The Reserve Bank of India (RBI) has recently released its fifth bi-monthly rate review of financial year 2019-20. Though the key interest rates have been kept unchanged, the RBI has been cutting the rates since February 2019.

There have been five consecutive rate cuts from RBI – in February, April, June & August of calendar year 2019. Also, the central bank has indicated that there is a possibility of further rate cuts in the near future. This signals a further downtrend in bank deposit and lending rates in India.

In this scenario, most of the banks and corporates may also reduce the interest rates on their deposits schemes, Bonds, NCD Public Issues etc.,

This may induce many small investors to look out for better fixed income products which can give decent fixed rate of return.

NCDs or Non Convertible Debentures are one of the fixed income options that can satiate investors’ hunger for better yield. But, don’t forget this rule of thumb – “the higher the risk, the higher the potential return.”

So, what is a Debenture?

Debenture is a type of Debt instrument which offers a fixed rate of interest for a specified tenure. Companies or governments use debentures to borrow money. Debentures are simply loans taken by the companies and do not provide the ownership in the company.

What are NCDs?

Debentures are of two types Convertible and Non-Convertible. The convertible debentures are the ones that can be converted into equity shares at a later time. This convertibility provides attraction to the investor but yield lower interest rates. Non convertible debentures does not convert into equity shares thus can yield a higher interest rate.

An NCD can be Secured or Unsecured. Secured NCDs are backed by the issuer company’s assets to fulfill the debt obligation unlike unsecured NCDs. Below is a short video on ‘basics of NCDs’.

L&T Finance NCD December 2019 Public Issue : Key Features

L&T Finance Limited (L&TFL) is part of the larger L&T Group which is one of the leading business conglomerates in India. It is one of the leading private non-banking financial services companies in India. Its primary financing business segments are rural, wholesale and housing.

- L&TFL’s rural business comprises farm equipment finance, two-wheeler finance and micro loans.

- Its wholesale business comprises of infrastructure finance, supply chain finance and structured corporate finance.

- L&TFL’s housing business comprises of loans against property and real estate finance.

Below are the few important details about upcoming L&T Finance NCD December 2019 Issue (FY 2019-20) ;

- NCD Issue opening Date : 16th Dec, 2019

- Issue Closes on : 30th Dec, 2019.

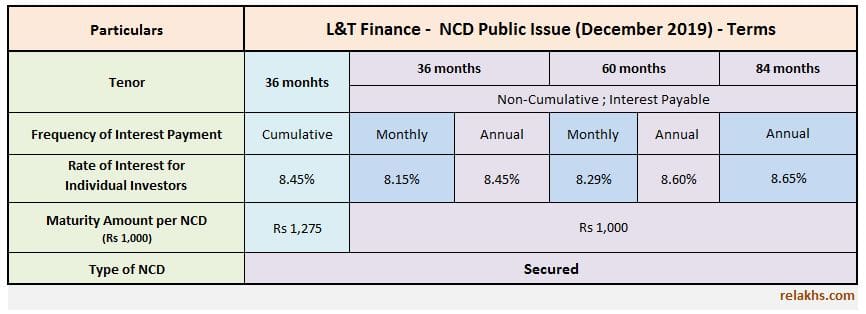

- Interest Rate or Coupon Rate on NCDs : The ROI ranges from 8.15% to 8.65% depending on the category of investor and tenure of the NCDs.

- Issue Size : Base Issue size is Rs 500 cr (with an option to retain over-subscription amount of up to Rs 1,000 cr for Tranche-II Issue.)

- Mode of Issue : Demat only

- Face Value or Issue Price of one NCD is Rs 1,000.

- Available Tenor options : 36 / 60 / 84 months

- Frequency of Interest payment : Monthly & Annual. Cumulative option is available for 36 month NCD Series.

- Minimum Application size : Rs 10,000 (10 NCDs) and in multiple of Rs 1,000 thereafter.

- Listing : The NCDs are proposed to be listed on BSE stock exchange.

- Security & Asset Cover : The Company and Promoter will create and maintain appropriate security in favour of the Debenture Trustee for the NCD Holders on the assets adequate to ensure required asset cover for the Secured NCDs.

- Credit Ratings : CARE, Crisil and Ind Rating have rated these NCDs as AAA/Stable which indicate that instruments with this rating are considered to have the highest degree of safety regarding timely servicing of financial obligations and carry lowest credit risk.

- Issue Allocation Ratio : 45% of the Issue is for retail investors & 35% for HNIs (HNIs – individuals (applying for an amount of > Rs 10 lakh).

- Allotment of NCDs is on ‘first come, first serve’ basis.

- NRIs are not eligible to apply to this NCD issue.

Latest L&T Finance NCD December 2019 Issue – Coupon Rates

In the last L&T NCD issue (April 2019), the interest rates were in the range of 8.66% to 9.05%. Whereas, the current NCD Issue has the highest coupon rate @ 8.65% .

What are the Tax Implications on NCDs?

- TDS is not applicable on the listed debentures’ interest payouts (which are in Demat form). Else, TDS will be applicable if the interest exceeds the threshold limit of Rs.5,000/- in a financial year.

- Interest earned on NCD bonds is taxable as per the tax slab of the investor.

- If you sell NCDs on stock exchange before one year from the date of purchase, Short Term Capital Gains Tax is applicable. Tax rates depend on the tax slab you fall into.

- If you sell NCDs on stock exchange before maturity but after one year, Long Term Capital Gains Tax (if any) at 10% without indexation is applicable.

- Listed Debentures : Holding period 1+ year to qualify as LTCG. LTCG tax rate @ of 10% without indexation & STCG tax rate is as per ‘income tax slab rate’.

- Unlisted Debentures : Holding period of 3 year to qualify as LTCG. STCG is taxed @ as per income tax slab rate. LTCG of 20% without indexation.

Should you invest in L&T Finance NCD December 2019 Issue?

We all are aware that interest rates on fixed income securities have already reached their lowest levels. With the possible rate cuts by the RBI in the near future, we may witness further decline of bank deposit and Small Saving Schemes rates.

Hence, the interest rates offered on Secured NCDs may look attractive when compared to other fixed income products like bank deposits or small saving schemes.

But, are NCDs totally risk-free? – No, they are not risk-free. These carry higher risk than bank deposits. The main risk with NCDs is default risk. The issuer may not be able pay the interest payments. Example : The recent case of DHFL.

Kindly understand the risks associated with NCDs and then take informed decision.

The NPA (Non-Performing Assets) related problems have been plaguing the banking sector (NBFCs as well). The current cash/liquidity crunch (DHFL/IL&FS Saga) have a deeper impact on NBFCs businesses.

The main risk with NCDs is default risk. The issuer may not be able to pay the interest payments. NCD Issuers, especially the top business groups, normally do not default but when things go drastically wrong, they may face problem in paying the investors. In such a scenario, secured NCD holders (if any) would be given higher priority than the holders of Subordinated NCDs. But, do not invest your entire investible surplus in one Company’s NCD Issue.

Given the highest credit ratings (ratings can change anytime) of this L&T Fin NCD Issue, if you could afford to take some risk, are looking for regular interest income and are in 10% or 20% income tax slab rate, you may consider investing in 36 month NCD Series. If you are in the highest tax slab, you may also consider investing in Tax Free Bonds from Secondary Market.)

Before investing in NCDs, kindly calculate your post tax returns on debentures and take your decision, as the interest payouts are taxable.

Post-tax returns = Pre-Tax returns * { (100-Tax Rate) / 100 }

In case, you can not afford to take any sort of risk, suggest you to stick to Bank FD/RD and Post office Small Saving Schemes.

Depending your risk profile and investment horizon, you may consider other alternative fixed income avenues like Debt oriented Mutual Funds, Hybrid Mutual Funds, Tax Free Bonds, Post office MIS scheme, PPF, Post office Senior Citizen Savings Scheme, 7.75% GoI Bonds etc.,

You may go through my article on snapshot of the most popular investment options in India.

Continue Reading :

- Best Company Fixed Deposits 2019-20 | Are Corporate FDs Safe?

- Best Lump sum Investment options for Retirees/Senior Citizens to get Regular Income?

(Post first published on : 12-December-2019)

Join our channels