A lot of salaried individuals assume their EPF money is always tax-free the moment it lands in their account. That’s not entirely true!

Whether your EPF withdrawal gets taxed—or how much of it does—depends on a mix of factors, like:

- How many years you’ve been in continuous service

- Why you’re withdrawing the money in the first place

- Whether it’s a full withdrawal or just a partial one

- The actual amount you’re pulling out

- Whether you’ve submitted your PAN or not

- Whether your own EPF contribution crosses ₹2.5 lakh in a year

- The interest your EPF balance has earned over time

In this guide, we’ll break down every major EPF tax rule that applies in 2026, with simple examples to make it easy to follow

Is EPF Always Tax-Free?

Is EPF always tax-free? Nope—that’s a common myth.

While EPF does come with some solid tax benefits, not every withdrawal automatically qualifies for exemption. Whether tax applies (and how much) comes down to a few things:

- How long you’ve been in service

- Whether it’s a full or partial withdrawal

- The actual reason behind the withdrawal

- How much you’ve contributed

- What the relevant provisions of the Income-tax Act say

So before you go ahead and withdraw your EPF balance, it’s worth understanding these rules first—it could save you from an unexpected tax bill.

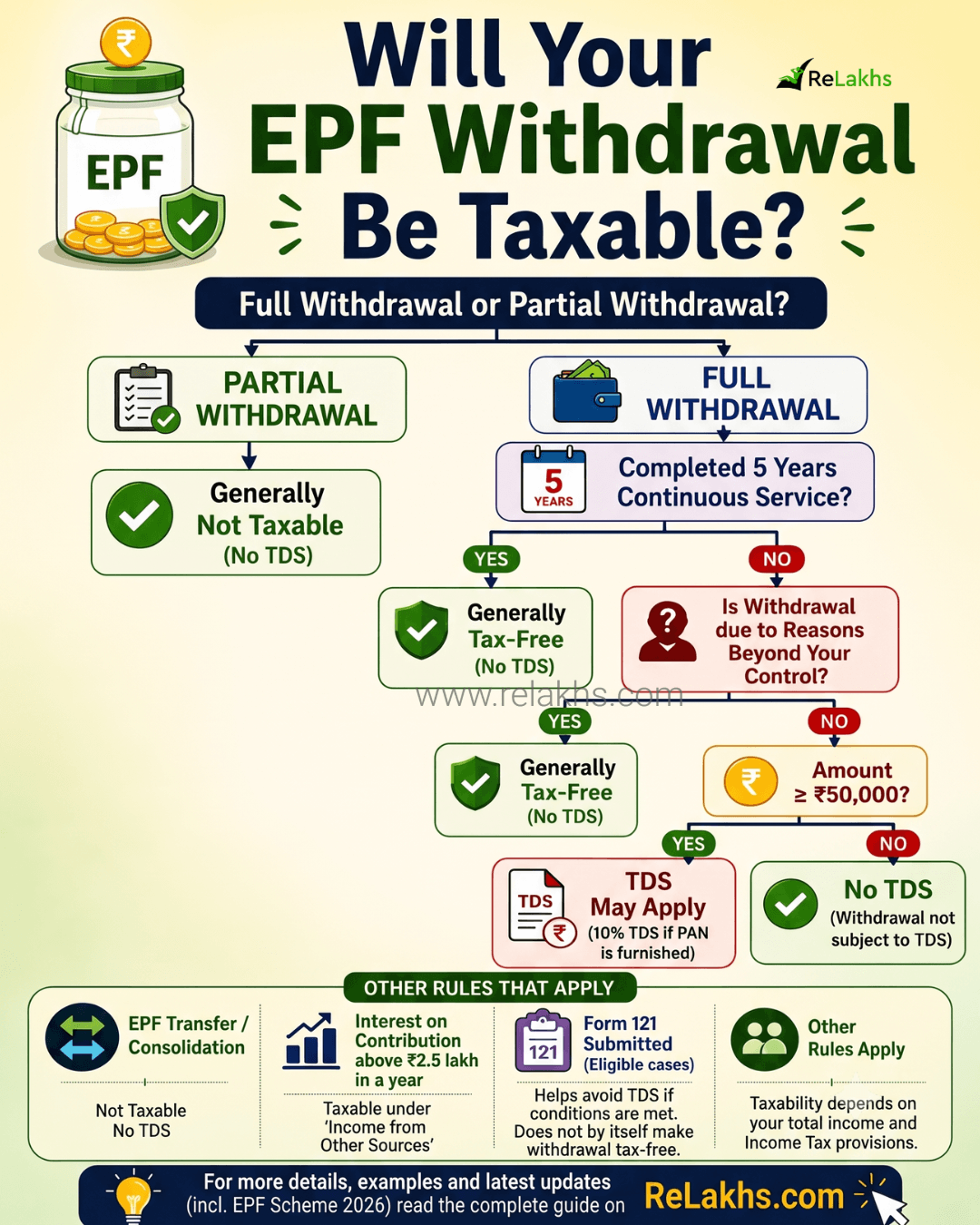

Tax on Complete EPF Withdrawal after Completing 5 Years of Continuous Service

This is the easiest scenario to understand. If you’ve completed five years or more of continuous service, your entire EPF withdrawal is generally exempt from income tax, and no TDS is deducted either. This exemption covers your own contribution, your employer’s contribution, and the interest earned on both.

For example, Rahul worked with Employer A for 2 years and then moved to Employer B, where he worked for another 4 years. Since he transferred his EPF account instead of withdrawing it when he switched jobs, his service is treated as continuous, adding up to a total of 6 years. Because this crosses the 5-year mark, his entire EPF withdrawal is generally tax-free.

The key thing to keep in mind here is that a transfer is not the same as a withdrawal. Moving your EPF balance around—whether between accounts, employers, or even into NPS where allowed—doesn’t count as taking the money out, so it stays outside the scope of tax.

But here’s the catch: this benefit only holds if you transfer your EPF account. If you choose to withdraw your EPF balance instead of transferring it when changing jobs, the continuity breaks right there, and your years of service start counting afresh from your next employer.

Tax on Complete EPF Withdrawal before Completing 5 Years

This is where most confusion arises. Whether TDS gets deducted on your EPF withdrawal depends mainly on two things: the amount you’re withdrawing and whether you’ve submitted your PAN.

| Withdrawal amount | PAN available | TDS |

|---|---|---|

| Below ₹50,000 | Yes/No | No TDS |

| ₹50,000 or more | Yes | TDS applicable |

| ₹50,000 or more | No | Higher TDS may apply as per the Income-tax Act |

If your estimated tax liability for the year is nil, you don’t have to just sit and let TDS get deducted—you can submit Form 121 to request that no TDS be cut, as long as you meet the prescribed conditions. This form has replaced the earlier Forms 15G and 15H starting FY 2026-27, so if you were familiar with those, Form 121 is essentially their updated version.

That said, it’s important not to misread what this form actually does. Form 121 only helps you avoid TDS at the time of withdrawal—it doesn’t make a taxable EPF withdrawal tax-free. So even if TDS isn’t deducted because of this form, you still need to check whether the withdrawal is taxable under the usual rules and report it accordingly when filing your return.

No TDS does NOT automatically mean the withdrawal is tax-free. Deduction of TDS does NOT mean that the final tax has already been paid.

Cases Where EPF Withdrawal is Generally Not Taxable Even Before Completing Five Years

There are certain exceptions where the usual 5-year rule doesn’t apply so strictly. These situations mostly cover cases where your employment ends for reasons that were beyond your (employee’s) control, such as:

- Closure of the employer’s business

- Business discontinuance

- Retrenchment

- Permanent disability

- Other prescribed circumstances

In these cases, you may still get tax relief on your EPF withdrawal even if you haven’t completed the full five years of service, subject to the conditions laid out under the Income-tax Act. So if you lost your job due to no fault of your own, it’s worth checking whether your situation falls under one of these exceptions before assuming your withdrawal will be taxed.

Tax on EPF Partial Withdrawals

The new EPF Scheme has significantly restructured and simplified the partial withdrawal provisions. EPF partial withdrawals (also known as EPF advances) permitted under the EPF Scheme, 2026 are generally not taxable, provided they are made in accordance with the prescribed conditions under the Scheme.

Eligible members can generally apply for EPF advances for purposes such as:

- Medical treatment

- Higher education

- Marriage

- Purchase of a plot or house

- Construction of a house

- Home loan repayment

- House renovation or alteration

- Disability-related requirements

- Natural calamities

- Other notified special circumstances

Since these withdrawals are specifically permitted under the EPF Scheme, they generally do not attract income tax.

Important: Although EPF advances are generally tax-free, withdrawing your retirement savings prematurely reduces the power of long-term compounding. Therefore, consider using EPF advances only for genuine financial needs rather than discretionary expenses.

Tax on Interest if Employee Contribution Exceeds ₹2.5 lakh in a Financial Year

This particular rule was brought in to stop people from parking excessively large amounts into EPF and enjoying tax-free interest on all of it forever.

Here’s how it works: if your own annual EPF contribution goes beyond ₹2.5 lakh in a financial year, the interest earned on that excess amount becomes taxable. Only the interest tied to the extra contribution gets taxed—your principal contribution itself stays completely unaffected. This taxable interest is charged under the head “Income from Other Sources” when you file your return.

For example, if your total employee contribution in a year is ₹3,20,000, then ₹2,50,000 of it remains exempt as usual, while the remaining ₹70,000 is treated as the “excess” contribution. It’s only the interest earned specifically on this ₹70,000 that becomes taxable—not the ₹70,000 itself, and definitely not your entire EPF balance.

Interest Earned on In-operative account

The EPFO continues to credit interest to all active and inactive accounts up to the age of 58, and even if no new contributions are made, it keeps earning interest until the member explicitly decides to withdraw the corpus or passes away. Inoperative accounts do not lose out on interest accumulation anymore; they simply sit waiting for a claim settlement.

However, there is a significant tax catch if you leave employment: the interest accrued from the date of your unemployment (whether due to resignation, termination, or retirement) till the date you actually withdraw the corpus is treated as taxable income under ‘Income from Other Sources’

Any interest that accrues in your EPF account after you resign or retire is not earned in the capacity of an “employee”. Therefore, it is fully taxable under “Income from Other Sources” in the financial year it accrues.

EPF Tax Rules – Summary

| Scenario | Income Tax Applicability | TDS |

| Withdrawal after 5 years | Generally Exempt | No |

| Withdrawal before 5 years (Below ₹50,000) | May be taxable (based on income slabs) | No |

| Withdrawal before 5 years (₹50,000 or more) | May be taxable (based on income slabs) | Applicable (10% with PAN) |

| Withdrawal before 5 years due to reasons beyond control (e.g., ill-health, business closure, retrenchment) | Generally Exempt (Subject to verification of the cause) | No |

| Form 121 submitted (Eligible cases) | Exempt only if final annual income remains below tax bracket | No TDS will be deducted |

| Partial withdrawal | Generally not taxable (for specified medical/housing/marriage uses) | No |

| EPF transfer | Not taxable | No |

| Interest on contribution above ₹2.5 lakh | Taxable under “Income from Other Sources” | Applicable (10% if interest exceeds ₹5,000/year) |

| Transfer to NPS (Eligible cases) | Generally not taxable | No |

Frequently Asked Questions

Is EPF taxable under the New Tax Regime? – The taxability of EPF withdrawals depends on the relevant provisions of the Income-tax Act and not merely on whether you opt for the old or new tax regime.

Does changing jobs reset the five-year period? – No. If you transfer your EPF account, the previous period of continuous service is generally counted.

Can Form 121 make my EPF withdrawal tax-free? – No. It can only help avoid TDS, subject to eligibility conditions.

Is TDS my final tax? – No. Your final tax liability is determined while filing your Income-tax Return.

Is every EPF partial withdrawal tax-free? – Eligible partial withdrawals under the EPF Scheme are generally not taxable.

Final Words

EPF continues to be one of the most tax-efficient retirement savings instruments available to salaried employees. However, many taxpayers end up paying unnecessary tax—or assuming they owe none—because they misunderstand the rules around withdrawals, TDS, continuous service, and interest taxation.

Before withdrawing your EPF balance, take a few minutes to evaluate your years of continuous service, the reason for withdrawal, the amount involved, and the applicable income-tax provisions. A little planning can help you avoid unexpected tax consequences and preserve more of your retirement savings.

Continue reading:

- EPF Scheme 2026: Mandatory ₹1,800 EPF, Voluntary Higher EPF & VPF Explained (With Examples)

- New EPF Withdrawal Rules 2025-26

- Best Pension Schemes in India (2026) – EPS, NPS, APY Explained

(Post first published on : 13-July-2026)

Join our channels