The Union Budget 2026, presented on February 1, 2026, has introduced a significant compliance relief for resident individuals and HUFs (Hindu Undivided Families) purchasing immovable property from Non-Resident Indians (NRIs).

The update focuses on simplifying the Tax Deducted at Source (TDS) process, which has historically been a major pain point for individual buyers.

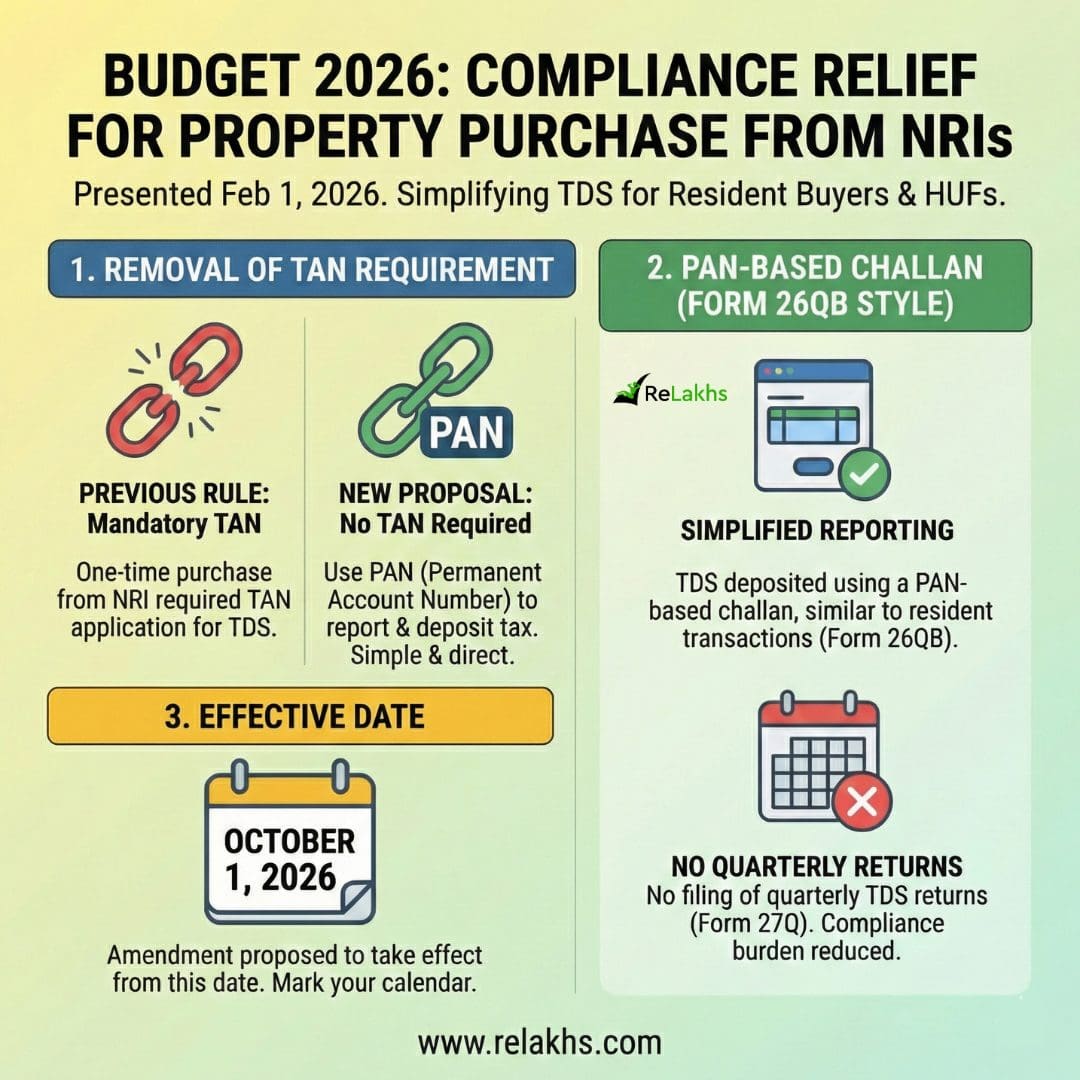

Buying Property from NRI? New Simplified Tax Compliance Rule

1. Removal of TAN Requirement

The most critical change is the scrapping of the mandatory TAN (Tax Deduction and Collection Account Number) requirement for these transactions.

- Previous Rule: Even for a one-time purchase from an NRI, a resident buyer was required to apply for and obtain a TAN to deduct and deposit TDS.

- New Proposal: Resident individuals or HUFs are no longer required to obtain a TAN. You can now use your PAN (Permanent Account Number) to report and deposit the tax.

2. PAN-Based Challan (Form 26QB Style)

The process will now align with the way property transactions between two resident Indians are handled.

- Simplified Reporting: TDS will be deposited using a PAN-based challan, similar to the existing Form 26QB used for resident-to-resident transactions (where the property value exceeds ₹50 lakh).

- No Quarterly Returns: By removing the TAN requirement, buyers are also spared from the hassle of filing quarterly TDS returns (Form 27Q), which was a common compliance burden for individual home buyers.

3. Effective Date

This proposed amendment to the Income Tax Act is proposed to take effect from October 1, 2026.

| Feature | Old Rule (Pre-Budget 2026) | New Rule (Post-Oct 1, 2026) |

| Identification | Mandatory TAN for the buyer | Buyer’s PAN is sufficient |

| Payment Mode | TAN-based Challan (ITNS 281) | PAN-based Challan (Simplified) |

| Filing | Quarterly TDS Return (Form 27Q) | No quarterly returns for individuals |

| Compliance | High (Complex for one-time buyers) | Low (Aligned with resident sales) |

Continue reading:

- Checklist of All Important Property Documents in India

- Why Property Mutation Matters in India—Even If It Doesn’t Create Title Ownership!

(Post first published on : 01-Feb-2026)

Join our channels