like retirement and children’s funds will no longer be allowed to take new money (fresh investments) and will eventually be merged into other funds with a similar asset mix and risk level. If you’re invested in a retirement fund, you cannot top up now. Your AMC will contact you regarding the transition.

2. Life Cycle Funds: New Fund Category

This is a completely new category. As per SEBI, these funds are designed for long-term goals like retirement or children’s education.

- Characteristics: These funds follow a glide path, starting with high equity exposure and gradually shifting to safer assets (debt/gold) as the target maturity date approaches.

- Maturity: Launched with specific target years (e.g., “Life Cycle Fund 2045”) in tenures of 5 to 30 years (multiples of 5).

- Exit Load: To encourage discipline, a tiered exit load applies (3% in Year 1, 2% in Year 2, and 1% in Year 3).

| Feature | Guideline |

|---|---|

| Tenure | 5, 10, 15, 20, 25, 30 years |

| Naming | Must include maturity year (e.g., “Life Cycle Fund 2045”) |

| Asset Mix | Equity + Debt + Gold/Silver ETFs + InvITs |

| Exit Load | 3% (Year 1), 2% (Year 2), 1% (Year 3) |

My Take on Life Cycle Funds: When Securities and Exchange Board of India (SEBI) introduced Life Cycle Funds, the intent was discipline and simplicity. But suitability depends on the investor.

- Pre-defined glide path – The fund reduces equity automatically over time. Your life, income, and risk appetite may not follow that fixed schedule.

- Less flexibility – Tiered exit loads (3%–2%–1%) encourage discipline, but they also make early adjustments costly if your goals change.

- May duplicate your allocation – If you already manage equity, debt, and gold separately, a Life Cycle Fund could simply bundle what you’re already doing — with less control.

- Automation vs control – Helpful for investors who struggle with rebalancing; unnecessary for those comfortable managing asset allocation themselves.

- Structure ≠ suitability – Just because it is goal-based and structured doesn’t mean it fits every financial journey.

- Life Cycle Funds aren’t inherently “good” or “bad.” They’re highly structured by design. And that structure shines brightest for the right kind of investor.

3.Sectoral Debt Funds Introduced

This is another new category. These funds can now invest 80% in debt instruments of a specific sector, such as:

- Infrastructure

- Energy

- Financial Services

There’s also a safety filter: these funds can invest only in corporate bonds rated AA+ and above, which improves clarity for investors and helps keep a check on excessive credit risk.

4.Equity Funds: Tighter Definitions

This is where many investors may see changes. Minimum equity allocation for several categories has been raised from 65% to 80%, including:

- Dividend Yield Funds

- Value Funds

- Contra Funds

- Focused Funds

At the same time, equity funds can now use gold, silver, REITs and InvITs in their residual portion.

Earlier, AMCs had to choose between offering either a Value Fund or a Contra Fund. Now they can launch both, but with a strict limit—the portfolio overlap between them cannot exceed 50%. This change encourages more options while preventing excessive similarity between the schemes.

5.Hybrid Funds: Definitions Tightened

SEBI has also refined hybrid categories.

One key change: Arbitrage is NOT allowed in Balanced Hybrid Funds anymore. This prevents misuse of the category purely for tax efficiency.

| Category | Equity | Debt | Notes |

|---|---|---|---|

| Conservative Hybrid | 10–25% | 75–90% | Debt-heavy |

| Balanced Hybrid | 40–60% | 40–60% | No arbitrage |

| Aggressive Hybrid | 65–80% | 20–35% | Equity-heavy |

| Multi Asset | Min 10% each | Min 10% each | At least 3 asset classes |

6.Debt Category Renaming (Clarity Move)

Several debt fund categories were renamed for clarity:

| Old Name | New Name |

|---|---|

| Low Duration Fund | Ultra Short to Short Term Fund |

| Short Duration Fund | Short Term Fund |

| Medium Duration Fund | Medium Term Fund |

| Dynamic Bond Fund | Dynamic Term Fund |

7.Index Funds, ETFs & Arbitrage Funds

As per the 2026 reforms by Securities and Exchange Board of India (SEBI):

- Index Funds & ETFs must invest at least 95% in the securities of the index they track.

- Fund of Funds (FoF) must invest 95% in their underlying fund(s).

At first glance, this looks like a small technical detail. In passive investing, consistency matters more than creativity. An index fund should behave like the index — not like an active fund with cash positions.

The 95% rule cuts down on drift by enforcing better tracking discipline and limiting unnecessary deviations. It quietly reinforces the core principle of staying true to the fund’s label.

SEBI guidelines now require Arbitrage Funds to invest their non-equity portion primarily in Government Securities (G-Secs) with a maturity of up to 1 year. This shift prioritizes safety and liquidity while curbing credit risk in these equity-oriented schemes.

8. “True to Label” – The Big Rule

This is the philosophical core of the reform.

- Strict Naming Rules: SEBI has introduced strict naming rules where scheme names must exactly match their category names, leaving no room for creative marketing spin.

- Banned Misleading Terms: Terms like “Wealth Builder,” “High Growth,” or “Power Gains” are now prohibited from fund names. The name must clearly reflect the fund’s actual mandate and strategy.

- Portfolio Overlap Limits: Sectoral and thematic funds now face restrictions where portfolio overlap with other schemes from the same AMC cannot exceed 50% (excluding large-cap funds). This ensures better differentiation and transparency across offerings.

My Take:

When SEBI talked about “True to Label,” it might have sounded technical at first. But the idea is actually very simple. If a fund calls itself a Value Fund, it should invest like one. If it’s labeled a Balanced Fund, it should genuinely stay balanced.

The name must reflect the fund’s actual strategy—not just marketing hype. Many investors pick funds based on these category names without digging into monthly portfolios.

So when labels drift from reality, they end up carrying hidden risks. “True to Label” isn’t about chasing higher returns. It’s about restoring honesty to classifications. Not a flashy reform, but a crucial one.

SEBI 2026 Mutual Fund New Rules: Timeline

- Immediate (Feb 26, 2026):

- Solution-Oriented funds stopped fresh subscriptions.

- AMCs can launch Life Cycle & Sectoral Debt funds.

- By August 2026 (6 Months):

- All schemes must align names.

- Equity floors must be increased to 80% where required.

- Monthly portfolio overlap reports must be published.

- Special Timeline:

- Gold & silver valuation changes effective April 1, 2026. (From April 1, 2026, gold and silver holdings will follow a revised domestic spot-price valuation method.)

- Sectoral and thematic funds have a three-year phased timeline (35% + 35% + 30%) to reduce excess portfolio overlap.

| Phase | Effective Date | What Changes |

|---|---|---|

| Immediate Effect | February 26, 2026 | • Solution-Oriented schemes stop fresh subscriptions • AMCs allowed to launch Life Cycle Funds & Sectoral Debt Funds |

| Gold & Silver Valuation Update | April 1, 2026 | • Physical gold & silver to be valued based on revised domestic spot-price methodology |

| 6-Month Compliance Window | By August 2026 | • True-to-label naming alignment • Equity floor increase (65% → 80%) where applicable • Portfolio realignment• Monthly portfolio overlap disclosures |

| Portfolio Overlap Transition (Sectoral/Thematic Funds) | 3-Year Phased Reduction | • Year 1: Remove 35% of excess overlap • Year 2: Remove additional 35% • Year 3: Remove remaining 30% |

What Should Investors Do?

If you’re a mutual fund investor:

- Don’t panic.

- Your existing units are safe.

- Watch for communication from your AMC.

- Re-evaluate your allocation if your fund changes category or risk level.

If you’re holding a Retirement/Children’s fund: You cannot add fresh money. Wait for the merger details before taking action.

In markets, drift happens gradually. Categories stretch, definitions blur, and marketing often drowns out the actual mandate. Every few years, a reset becomes essential. This 2026 reform feels like exactly that—a corrective step rather than a revolution. For investors, that clarity is usually far more valuable than added complexity.

Continue reading:

- Best Mutual Funds for 2026: Picking “Consistency Kings” Over Performance

- My Latest Mutual Fund Portfolio 2026 | My 16 Year MF Journey & Lessons Learned

- What’s in a Name? The Hidden Truth About Children’s Insurance Plans

- All LIC Plans Analysis 2026: How Much Do LIC Policies Really Return?

(Post first published on : 01-Mar-2026)

Join our channels