When you invest your hard-earned money, there’s one question that often gets overlooked: “Will I be able to withdraw my money when I need it?”

Many investors focus only on returns and forget an equally important factor—liquidity, or how easily you can access your money. But the reality is, some investments lock your money in for years, and exiting early can be difficult, expensive, or sometimes not possible at all.

Let’s make sense of lock-in periods and withdrawal rules across popular investment options in India.

What is a Lock-in Period?

A lock-in period is the minimum time you need to stay invested before you can withdraw your money.

Early withdrawal may not be allowed, and in some cases, it can also attract a heavy penalty. On the other hand, if you stay invested for the full lock-in period, you can enjoy the complete benefits.

In simple words, think of it as a “no exit” rule for a fixed period.

Why Lock-in Period Matters

Ignoring lock-in rules can create cash flow problems during emergencies, lead to penalties or lower returns, and even force you to stay invested in products you no longer want. That’s why liquidity is just as important as returns when choosing an investment.

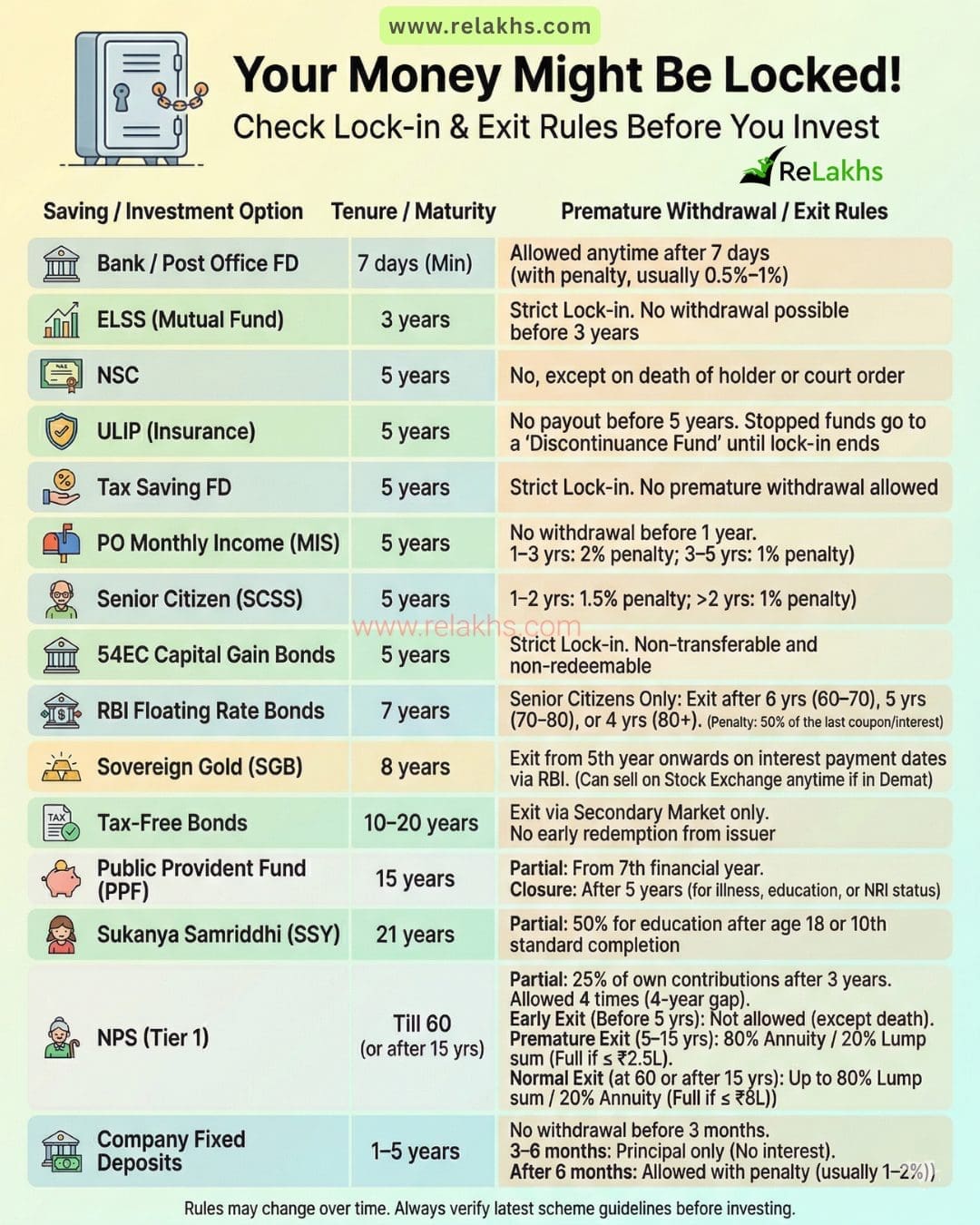

Popular Investments | Lock-in Periods & Their Exit Rules

Before you commit your hard-earned cash, you need to know exactly when you can get it back. Here is a breakdown of the lock-in and exit rules for India’s most popular investment options;

Fixed Deposits (Bank / Post Office)

Lock-in is generally a minimum of 7 days. You can withdraw before the period ends, but a penalty will apply (0.5%–1% penalty on the interest). Overall, it offers good liquidity.

ELSS (Tax Saving Mutual Funds)

ELSS funds come with a 3-year lock-in period, and early withdrawal is not allowed. They’re perfect for combining tax savings with long-term wealth creation.

Public Provident Fund (PPF)

PPF comes with a 15-year lock-in period, though you can make partial withdrawals from the 7th year and close the account early after 5 years under specific conditions. It’s ideal for long-term, disciplined savings.

Sukanya Samriddhi Yojana (SSY)

The Sukanya Samriddhi Scheme has a tenure of up to 21 years, with partial withdrawal (up to 50%) allowed after the girl child turns 18. It’s a perfect goal-based savings option for your girl child’s future.

Senior Citizen Savings Scheme (SCSS)

SCSS has a 5-year lock-in period, with no exit allowed before 1 year, and early withdrawal thereafter comes with a penalty. It costs you: a 1.5% penalty if you leave within 2 years, and 1% after that. It’s an ideal choice for retirees seeking steady income.

Post Office Monthly Income Scheme (PO MIS)

POMIS has a 5-year tenure, but premature withdrawal comes with rules: no exit before 1 year, a 2% penalty if withdrawn between 1–3 years, and 1% penalty between 3–5 years. Perfect for regular monthly income seekers, retirees, or low-risk investors—but it’s not very liquid in the first year.

Kisan Vikas Patra (KVP)

KVP has a tenure of ~115 months (around 9 years 7 months), designed to double your investment. Premature withdrawal isn’t allowed before 2 years 6 months (30 months), but after that, it’s possible with no major penalty—though your effective returns will be lower. Early exit is only permitted in exceptional cases like a court order or the holder’s death.

National Savings Certificate (NSC)

NSC comes with a 5-year lock-in period, and premature withdrawal is not allowed except in rare cases. A safe, fixed-return option for medium-term goals.

Tax Saving Fixed Deposits

Tax-saving FDs have a strict 5-year lock-in period, and premature withdrawal is not allowed. A secure option for those who can commit to the full tenure.

Tax-Free Bonds

Tax-free bonds typically have a long 10–20 year tenure. The issuer won’t let you exit early, so your only option is to sell them on the secondary market. Great for steady tax-free income, but plan for low liquidity.

54EC Capital Gain Bonds

These are the ultimate commitment—with a strict 5-year lock-in period, and they’re completely non-transferable. Once you invest, you’re in it for the long haul!

ULIP (Insurance + Investment)

ULIPs come with a 5-year lock-in period, and you cannot withdraw funds before it ends. With ULIPs, payouts are only possible after the 5-year lock-in—any stopped funds go into a Discontinuance Fund. Many think ULIPs are flexible—they’re often not!

Sovereign Gold Bonds (SGB)

SGBs have an 8-year tenure, though you can exit after 5 years on specific interest payment dates. You can exit via the RBI after the 5th year, or sell them on the Stock Exchange anytime if you hold them in a Demat account. A smart way to invest in gold with some flexibility built in.

RBI Floating Rate Bonds

RBI Floating Rate Bonds have a 7-year lock-in period, with early exit allowed only for senior citizens (with a penalty of 50% of the last interest payment) under specific conditions. A stable option for those comfortable with the longer tenure.

NPS (Tier 1) – Updated Rules

NPS Tier 1 has a lock-in until age 60 (extendable up to 85), but it’s now more flexible: partial withdrawals are allowed after 3 years, premature exit is possible after 5 years (with annuity rules), and at retirement, you can take up to 80% as a lump sum.

Company Fixed Deposits

Company FDs typically have a minimum 3-month lock-in period, with no withdrawal allowed before that. If you exit between 3–6 months, you might only get your principal back with zero interest. Suitable if you’re okay with slightly higher returns but lower liquidity.

Final Thoughts

A good investment isn’t just about high returns—it’s also about access, flexibility, and perfect timing.

- Before you invest, always double-check these:

- Lock-in period

- Exit rules

- Penalties involved

- Whether it matches your financial goals

Because sometimes, the biggest risk isn’t losing money…it’s not being able to access it when you need it most.

Before investing in any product, follow this simple rule: “No clarity on exit = No investment”

Continue reading:

- Do Small Savings Schemes Interest Rates Change Every Quarter? Fixed vs Variable Explained

- List of 20 Key Central Government Schemes for Personal Finance (Features, Tax & Eligibility Explained)

(post first published on : 07-April-2026)

Join our channels