The Union Budget 2026–27, presented by Finance Minister Nirmala Sitharaman on 1 Feb 2026, has introduced a significant change in how capital gains on Sovereign Gold Bonds (SGBs) are taxed — especially on redemption at maturity.

What Are Sovereign Gold Bonds?

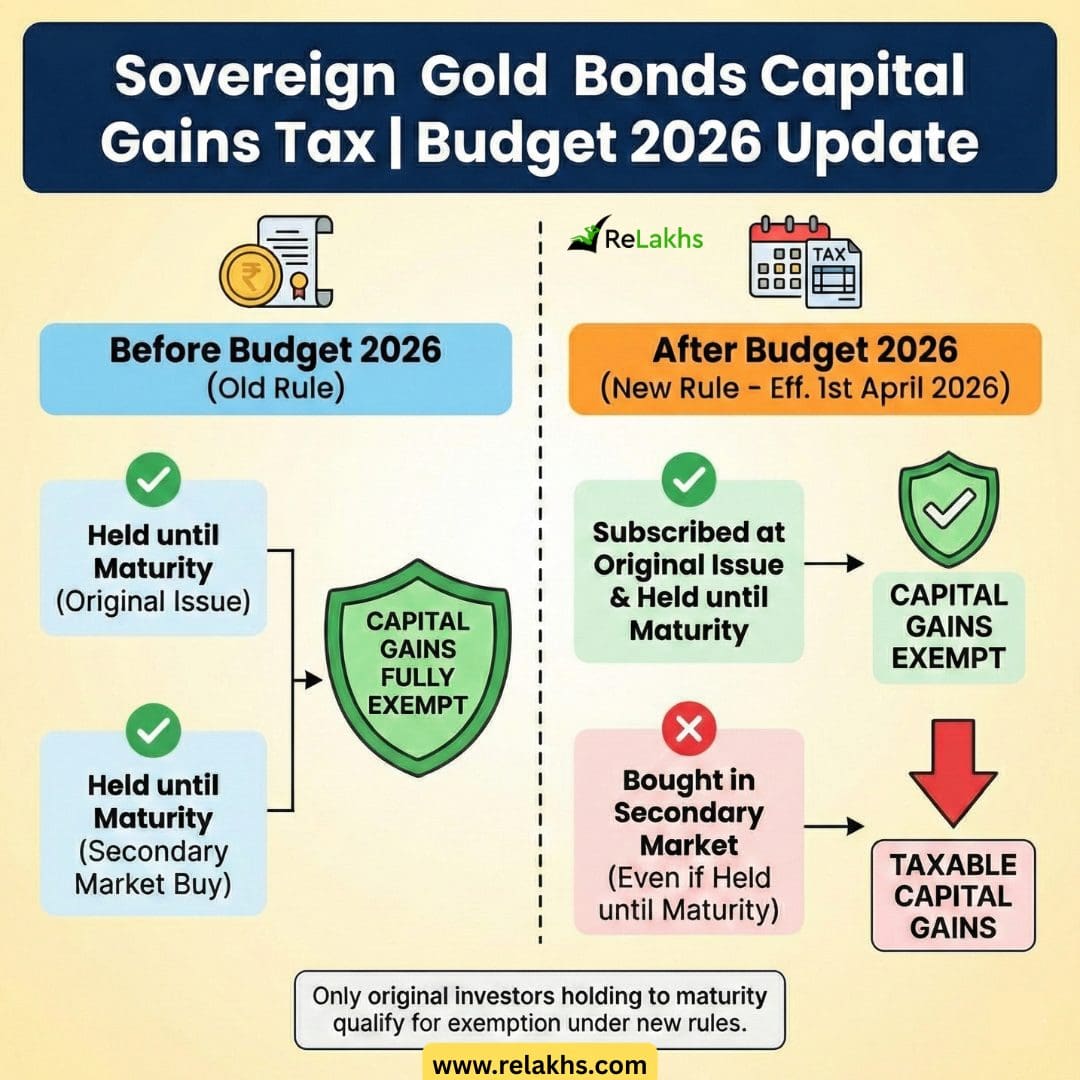

Sovereign Gold Bonds are government-backed debt instruments linked to gold prices. Investors buy them from the Reserve Bank of India (RBI), earn 2.5 % annual interest, and upon maturity (usually 8 years), redeem the bond at the prevailing price of gold. Historically, capital gains at maturity have been completely tax-free, making SGBs a popular and tax-efficient way to invest in gold.

Sovereign Gold Bonds Capital Gains Tax | Budget 2026

Before Budget 2026, the rule was straightforward: If you held the SGB until maturity — even if bought on the secondary market — your capital gains at redemption were fully exempt from tax.

However, Budget 2026 has come up with a new tax rule effective from 1st April 2026;

From the upcoming tax year 2026-27:

- Capital gains at maturity will be tax-exempt ONLY if:

- You have subscribed to the Sovereign Gold Bond at the time of the original issue (primary issuance by RBI), and

- You held the bond continuously until redemption at maturity.

- If you bought the SGB in the secondary market, even if you hold it until maturity, your gains on redemption will no longer be exempt — they will be treated as taxable capital gains.

- This means that if you buy an SGB later from someone else (for instance, from the stock market) and then redeem it at maturity, you might not qualify for the capital gains tax exemption. Only original investors who hold the bond until maturity will receive the tax benefit.

This amendment clarifies the tax exemption’s intended scope under Section 70(1)(x) of the Income-tax Act: that the benefit is meant to encourage long-term investing in SGBs by original subscribers.

Based on the Finance Bill wording:

“These amendments shall take effect from 1st April 2026 and shall apply in relation to the tax year 2026-27 and subsequent tax years.”

Since the amendment is effective from 1 April 2026 and applies prospectively, SGBs bought before 31 March 2026 should be grandfathered. Any further clarification, if required, may come via CBDT circulars.

SGB Secondary Market | Applicability of Capital Gains Tax

If you acquired the SGB in the market – Going forward, you will NOT get the capital-gains exemption at maturity.

Your gains (if any) on redemption will be taxed like other capital assets:

- If sold before maturity:

• Less than 12 months — short-term gains will be taxed at slab rate.

• More than 12 months — long-term gains will be taxed at 12.5 % (no indexation). - If held until maturity and eligible under new rules:

• Secondary market SGB buyers will pay 12.5% LTCG tax on long-term gains even if bonds are redeemed at maturity.

What are the reasons for this change?

The government’s objective with this tax tweak is to:

- Curb tax arbitrage — Previously, some investors bought SGBs on the secondary market at a discount solely to benefit from tax-free redemption.

- Align the exemption with its original purpose — Reward genuine long-term participation via primary subscription instead of trading.

Continue reading:

- Gold vs Silver vs Copper: Should You Invest in Silver Now?

- How much Gold can Indian Families legally hold at Home?

- Income Tax Slab Rates 2026-27 (Tax Year) | Budget 2026

(Post first published on : 01-Feb-2026)

Join our channels