Every year, IRDA (Insurance Regulatory & Development Authority) publishes Incurred Claims Ratio (ICR) data in its annual report. ICR is one of important factors that you can consider when buying a health insurance plan.

What is Incurred Claims Ratio (ICR)?

Incurred Claims Ratio is nothing but the total value of all claims paid by the health insurance company divided by the total amount of premium they collected in the same period. Incurred Claims Ratio indicates the company’s ability to pay the claims.

As an example a 70 percent incurred claims ratio means that for every Rs 1000 of premium earned in a given accounting period, Rs 700 is paid back in the form of benefits (claims). Incurred Claim ratio is the ratio of the claims settled to the premium received.

So, how to analyze the ICR data? Whether a Non-life Insurance company which has say ICR of 120% is better than a company which has incurred claims ratio of say 75%?? Let us now understand this point.

If ICR is greater than 100%, it means that the company has given more money away as claims than what it has collected as premium. This is not good for the company.

If ICR is less than 100% say in the range of 60% to 90%, it means that the health insurance company has given lesser amount as claims than what it has collected. It means that they are making profits.

If ICR is very low say 30%, it means that either the company is charging higher premium rates than its peers and making huge profits (or) it has a good pool of low-risk (may be youngsters) profile individuals as clients (or even both).

Hence it is better to be with an insurance company which has neither high nor low incurred claim ratio. I believe that the ideal ratio (percentage) range can be anywhere between 60% to 90%.

The main difference between Incurred Claims Ratio and Claim Settlement ratio is – Incurred Claim ratio is the ratio of the claims settled to the premium received. Claim Settlement Ratio (CSR) is the ratio of claims approved to total claims made (received). The higher the CSR the better. Same is not the case with ICR.

Non-Life Insurance companies provide products under various segments like Motor, Health, Home, Personal Accident, Travel, Marine and other types of Insurances. In this post, we are analyzing the ICR details of Health Insurance vertical only.

Non-Life Insurance Business in India 2015-16

- The non-life insurance industry underwrote total direct premium of Rs 96,379 crore in India for the year 2015-16 as against Rs 84,686 crore in 2014-15.

- The public sector insurers exhibited growth in 2015-16 at 12.08% ; over the previous year’s growth rate of 10.24%.

- The private general insurers registered a growth rate of 13.12%, against 9.62%growth rate during the previous year.

- The standalone health insurers registered a growth rate of 41.12% in 2015-16 as against 31.07% growth rate during 2014-15.

- ICICI Lombard continued to be the largest private sector non-life insurance company, with market share of 8.39%.

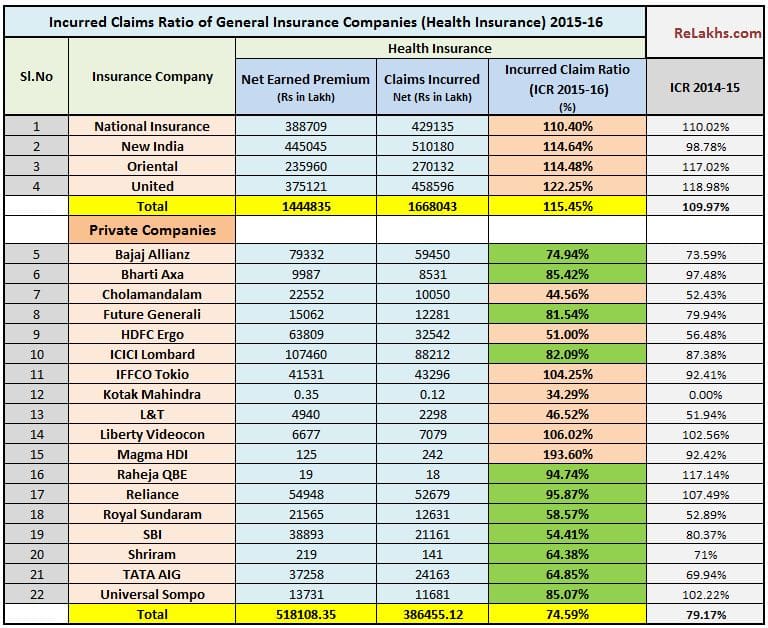

Health Insurance & Latest IRDA Incurred Claims Ratio 2015-16

Below are the details of Stand-alone Health Insurers’ incurred claims ratio during 2015-16;

- The incurred claims ratio of all four public sector General Insurance companies was more than 100% in 2015-16.

- The incurred claims ratio (net incurred claims to net earned premium) of the Public Sector non-life insurance companies (health insurance vertical) was 115% during 2015-16 which is higher than the previous year figure of 109%.

- The incurred claims ratio of the Private Sector non-life insurance companies (health insurance vertical) was 74% during 2015-16 which is lesser than the previous year figure of 79%.

- The incurred claims ratio of the stand-alone Health Insurance companies was 58% during 2015-16 which is lesser than the previous year figure of 62%.

- You can notice that Public sector non-life insurance companies like National Insurance, New India, Oriental & United have Incurred Claim Ratios of more than 100%. So, does this mean that the PSU Non-life insurance companies are making losses? Kindly note that these companies also provide other types of insurance covers like Fire, Marine, Travel, Motor etc., Their health insurance vertical may not be making profits but other verticals might be generating profits.

- As far as Private General Insurance companies are concerned, the ones which have reasonable and are close to total average ICR (avg ICR of all Pvt companies is 74.59%) have been highlighted in GREEN. You may prefer buying health insurance policies from these companies.

- All the stand-alone ones or the specialized health insurance companies like Apollo Munich, Max Bupa, Religare & Star Health have good Incurred Claims Ratio which is around 60%. So, these can be preferred to other ones when buying a mediclaim or family floater health insurance plans.

- Kindly note that the industry’s average figure (the average ICR of non-life & stand-alone health insurance companies) is 68.53%.

When it comes to health insurance, there is no one-size fits-all plan that you can rely on. Medical Insurance is a contract based policy with legal jargon thrown in. Besides this, a Health Insurance policy has medical terminologies. Of the numerous medical insurance plans in the market, you may find that each one is unique in some way or the other, with its own benefits and limitations.

The Incurred Claim Ratio (or) Claim Settlement Ratio can help you in shortlisting the best health insurance companies but you have to do a lot of research to identify the right and best health insurance plan which suits your requirements. You have to make a comparison of health insurance plans offered by multiple companies. This is where I believe that health insurance comparison websites could be beneficial.

Actually, Claim Settlement Ratio can be a better indicator than ICR for shortlisting best health insurance companies. But IRDA does not publish CSR details for Health Insurance in its annual report. The CSR details are available in respective company websites. I tried to collate CSR details by visiting respective company websites, but the data which is available is incomplete. You can find data under ‘public disclosures’ menu option.

Continue reading:

- Best portals for comparing Health Insurance Plans

- Evaluate these important factors when buying a Health Insurance plan

(Image courtesy of fantasista at FreeDigitalPhotos.net) (Reference & Source : IRDA Annual Report 2015-16) (Post published on : 22-December-2016)

Join our channels

Sir I m planning to medical policy 5 lacs for a family my age 30, wife 31, son 2, daughter 5, daughter 9 year. Which policy is best claim sattelment. Apollo OR Religare ? Reply fast

Dear BHARAT…Both have decent Incurred claim ratios.

Based on the above ratios, the premium rates of Religare plans can be higher than the Apollo’s.

Based on your requirements you may shortlist a plan..

Suggested readings :

Best portals to compare health insurance plans

Evaluate these important factors when buying an health insurance plan

Best family floater health insurance plans

i am having a HDFC Ergo MEdisure Classic Policy with basic cover of 5 lacs and reinstatement of 5 lacs in case of accident. i am thinking of porting to Cigna TTK PRo Health Plus. I am single with no prior history of any hospitalisation. Which would be a better policy and which is a good company ??

Dear siddharth…Health insurance is more of a personal choice based on ones requirements..

May I know why do you want to port to Cigna?

Kindly read :

Important factors that need to be considered when buying an health insurance plan

Best portals to compare health insurance plans

Hey Sreekanth I have a query regarding my parent’s medi-claim policy, is it viable to go for a private insurer for atleast the policy (1) ? Or should we continue with New India for both these policies? The reason I’m asking is that i have heard the private ones are much competitive in terms of premiums and service.

Policies:

Age: Dad-53,Mother-50

Pre-Condition: Mother- Diabetes(in control), Dad- None

Current Policy:

1) New India Assurance Co.- New Mediclaim 2012

Dad(proposer)- Sum Insured-5lac, bonus buffer- 63k,

Mother-Sum Insured-5lac, bonus buffer- 63k

Sister- Sum Insured-2lac, bonus buffer- 30k

Net Premium- 13k+11k+3k=31k

2) New India Assurance Co.- Top-up Mediclaim floater policy-

Threshold-5lac/-

Sum Insured- 15lac/-

Premium- 5600+2800= 9660/-

Hi,

As far as premiums are concerned, the public sector General insurers are equally competitive. But in my experience too, when it comes to service, Pvt insurers do fare well.

Is the first one Family floater one? May I know your sister’s age?

Suggestions: As your mother is a diabetic, she may consider opting for stand-alone Diabetic specific plan.

In my view, a super top-up plan is better than a top-up plan.

Kindly read : Super Top up plan Vs Top up health insurance plans..

In case, you wish to discontinue this policy, you can consider the option of PORTING it to a pvt insurer.

Is the first one Family floater one?

No it is an individual one with individual coverages.

May I know your sister’s age?

She’s 25, unmarried & a working professional

I have checked to port with coverfox.com, waiting for them to respond with a plan.

Also I would like to know if we should stick with this individual policy or go for a floater instead?

Hi,

You may continue with individual mediclaim policies.

Hi Srikant,

I m looking for health insurance for 2 adult + 1 child, currently i m in delima either to go for Cigna ttk / Applo munich or HDFC ERGO.

I m already holding HDFC ERGO for my mom, but they cheated with me. At the time of renewal they confirmed me will be providing Health Coupon but after renewal they turned down. I asked them to listen recorded session at the time of renewal but they still denies.

Kindly suggest good Health Insurance so I can go for it, who claim settlement ratio is excellent.

Dear Jagdish ..It is tough to suggest a health plan…requirements can vary from family to family.

Suggest you to go through below articles :

Best Family floater health insurance plans

Best portals to compare health plans

Important factors that need to be evaluated when buying a health insurance plan

Dear Srikant,

I want to purchase health insurance policy for 2Adults + 1Child of Rs. 3,00,000 Sum assured. I am have shortlisted HDFC Ergo Medisure Classic with CI, Apollo Munich Optima Restore and Max Bupa Health Companion. But I am confused after seen their low “Incurred Claim Ratio”. So request you to guide me which will be better for service and claim settlement purpose.

Thanks & regards.

Dear Mridul ..Apollo has a decent ICR..Kindly do not confuse ICR with claim settlement ratio..

Suggested readings :

Vital factors that need to need to be considered when buying a health insurance policy..

Best portals to compare health plans

Best Family floater health insurance plans

Ok Thanks. Will decide according to Claim settlement ratio only.

Regards.

hello Sreekanth sir

i follow your web site from past 1 year really helpfull project thanks for such grateful effort

my question is

1. star mediclaim give joint replacement cryosurgery after continuous period 2 year oprat policy (when port policy bajaj to star)

2. i confuse between cigna ttk & universal sompo mediclaim

please help me sir and any friend also he expert in question

Thank you in advance

Dear pradeep,

Thank you for being a loyal reader!

I am unable to understand your query. Kindly re-phrase it!

Kindly read : Best portals to compare health insurance plans!

hello sir for replay

1. actually that problem face my mother (she 51 years old ) from past 2 to 3 month ……i plane to do surgery next renewal after july 2018

my previous policy was bajaj just portability with star (star told me wecover after continuous 24 month only in when portability case )

please make sure is it right???

note – because no any preexist diseases mention on bajaj policy…

2. i confuse between cigna ttk & universal sompo mediclaim (this policy take for me age is 31 years old)

Thank you sir

Dear pradeep,

1 – If you are planning for a surgery, and if that treatment is covered by Bajaj, suggest you not to do Porting now.

2 – Kindly go through the suggested article, compare the plans and opt for the one which meets your requirements.

Hi,

Want to buy one health insurance for my mother her age is 55 & she is absolutely fine excepts BP low issue sometimes.

Good Health Policy included which I prefer,

No capping system on room rent, No Co-payment option, Utilization about restoration amount should be beneficial, Waiting Period, Surely with Low premium.

If anyone could suggest me with the best Plan, really appreciate.

Thanks & Regards

Rachna Mehra

Dear Rachna,

You may go through below articles ;

Best portals to compare health insurance plans.

Best health insurance plans for parents.

Good information regarding health insurance provided

Thanks

I’m planning to take health insurance for my parents above 60. I choose star health senior citizen red carpet since it din’t have premedical tests. But when I looked at ICR, it had come down from 63% to 53% for 2015-16. Is it still recommendable do go with star health as the numbers doesn’t looks promising in terms of ICR?

NOTE – My parents are healthy doesn’t have major health ailments except for BP & Diabetes.

Dear Madhan,

In case they have BP or diabetes, may be it is advisable to go with Diabetic or hyper tension oriented plans ??

Dear Sreekanth,

Thanks for your reply. How about my query on ICR for Star Health. It has come down drastically from 63% to 53%? Does this number have major impact on claims settlement?

Dear Madhan ..I dont think it should not be of a great concern.

Personally, I also have a family floater plan with STAR (just a disclose and not a recommendation).

I am planning to go for Apollo Munich Optima Restore. The reason for selecting this plan is life long renewals beside Restoring feature if Sum Assured gets exhausted. Please provide your opinion. I am ok if this plan costs a little bit high

Dear Sreedhar ..If the plan is affordable to you and its features meet your requirements, you may kindly consider it.

Read:

Best portals to compare health insurance plans.

Evaluate these important factors when buying a health insurance plan.

pls look Religare Care Product which give you and your family Annual health check absolutely free apart from restoring feature of Sum assured and life long renewals and also NO CLAIM BONUS upto 150%

Which one is good Mediclaim or Health insurance?

Religare health insurance

Hi Shrikant,

I am looking for a health plans for self and my parents.

Father 56 and mother 54 years old. Both are fit and find till date. No medical problems till date.

I am looking for sum assured 3-5 lakhs.

I just shortlisted HDFC Eargo Health Suraksha Gold with Regain & ECB and Max Bupa Family Plan.

Max Bupa also provide extended Family Plan which include Me with my parents.

But I get some negative reviews from my contacts about Max Bupa for service and management.

Can you please suggest.

Thanks & regards,

Ankit Patel

Dear Ankit,

Kindly go ahead with a plan which meets your requirements.

But, suggest you to take separate plan(s) for your parents and do not make them part of your mediclaim.

Kindly read:

Best portals to compare health insurance plans.

Best health insurance plans for parents.

Important factors that need to be considered when buying a health insurance plan.

Thanks for your comments.

Yes, of course I need to go for separate policy for parents and me.

But as per your experience and knowledge, is Max Bupa performance good and trustable.

Thanks & regards,

Ankit Patel

Dear Ankit,

To be frank it is very tough to suggest a best suitable health insurance plan.

Based on my interactions with my blog readers, Max bupa is a decent choice. Kindly go through the Policy wordings, Sub-limits, Clauses etc., before taking final decision.

Thanks for your comments.

Go For religare product called CARE

Hi Sreekanth,

last year i have taken Religare insurance policy individually for me,my wife..these two policies are for 3Lakh along with [No claim Bonus – Super ] Add on Benefit feature.

I have admitted to hospital for Diarrhoea and gastroenteritis. But claim has been rejected stating that “Admission not justified”, though a need to admit in hospital for two days.

I am completely disappointed and thinking not to go for renewal.

Please suggest me if that is the right opinion according to you. If not, state the reasons.

If yes, can you give alternatives

Dear venkat,

That’s why health insurance products are the most complicated ones to understand.

Suggest you to stick with these plans.

Dear sir,

I Yogesh verma and Want to purchase health insurance policy 2A +1 and Rs. 300000 Sum assured. I am Confused that Should I buy from Priate Co. and Govt. Co. If pvt. so Which Co as as govt. co. So pLz guide me which will be better for service and claim settlement purpose.

Dear Yogesh,

Suggest you to compare plans and take final decision as per your requirements.

Read : Best portals to compare health insurance plans.

Religare Health

Hello Sreekanth!

I have an existing health insurance policy from Religare. I am looking for a Super Top Up plan to add to it.

As such I have not made any claim in last 4 years, so cannot comment on the service quality of the company. But in general sense, is it recommended to go for the same company for super top up, considering there will not be any disputes if any such cascading claim arises in the future?

Regards,

Amit

Dear Amit,

Advisable to have super top up plan from the same company (though not mandatory), if meets your requirements.

Read : Best Super Top up health insurance plans.

Absolutely go ahead with Religare health

Hi Srikant,

My wife and I have got a family floater L&T Classic Health Insurance. The main reason we went for it was lesser premium and no cap on room rents. We bought through coverfox.

However, looking at the ICR stats I really doubt this choice. What do suggest – should we switch?

Thanks.

Zubin

Dear Zubin ..HDFC Ergo has acquired L&T insurance in 2016. So, things might change. Suggest you to continue with it for one or 2 years, if you are not satisfied with their service levels you can PORT your policy to some other General Insurer.

Thank you so much for your advice.