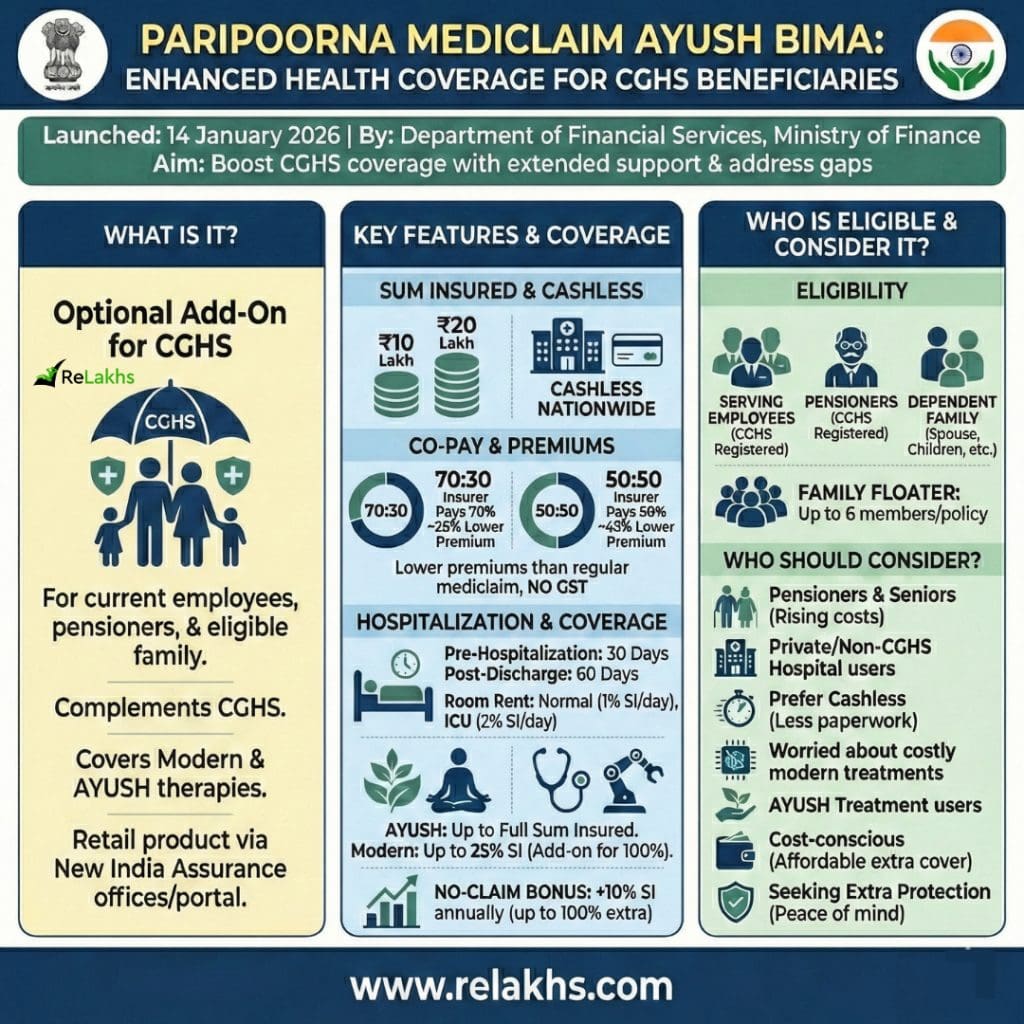

The Government of India has recently unveiled an health insurance product — Paripoorna Mediclaim Ayush Bima — aimed at enhancing medical coverage for Central Government Health Scheme (CGHS) beneficiaries and their families. Launched on 14 January 2026 by the Department of Financial Services (DFS), Ministry of Finance, this scheme is designed to provide extended support alongside the existing CGHS facilities and address coverage gaps in today’s evolving healthcare landscape.

What Is Paripoorna Mediclaim Ayush Bima?

Paripoorna Mediclaim Ayush Bima is an optional health insurance plan introduced specifically for CGHS beneficiaries — including current government employees, pensioners, and their eligible dependent family members. It is meant to complement the CGHS benefits, offering broader hospitalisation and treatment coverage, including both modern medical procedures and AYUSH therapies (Ayurveda, Yoga & Naturopathy, Unani, Siddha and Homeopathy).

Unlike regular CGHS cover, this is a retail insurance product that interested beneficiaries can choose to purchase through designated channels such as New India Assurance Company Limited’s offices and online portal.

Key Features & Coverage Highlights of PMAB Plan

- Sum Insured Options : You can choose health cover of ₹10 lakh or ₹20 lakh for hospital treatment in India.

- Cashless Treatment : Treatment can be taken cashless at a large network of empanelled hospitals across India.

- Co-Payment Choices: You can select how expenses are shared:

- 70:30 – insurer pays 70%, you pay 30%

- 50:50 – insurer pays 50%, you pay 50% (Higher co-pay means lower premium.)

- Waiting Periods :

- 30 Days – General waiting period

- 90 Days – For Diabetes / Hypertension

- Up to 24 months : For specific & Pre-Existing Diseases (PEDs)

- Lower Premiums : Premiums are cheaper than regular mediclaim policies;

- Around 28% lower with 70:30 option

- Around 42% lower with 50:50 option

- Hospitalisation Expenses Covered :

- Medical expenses 30 days before hospitalisation are covered.

- Expenses 60 days after discharge are covered

- Room rent limit:

- Normal room: up to 1% of sum insured per day

- ICU: up to 2% of sum insured per day

- AYUSH & Modern Treatment Coverage :

- AYUSH treatments (Ayurveda, Yoga, Unani, Siddha, Homeopathy) are covered up to full sum insured

- Modern treatments are covered up to 25% of sum insured.

- An optional add-on can increase modern treatment cover to 100%

- No-Claim Bonus :If no claim is made in a year, your sum insured increases by 10% every year, up to 100% extra, without extra cost.

Who Is Eligible for Paripoorna Mediclaim Ayush Bima?

This health insurance policy is exclusively meant for CGHS beneficiaries. It is not available to the general public.

The following persons are eligible to buy this policy:

- Serving Central Government employees who are registered under the Central Government Health Scheme (CGHS).

- CGHS pensioners, including retired central government employees who continue to avail CGHS facilities.

- Eligible dependent family members of the CGHS beneficiary, such as spouse, dependent children, and other dependents as permitted under CGHS rules.

Under a single policy, up to six family members can be covered together. This makes it convenient for families to take one combined cover instead of purchasing multiple individual policies.

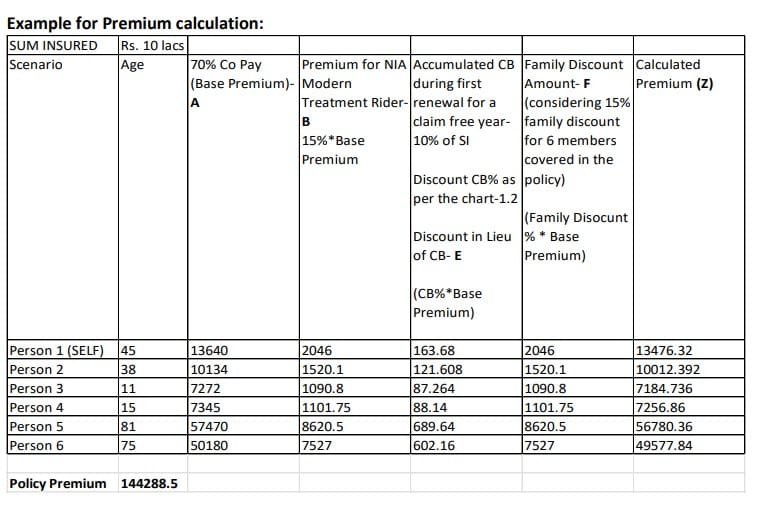

Paripoorna Mediclaim Plan Premium Illustration

This premium illustration shows how the cost of the policy is calculated for a family of six, with a ₹10 lakh sum insured under the 70:30 co-payment option.

Step 1: Base Premium (Age-Based)

- Each family member’s premium depends mainly on age.

- Younger members pay less, while senior citizens pay more due to higher health risk. This means family floater cost heavily depends on elderly members.

Step 2: Modern Treatment Rider (Optional)

- If you choose coverage for advanced/modern treatments, an extra 15% of the base premium is added.

- This is optional but useful for high-end medical procedures.

Step 3: Claim-Free Bonus Benefit

- If no claim is made in the first year, the policy earns a claim-free benefit.

- This benefit is shown as a discount equivalent in the illustration (actual benefit is usually given as increased coverage).

Step 4: Family Discount

- A 15% family discount is applied because six members are covered under one policy.

- This helps reduce the overall cost for larger families.

Step 5: Final Premium Calculation

- After adding riders and subtracting discounts, the final premium is calculated for each person.

- The total of all six members gives the overall policy premium.

Total Premium (Illustration)

👉 Approx. ₹1.44 lakh per year for 6 family members. Despite high senior premiums, likely cheaper than many individual retail family floater plans.

(₹10 lakh sum insured, 70:30 co-pay, with modern treatment rider)

Who Can Consider Paripoorna Mediclaim Ayush Bima?

This policy is useful for CGHS beneficiaries who feel CGHS alone may not be sufficient in all situations. It may be a good option for:

- CGHS pensioners and senior citizens : Medical costs usually increase with age. This policy gives extra financial support during hospitalisation, especially in private hospitals.

- Families using private or non-CGHS hospitals: If CGHS hospitals are limited in your city, this policy offers wider hospital choice and cashless treatment.

- Those who prefer cashless treatment : CGHS reimbursements can take time and paperwork. This policy helps by reducing upfront payments through cashless claims.

- People worried about costly or advanced treatments : Modern medical procedures can be expensive. This policy provides additional coverage for such treatments.

- Those who use AYUSH treatments : If you prefer Ayurveda, Yoga, Unani, Siddha or Homeopathy, this policy offers good in-patient AYUSH coverage.

- Cost-conscious CGHS beneficiaries : With lower premiums and no GST, it is likely a more affordable way to get extra health cover.

- Those looking for extra protection : This policy is meant to add to CGHS, not replace it, and provides peace of mind during medical emergencies.

Paripoorna Mediclaim Ayush Bima offers CGHS beneficiaries an optional way to boost their health coverage. While it is not mandatory, those seeking extra protection and peace of mind may find it a worthwhile addition to their existing CGHS benefits.

Before buying, it’s important to check policy details such as exclusions, waiting periods for pre-existing conditions, sub-limits on certain treatments, co-pay, room rent caps and other terms. Compare these elements with other retail health insurance options to decide what best fits your needs and budget.

Disclaimer: Detailed premium rates for Paripoorna Mediclaim Ayush Bima have not yet been officially released. This article is based on information available at the time of publication and may be updated or revised as new details become available.

Continue reading:

- All LIC Plans Returns Analysis 2026: How Much Do LIC Policies Really Return?

- Latest Health Insurance Incurred Claim Ratio 2025 | Top Health Insurance Companies List

(Post first published on : 16-Jan-2026)

Join our channels