One of the biggest changes introduced under the EPF Scheme, 2026 is the concept of mandatory and voluntary EPF contributions.

Many employees are asking:

- Is EPF now capped at ₹1,800 per month?

- Can I still contribute on my full Basic Salary?

- Is this the same as VPF?

- Will my employer continue contributing above ₹1,800?

Unfortunately, there is considerable confusion because the new scheme uses the term “voluntary contribution”, while employees have traditionally been familiar with Voluntary Provident Fund (VPF). Although these terms sound similar, they are not the same. Let’s understand the new rules in simple language.

What Has Changed Under EPF Scheme 2026?

Earlier, many employers calculated EPF contributions at 12% of the employee’s actual Basic Salary (plus Dearness Allowance, wherever applicable), even if the salary exceeded the statutory wage ceiling of ₹15,000.

For example, if an employee’s Basic Salary was ₹50,000:

- Employee EPF = 12% × ₹50,000 = ₹6,000

- Employer EPF = 12% × ₹50,000 = ₹6,000 (subject to the applicable EPS allocation)

This practice continued because both the employer and the employee had agreed to contribute EPF on higher wages.

Under the EPF Scheme, 2026, the law now expressly distinguishes between:

- Mandatory EPF contribution (up to the statutory wage ceiling), and

- Voluntary EPF contribution on higher wages (beyond the statutory wage ceiling).

This is one of the most significant structural clarifications introduced under the new Scheme. It clearly separates the statutory minimum contribution from higher-wage contributions made by mutual agreement.

Mandatory EPF Contribution

The mandatory EPF contribution is still tied to the statutory wage ceiling—it has not changed to your full Basic Salary.

Current statutory wage ceiling: ₹15,000

So, the compulsory EPF looks like this:

- Employee contribution: 12% × ₹15,000 = ₹1,800

- Employer contribution: 12% × ₹15,000 = ₹1,800 (with the usual EPS allocation applied as per rules)

This ₹1,800 from you and ₹1,800 from your employer is the mandatory portion that must be contributed under the EPF Scheme, 2026. The confusion usually arises when people mix this compulsory part with any extra, higher-wage contributions that are allowed by agreement.

What is “Voluntary EPF on Higher Wages”?

If your Basic Salary is ₹50,000, you and your employer can still choose to contribute EPF on the full amount—not just on ₹15,000.

For example:

- Basic Salary = ₹50,000

- Employee EPF = 12% × ₹50,000 = ₹6,000

- Employer EPF = 12% × ₹50,000 = ₹6,000 (subject to the applicable EPS allocation)

Under the EPF Scheme, 2026, anything above the mandatory ₹1,800 (12% of ₹15,000) is now clearly treated as a voluntary contribution, because it is calculated on wages higher than the statutory ceiling.

This doesn’t introduce a brand-new benefit. Instead, the new Scheme simply gives formal legal recognition to a practice many organisations were already following—contributing on higher wages by mutual agreement—while separating it cleanly from the compulsory minimum.

Is Employer Required to Match Above ₹1,800?

No – your employer is not automatically locked into contributing only ₹1,800 per month.

Under the EPF Scheme, 2026, the employer is legally obliged to contribute only up to the statutory wage ceiling of ₹15,000. That means:

- Mandatory employer EPF = 12% × ₹15,000 = ₹1,800

Anything above this, i.e., contributions on wages exceeding ₹15,000, is now clearly treated as voluntary and is based on mutual agreement between you and your employer.

In practice, this means your employer has three broad options:

- It may choose to continue contributing on your higher actual wages (like before).

- It may revise its PF policy and partially or fully reduce contributions above the ceiling.

- It may decide to restrict future contributions strictly to the statutory limit of ₹15,000.

Because of this flexibility, it becomes crucial for employees to understand their organisation’s PF policy—whether the company intends to maintain higher-wage contributions, cap them, or change them over time.

Is This the Same as VPF (Voluntary Provident Fund)?

This is not the same as VPF—and that’s exactly where most of the confusion comes from.

Voluntary EPF on higher wages

This happens when both you and your employer agree to contribute EPF on wages above ₹15,000.

- Example:

- Basic Salary = ₹50,000

- Employee EPF = ₹6,000

- Employer EPF = ₹6,000

Here, EPF is being calculated on the full ₹50,000, not just on the statutory ceiling of ₹15,000. Both sides are contributing on the higher wage, so this “extra” portion is treated as a voluntary EPF contribution on higher wages.

Voluntary Provident Fund (VPF)

VPF is different. It is an extra, optional amount that only the employee chooses to contribute. The employer does not match this additional VPF.

- Example:

- Employee EPF = ₹6,000

- Additional VPF = ₹10,000 (subject to maximum of Basic + DA)

- Total employee contribution = ₹16,000

- Employer contribution = ₹6,000

In this case, the extra ₹10,000 is VPF—purely your own voluntary top-up. The employer’s share stays limited to its regular EPF contribution.

In short:

- Voluntary EPF on higher wages = both employer and employee contribute on salary above ₹15,000.

- VPF = only the employee adds extra money; the employer does not match it.

Mandatory EPF vs Voluntary Higher EPF vs VPF

| Feature | Mandatory EPF | Voluntary EPF on Higher Wages | Voluntary Provident Fund (VPF) |

|---|---|---|---|

| Contribution Basis | 12% of statutory wage ceiling (₹15,000) | EPF calculated on wages above ₹15,000 by mutual agreement | Additional employee contribution over and above EPF |

| Employee Contribution | Mandatory | Voluntary | Voluntary |

| Employer Contribution | Mandatory | Only if employer agrees | No employer contribution |

| Employer Matching | Yes | Only if employer participates | No |

| Purpose | Statutory compliance | Continue higher PF contributions | Increase retirement savings |

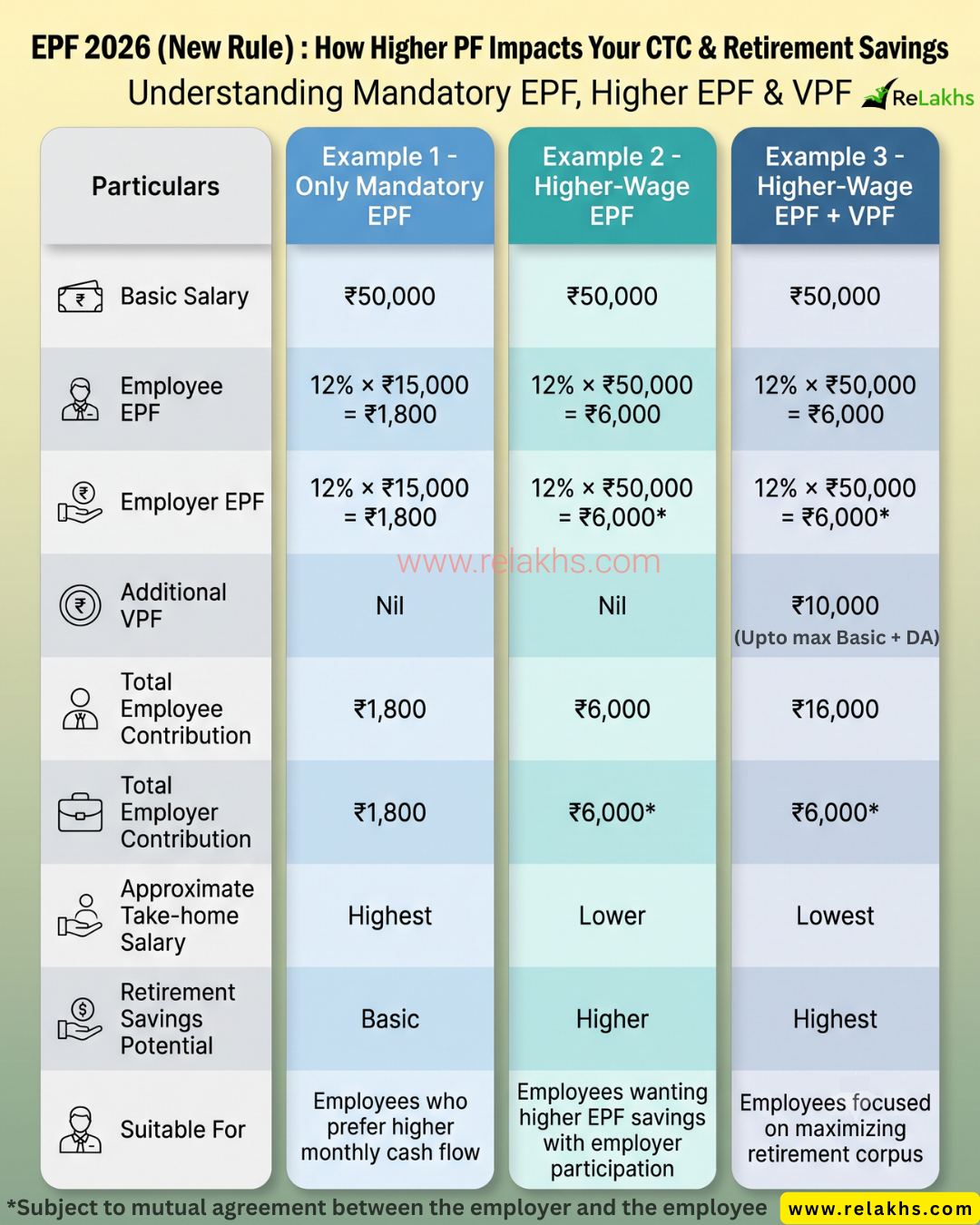

Examples: How Mandatory EPF, Higher-Wage EPF & VPF Work

Assume the employee’s Basic Salary is ₹50,000.

| Particulars | Example 1 – Only Mandatory EPF | Example 2 – Higher-Wage EPF | Example 3 – Higher-Wage EPF + VPF |

|---|---|---|---|

| Basic Salary | ₹50,000 | ₹50,000 | ₹50,000 |

| Employee EPF | 12% × ₹15,000 = ₹1,800 | 12% × ₹50,000 = ₹6,000 | 12% × ₹50,000 = ₹6,000 |

| Employer EPF | 12% × ₹15,000 = ₹1,800 | 12% × ₹50,000 = ₹6,000* | 12% × ₹50,000 = ₹6,000* |

| Additional VPF | Nil | Nil | ₹10,000 |

| Total Employee Contribution | ₹1,800 | ₹6,000 | ₹16,000 |

| Total Employer Contribution | ₹1,800 | ₹6,000* | ₹6,000* |

| Approximate Take-home Salary | Highest | Lower | Lowest |

| Retirement Savings Potential | Basic | Higher | Highest |

| Suitable For | Employees who prefer higher monthly cash flow | Employees wanting higher EPF savings with employer participation | Employees focused on maximizing retirement corpus |

*Assumes the employer has agreed to contribute EPF on wages exceeding the statutory wage ceiling. Under the EPF Scheme, 2026, contributions above the statutory wage ceiling are voluntary and depend on the employer’s policy or mutual agreement.

Key Takeaway

The EPF Scheme, 2026 recognizes two different voluntary contribution mechanisms, and they should not be confused.

- Voluntary EPF on Higher Wages involves contributions by both the employer and employee on wages exceeding the statutory wage ceiling, if they mutually agree.

- Voluntary Provident Fund (VPF) is an additional contribution made solely by the employee, with no corresponding employer contribution.

Understanding this distinction will help you correctly interpret your salary structure, EPF deductions, employer contribution, and retirement savings under the new EPF framework.

Frequently Asked Questions (FAQs)

Is EPF now limited to ₹1,800 per month? No. ₹1,800 is the mandatory minimum contribution based on the current statutory wage ceiling of ₹15,000. Higher contributions may continue if the employer and employee mutually agree.

Can my employer stop contributing on my full Basic Salary? The 2026 Scheme clarifies that contributions above the statutory wage ceiling are voluntary. Whether an employer continues higher-wage contributions depends on its policy, applicable agreements, and legal obligations.

Is higher EPF the same as VPF? No. Higher-wage EPF involves contributions based on wages above ₹15,000 and may include both employer and employee. VPF is an additional contribution made only by the employee.

Does VPF continue under the EPF Scheme, 2026? Yes. The VPF facility continues, allowing employees to voluntarily contribute additional amounts (up to the permitted limit), without any matching contribution from the employer.

My View

The EPF Scheme, 2026 has not introduced a new investment option. Instead, it has brought greater clarity by explicitly distinguishing between the mandatory statutory contribution and voluntary contributions on higher wages. The long-standing VPF facility also continues as a separate avenue for employees who wish to save more for retirement.

The challenge is that the word “voluntary” is now used in two different contexts. Once you understand the distinction, the new framework becomes much easier to follow.

Continue reading:

- EPF Tax Rules 2026 – Complete Guide to EPF Withdrawal, Interest & Income Tax

- Best Pension Schemes in India (2026)

- India’s 35-Year Journey of 1-Year Bank FD Interest Rates (1990–2026)

- New EPF Withdrawal Rules 2026 | Big Relief, Bigger Responsibility for 30 Crore Subscribers

(Post first published on : 07-July-2026)

Join our channels