Union Finance Minister Smt Nirmala Sitharaman on February 1st 2025 announced her eighth consecutive Union Budget 2025 in the Lok Sabha. Below are the latest personal finance related proposals that have been made in Budget 2025-26 ;

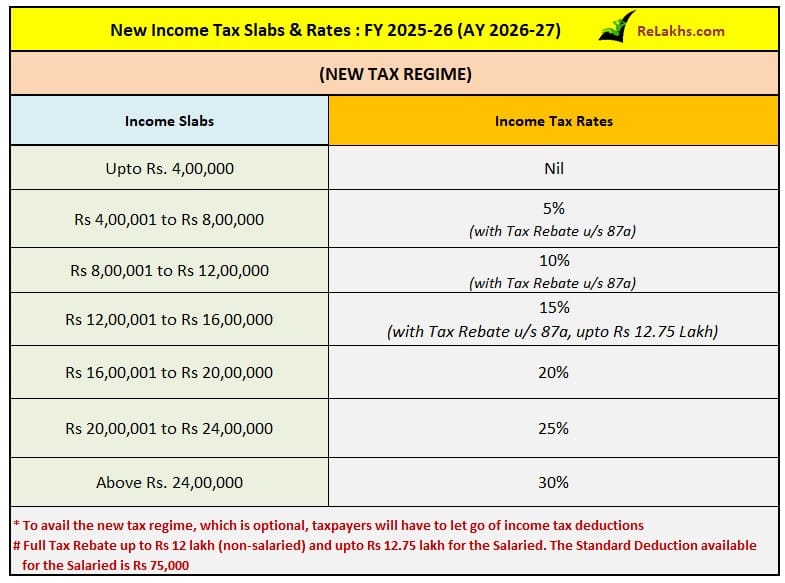

1) Revised Income Tax Slab Rates for FY 2025-26

- Under the new tax regime, the basic exemption limit has been increased from Rs 3 lakh to Rs 4 lakh.

- As per the Budget 2025, no income tax will be payable on income up to Rs 12 lakh has been proposed.

- The salaried individuals eligible for the standard deduction benefit of Rs 75,000 will not be required to pay any taxes if their gross taxable income does not exceed Rs 12.75 lakh.

- If your income exceeds Rs 12 lakh then you need to pay tax at applicable slab rates.

Related article : 90% of Tax payers will now have Zero Tax Liability? (Budget 2025)

2) Revised Section 87A Tax Rebate FY 2025-26 / AY 2026-27

- The limit for claiming the tax rebate is increased from the existing Rs 7 lakh to Rs 12 lakh for income under Section 115BAC. The maximum rebate will rise from Rs 25,000 to Rs 60,000.

- Kindly note that this rebate will not apply to special grade incomes such as capital gains.

- If your normal income other than special rate income (such as capital gains) is up to Rs 12 lakh, a tax rebate is being provided in addition to the benefit due to slab rate reduction in such a manner that there is no tax payable by you.

- In simpler terms, if you’re a regular salaried individual or earn other kinds of “normal income” up to Rs 12 lakh, you won’t have to pay any tax, thanks to both the tax rebate and the reduced income tax slabs. However, if you earn income from sources like capital gains, that income won’t benefit from the rebate, and it will be taxed separately under different rules.

Normal Income or regular income refers to your salary, wages, rental income or business profits. Where as Special Rate income refers to capital gains, where applicable tax rates are different. So, LTCG & STCG from Equity or other special rates assets are not tax free within this Rs 12 lakh.

Related article : What is the difference between Normal Income and Special Rate Income?

3) Revised TDS limit for Senior Citizens

The limit for tax deduction at source on interest income for senior citizens is being doubled from the present Rs 50,000 to Rs 1 lakh.

4) Revised TDS limit on Rent

The annual limit of Rs 2.40 lakh for TDS on rent is increased to Rs 6 lakh.

5) Revised time limit to update ITRs

- Budget 2025 has proposed to extend the time limit for filing updated income tax returns from the existing 24 months to 48 months.

- While Budget 2025 has extended the time limit for filing updated ITR, the penal tax payable on the additional income declared in the ITR has been pegged at 60% and 70% for updated ITRs filed in the 3rd and 4th year from the end of the respective assessment year.

6) Benefit of two Self-Occupied Properties

Presently income tax assessees ca claim the annual value of self-occupied properties as nil only on the fulfilment of certain conditions. Considering the difficulties faced by taxpayers, it is proposed to allow the benefit of two such self-occupied properties without any condition.

7) TCS changes for remittances under LRS

The threshold to collect tax at source (TCS) on remittances under RBI’s Liberalized Remittance Scheme (LRS) is proposed to be increased from Rs 7 lakh to Rs 10 lakh. The FM also proposed to remove TCS on remittances for education purposes, where such remittance is out of a loan taken from a specified financial institution.

8) Tax free withdrawals from NSS

Withdrawals from old NSS accounts (National Savings Scheme) will be entirely tax-free if the funds are withdrawn on or after August 29, 2024. There will be no tax liability on withdrawals from these accounts.

9) NPS Vatsalya Account

It is proposed to extend the tax benefits available to the National Pension Scheme (NPS) under Section 80CCD of the Act to the contributions made to the NPS Vatsalya accounts as well. No additional benefit is applicable for deposits in NPS vatsalya account.

10) Taxation on ULIPs

- The taxation of ULIPs (Unit Linked Insurance Plans) has been rationalised to provide that all ULIPs which are not exempt under section 10(10D) will be taxable as capital gains similar to equity oriented funds. Currently only those ULIPs which are purchased after 01 Feb 2021 with premium/ aggregage premiums more than INR 2.5 lakhs p.a. are taxable as capital gains.

- Post the amendment, a ULIP purchased say in 2005 for which the premium payable in any year exceeds 10% of the actual sum assured, will also be taxable as capital gain instead of being taxed as income from other sources. The ULIPs which were exempt previously will continue to remain so.

Kindly note that this article will be updated/edited as and when more information is available.

(Post first published on : 01-February-2025)

Join our channels