A new tax era begins! Starting April 1, 2026, India’s tax system enters a major transformation under the Income Tax Act, 2025 — the biggest structural change in decades.

The aim is simpler taxation, but the big question still stands: Old Regime or New Regime — which one should you choose this year?

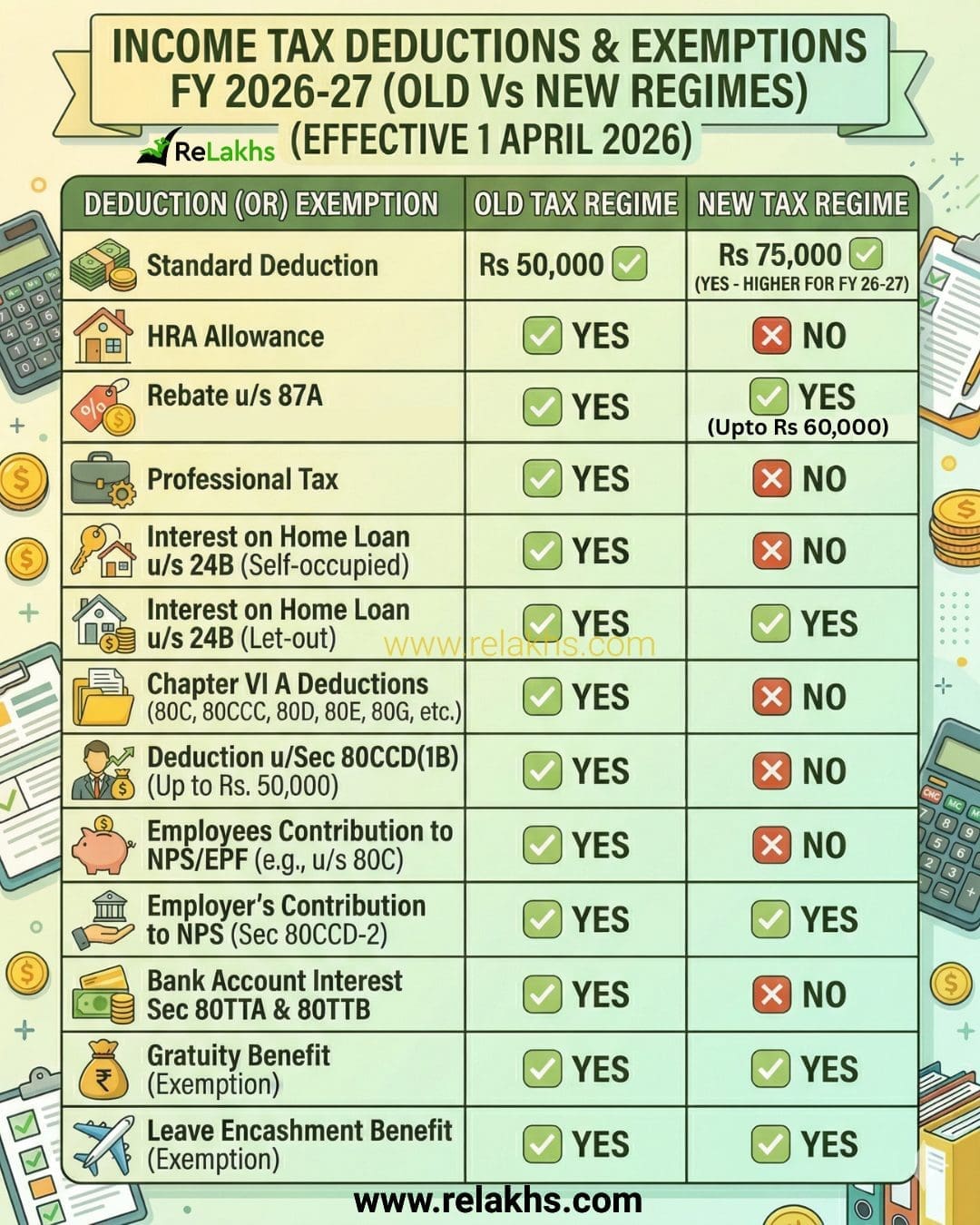

Whether you trust the old, familiar route or plan to switch to the new default regime, here’s a clear breakdown of deductions available for FY 2026–27 to help you decide wisely.

Note: Starting this tax filing year — effective April 1, 2026 — the terms Financial Year and Assessment Year are no longer in use. It’s now simply called the Tax Year, covering income earned from April 1, 2026, to March 31, 2027.

Income Tax Deductions Tax Year 2026-27 – Tax Planning Guide

Income tax deductions for FY 2026-27 differ significantly between the old and new tax regimes. The new regime allows only limited deductions like standard deduction and NPS employer contribution, while the old regime offers multiple benefits under Sections 80C, 80D, HRA, and home loan interest. Choosing the right regime depends on your investments and expenses.

This blog is divided into two simple sections:

- Deductions, Rebates & Exemptions available under both the Old and New Tax Regimes – common benefits you can claim regardless of which regime you choose.

- Deductions, Rebates & Exemptions exclusive to the Old Tax Regime – additional tax-saving options available only if you stick with the traditional system.

A) Deductions Available Under Both Old & New Tax Regimes

Even though the new tax regime removes most deductions, a few important benefits are still allowed.

1. Standard Deduction for Salaried Individuals

The standard deduction remains a powerful tool to reduce your taxable income without any investment proofs.

- New Tax Regime Limit: ₹75,000

- Old Tax Regime Limit: ₹50,000

2. Employer’s Contribution to NPS (Section 80CCD(2))

You can claim a deduction for your employer’s contribution to your NPS account.

Limit: Up to 14% of your salary (Basic + DA) — this applies to both government and private sector employees.

Section 80CCD(2) is effectively the “Section 124” of the new tax era effective 1 Apr 2026.

3. Interest received on Post office Account

Under Section 10(15)(i) of the Income Tax Act, interest received from the post office savings account is exempt from tax for up to Rs 3,500 for individual accounts and Rs 7,000 in the case of joint accounts per financial year. (Note: This is not the same as the Section 80TTA/80TTB deductions.)

4. Family Pension Deduction (Section 57)

If you are receiving a family pension, you are eligible for a standard deduction (pension received by the legal heir of a deceased employee).

- New Tax Regime: The deduction has been increased up to ₹25,000 (previously ₹15,000) or one-third of the pension, whichever is lower.

- Old Tax Regime: It remains at ₹15,000 or one-third of the pension, whichever is lower.

5. Rebate under Section 87A

- New Regime: Rebate up to ₹60,000 — making income up to ₹12 lakh completely tax-free.

- Old Regime: Rebate up to ₹12,500 — income up to ₹5 lakh becomes tax-free.

Note: While not a deduction technically, this rebate plays a big role in reducing your overall tax liability. Also, Section 87A is effectively the “Section 156” of the new tax era effective 1 Apr 2026.

6. Interest on EPF Account

While the New Tax Regime (the default regime) has removed the tax deduction for the amount you invest (under Section 80C), the interest earned on EPF deposit remains exempt from tax in both systems.

| Feature | Old Tax Regime | New Tax Regime (Default) |

| Tax Exemption on EPF Interest | Available (up to limits) | Available (up to limits) |

| Exempt Limit (Private Sector) | Interest on contribution up to ₹2.5 Lakh | Interest on contribution up to ₹2.5 Lakh |

| Exempt Limit (Govt Sector) | Interest on contribution up to ₹5.0 Lakh | Interest on contribution up to ₹5.0 Lakh |

| Tax on Excess Interest | Taxed at Slab Rates | Taxed at Slab Rates |

7. Conveyance Allowance

You can claim income tax exemption for conveyance (official), transport (specially-abled) and other allowances given by your employers under both the regimes.

8. Gratuity & Other retiral benefits

For FY 2026-27 (Tax Year 2026-27), retirement benefits such as Gratuity, Leave Encashment, and Commuted Pension are available under both the Old and New Tax Regimes.

9. Home Loan Interest (Let-out Property) | Section 24(b)

Tthe deduction for Home Loan Interest on Let-out (Rented) Property is available under both the Old and New Tax Regimes for FY 2026-27.

However, while both regimes allow you to deduct the interest, the way you “use” that deduction to lower your overall tax bill is very different between the two. Under the Income Tax Act, 2025 (effective April 1, 2026), the rules have become even more distinct.

In the Old Regime, the tax laws remain very supportive of property investors.

- Deduction Limit: There is no upper limit on the amount of interest you can claim as a deduction against your rental income.

- Set-off of Losses: If your interest payment is higher than your rental income (creating a “loss from house property”), you can set off this loss against your Salary or Business income up to a limit of ₹2 Lakh per year.

- Carry Forward: Any loss exceeding ₹2 Lakh can be carried forward for up to 8 years to be set off against future house property income

In the New Tax Regime (the default regime for 2026-27), the rules are more restrictive to ensure simplicity. Here is a comparison;

| Feature | Old Tax Regime | New Tax Regime (Default) |

| Standard Deduction (30% of Rent) | Available | Available |

| Municipal Taxes Paid | Deductible | Deductible |

| Interest Deduction (u/s 24b) | Available (No Limit) | Available (No Limit) |

| Set-off Loss against Salary? | Yes (Up to ₹2 Lakh) | Strictly No |

| Carry Forward of Loss? | Yes (8 Years) | No |

Earlier Provision: Section 24(b) under the Income Tax Act, 1961

New Provision (from FY 2026–27): Section 22 (Home Loan Interest) under the New Income Tax Act, 2025

B) Deductions Available Only Under Old Tax Regime Only

Starting April 1, 2026, the section “names” (the numbers) are changing completely because the Income Tax Act, 1961 has been officially replaced by the Income Tax Act, 2025. While the benefits (like the ₹1.5 Lakh limit for 80C) are being carried forward to ensure continuity, they have been assigned entirely new section numbers in the new law.

Here is how some of your familiar “household names” have moved and their respective tax benefits:

| Legacy Section (1961 Act) | New Section (2025 Act) | Description | 2026 Limit / Change |

| Section 80C | Section 123 | Investments (PPF, ELSS, Life Insurance) | Limit remains ₹1.5 Lakh. Only available in Old Regime. |

| Section 80D | Section 126 | Health Insurance Premiums | Limit: ₹25,000 (Self) / ₹50,000 (Seniors). |

| Section 87A | Section 156 | Tax Rebate | New Regime: Up to ₹60,000 (for income up to ₹12L). Old Regime: Up to ₹12,500 (for income up to ₹5L). |

| Section 24(b) | Section 22(1)(b) | Home Loan Interest | ₹2 Lakh limit. Self Occupied or Let-out Property |

| Section 80G | Section 133 | Charitable Donations | Digital receipts are now mandatory for all claims. |

| Section 80DD | Section 127 | Disabled Dependent Maintenance | ₹75,000 (Std) / ₹1.25 Lakh (Severe Disability). |

| Section 80E | Section 129 | Education Loan Interest | Entire interest amount is deductible (Old Regime only). |

| Section 80TTA | Section 153(1) | Savings Interest (Non-Seniors) | Increased to ₹50,000 (from ₹10,000) for Old Regime. |

| Section 80TTB | Section 153(2) | Savings Interest (Seniors) | Increased to ₹1,00,000 (from ₹50,000) for Old Regime. |

| Section 10(13A) | Section 11(13) | House Rent Allowance (HRA) | 50% limit extended to 8 cities (incl. Bengaluru, Pune, etc.). |

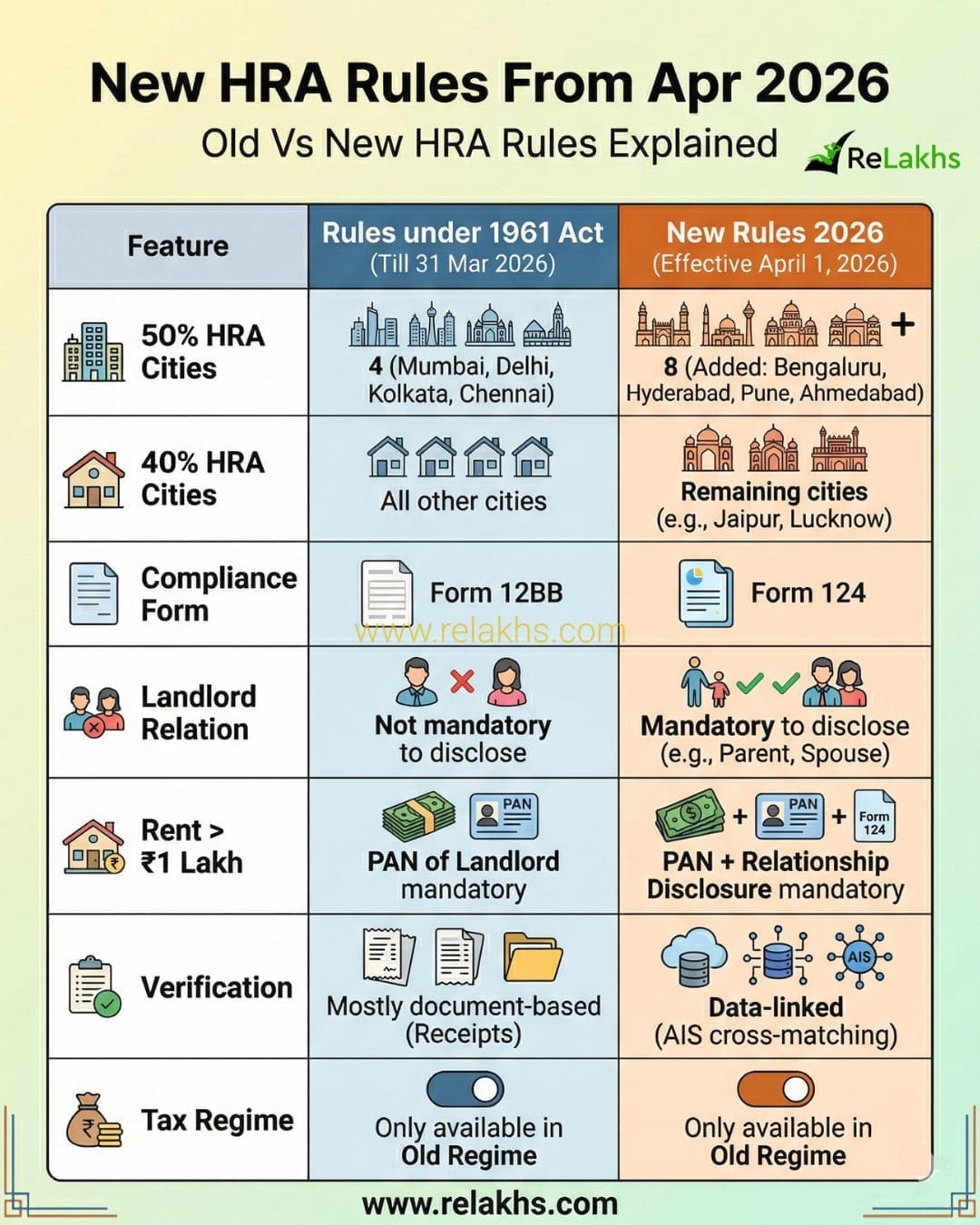

Two major updates under the Old Tax Regime include changes to House Rent Allowance (HRA) and enhanced allowances available for salaried individuals.

House Rent Allowance (HRA) & New 2026 Rules

HRA remains a major benefit for those living in rented accommodation.

- Update: Effective April 2026, the 50% salary exemption now applies to 8 cities: Mumbai, Delhi, Kolkata, Chennai, Bengaluru, Pune, Hyderabad, and Ahmedabad.

- Compliance: If your annual rent exceeds ₹1 Lakh, you must now disclose your relationship with the landlord (to curb “sham” transactions with relatives).

Enhanced Allowances

The 2026 rules have significantly increased the limits for these long-stagnant exemptions (available under Old Tax Regime only):

- Children’s Education Allowance: Hiked from ₹100/month to ₹3,000/month per child.

- Hostel Expenditure Allowance: Increased from ₹300/month to ₹9,000/month per child.

- Meal Vouchers: Tax-free limit on corporate meal cards or coupons raised from ₹50 to ₹200 per meal.

- Corporate Gifts: Tax-free threshold for gift cards or vouchers now ₹15,000 per year.

- Home-to-Office Commute: Daily commute provided or reimbursed by the employer will no longer be taxed as a perquisite.

- Medical Loans: Interest-free or concessional loans provided by employers for medical treatment are now tax-exempt up to ₹2 Lakh (previously ₹20,000).

A word of advice:

Choosing between the old and new tax regime is no longer straightforward. It’s not about which regime is better — it’s about which works better for YOU.

It depends on your income, investments, expenses, and financial goals. A one-size-fits-all approach simply doesn’t work anymore. Before making your choice, take a few minutes to evaluate your deductions or consult a tax expert if needed. The right decision can help you save thousands in taxes every year.

Which tax regime are you planning to choose for Tax Year (FY) 2026-27 — old or new? Let me know in the comments!

Continue reading:

- New Income Tax Forms 2026: New Form Numbers Explained (Form 16, 26AS – Replaced)

- Income Tax Slab Rates 2026-27 (Tax Year) | Budget 2026

- New PAN Rules from April 2026: Limits & Impact

- New Income Tax Rules 2026 | 10 Key Changes Explained

- Latest TDS Rates Tax Year 2026-27 – Complete Chart

(Post first published on : 26-March-2026)

Join our channels