Sovereign Gold Bonds Scheme is an indirect way of investing in Gold. Instead of buying physical gold, investors can buy gold in paper form through Sovereign Gold Bonds. These bonds track the price of gold, plus an extra interest amount is paid on the investment.

The Reserve Bank of India, in consultation with the Government of India, has decided to launch latest Sovereign Gold Bonds Issue Series-III (FY 2017-18). Applications for the bonds will be accepted from 9th October, 2017 to 27th December, 2017. The Bonds will be issued on the succeeding Monday after each subscription period. (SGB Series III was launched in the month of July- 2017.)

This is the third tranche of the Financial Year 2017 – 2018. The Gold Bonds scheme was launched in November 2015.

The Budget (2017) has set a target to garner as much as Rs 5,000 crore from the three gold schemes for the fiscal 2017-18. These schemes are namely – Sovereign Gold Bonds, Gold Deposit Scheme & Indian Gold Coins.

Latest Sovereign Gold Bonds Issue Series-III (Oct-Dec 2017) : Issue Details

Applications for the latest ‘Sovereign Gold Bonds Scheme’ will be accepted from 9th Oct, 2017 through banks, Stock Holding Corporation of India Limited (SHCIL), designated post office branches and stock exchanges (BSE & NSE).

Below are the key features of Sovereign Gold Bonds Scheme Oct – Dec 2017 ;

- Latest Issue Subscription dates : 9th Oct, 2017 to 27th Dec, 2017.

- Calendar of Bonds Issuance : The Sovereign Gold Bonds will be issued every week from October 2017 to December 2017 as per the calendar specified below ;

- Public Issue Price : The government has fixed the Issue price for next subscription period i.e. December 18th to 20th, 2017 would be Rs. 2,866 per gram with Settlement on December 26, 2017. (The issue price of the Gold Bonds is based on the simple average closing price published by the India Bullion and Jewellers Association Ltd (IBJA) for gold of 999 purity of the week preceding the subscription period. A discount of Rs 50 per gram from the issue price is offered to those investors who invest through online mode.)

- Who can buy Gold bonds? : The Bonds will be restricted for sale to resident Indian entities including individuals, HUFs, trusts, Universities and charitable institutions.

- Duration of Bonds : The tenor (tenure) of the Bond will be for a period of 8 years with an exit option from 5th year onwards. Gold bonds shall be repayable on the expiration of eight years from the date of the issue and premature redemption is permitted after 5th, 6th and 7th years from the date of issue of SGB.

- Minimum investment Size : Minimum permissible investment will be 1 unit (i.e. 1 gram of gold.)

- Maximum allowed investment : The maximum amount subscribed by an entity or an individual investor will not be more than 4 kg per financial year (April-March). A self-declaration to this effect will be obtained. In case of joint holding, the investment limit of 4 kg will be applied to the first applicant only. The annual ceiling will include bonds subscribed under different tranches during initial issuance by Government and those purchase from the Secondary Market.

- Interest rate on Gold Bonds : The investors will be compensated at a fixed rate of 2.5% per annum payable semi-annually on the initial value of investment. Interest will be credited directly in to the account mentioned in the application form or in the Account linked with the Demat a/c. (It is mandatory for the investors to provide bank account details to facilitate payment of interest /maturity value.)

- Where to buy Gold Bonds ? : Gold Bonds can now be purchased from NSE and BSE, besides all Bank branches, select Post Offices and the Stock Holding Corporation of India Limited (SHCIL) and as may be notified, either directly or through agents.

- Payment mode : Payment for the Bonds will be through cash payment (upto a maximum of Rs. 20,000) or demand draft or cheque or electronic banking.

- The investors will be issued a Holding Certificate. The Bonds are eligible for conversion into demat form.

- KYC Documentation : Know-your-customer (KYC) norms will be the same as that for purchase of physical gold. KYC documents such as Voter ID, Aadhaar card/PAN or TAN /Passport will be required.

- Transfer of Bonds : The bond can be gifted/transferable to a relative/friend/anybody.

- Redemption Price : The redemption price will be in Indian Rupees based on previous week’s (Monday-Friday) simple average of closing price of gold of 999 purity published by IBJA (Indian Bullion Jewelers Association).

- Collateral : Gold Bonds can be used as collateral for loans. The loan-to-value (LTV) ratio is to be set equal to ordinary gold loan mandated by the Reserve Bank from time to time.

- Liquidity & Tradability : Bonds will be tradable on stock exchanges within a fortnight of the issuance on a date as notified by the RBI.

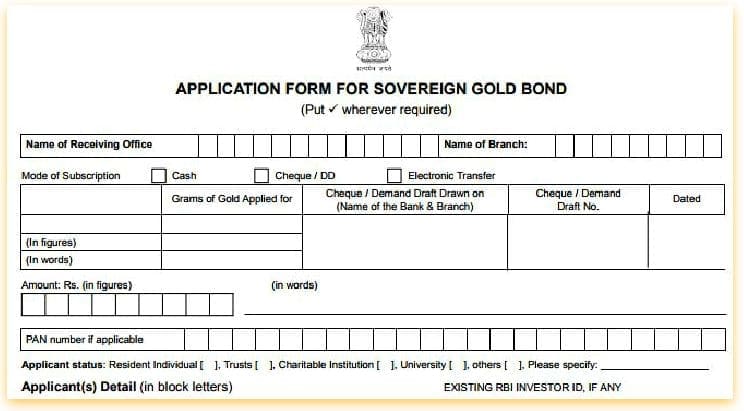

Sovereign Gold Bonds Application Form for Series III of FY 2017-18

Click on the below image to download Gold Bonds Application form 2017-18 Series -III (Oct – Dec 2017).

Sovereign Golds Bonds & Tax Implications

- The interest payments on Gold Bonds shall be taxable as per the provision of Income Tax Act.

- Gold bonds will be exempted from capital gains (LTCG) tax at the time of redemption.

- However, kindly note that Long term capital gains arising to any person on transfer of SGB will continue to be taxable and eligible for indexation benefits.

- TDS is not applicable on the bonds. However, it is the responsibility of the bond holder to comply with the tax laws.

Should you buy Gold Bonds?

The main benefit of Gold bonds is, you may get capital appreciation (if gold prices increase) plus ‘interest payment’ on bonds. If you buy physical gold or Gold ETFs (which also track gold prices), you may get capital appreciation only. Neither physical gold, gold mutual funds nor gold ETFs pay any interest rate.

If you buy Gold mutual funds or Gold ETFs, you have to bear ‘fund management charges’. In case of Gold bonds, no charges are applicable. Also, like gold funds and ETFs, you don’t have to worry about storage of physical gold or pay locker fees in case of Gold Bonds.

The biggest disadvantage of Gold bonds is lack of liquidity. The lock-in period is 5 years. But you can sell the bonds on stock exchanges. During last fiscal, stock exchanges BSE and NSE had launched online bidding platforms for SGBs. The exchanges will act as receiving offices for this tranche also. The online platforms are expected to raise demand for SGBs in the demat form.

If you HAVE to invest a portion of your savings in Gold for long-term, Gold bonds outscore the Gold funds / physical gold and can be a preferred mode of investing in Gold. (Related Article: ‘Best Gold buying options‘)

If there are uncertainties across the globe and if the geo-political risks are high (for example : conflict between North Korea and the USA), generally Gold prices tend to increase. Investors tend to take refuge in assets like Gold.

Personally, I have never invested in Gold. The extent of volatility of Gold prices in the recent years is more than that of Equity oriented securities/funds. So, the risk-reward ratio may not be favorable for investing in Gold.

(Post first published on : 07-October-2017)

Join our channels

WHERE TO DOWNLOAD GOLD BOND CERTIFICATE ISSUED ON OCT 23, 2017

Dear Manoj..If you have subscribed through any banks/Post office branch (offline), you can request them to issue the physical bond certificates.

Hi Sreekanth,

The bond can be gifted/transferable to a relative/friend/anybody…But do they need to have a demat account? And, what’s the procedure for that?

Thanks in advance.

Dear Shailesh,

You may contact your banker/service provider where you have bought these bonds, they can guide you in this regard.

As per the RBI website, one can submit Form F for transfer of bonds.

Kindly go through these links ;

Link – 1

Link – 2 (Form F)

Sreekanth,

I have a query. Once these bonds are matured, how will I get back my accumulated amount. Whether it will automatically gets credited to my amount (similar to how FD matures) or I need to carry the bonds to banks and request them to credit it.

And one more query. Is it mandatory to save the paper bonds issued by banks? I will have the payment receipt right for my safety.

Thanks!

Dear Jagan .. The investor has to submit the bond certificate at the bank, and the amount gets credited to the bank account that has been given/updated in the application.