The 2025 Union Budget brought relief for many taxpayers since incomes up to Rs 12 lakh will not be taxed, but many individuals are struggling to understand how it actually works.

The primary reason for all the confusion is the below statement made by the union FM minister in her budget speech;

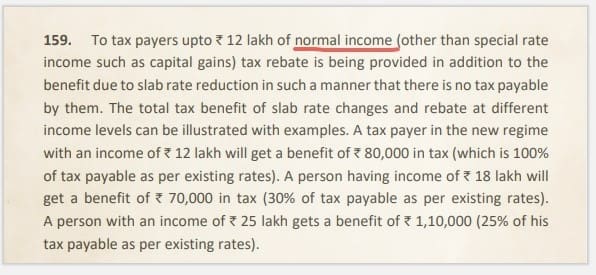

“Tax payers upto Rs 12 lakh of normal income (other than special rate income such as capital gains) tax rebate is being provided in addition to the benefit due to slab rate reduction in such a manner that there is no tax payable by them…”

So, what is meant by Normal income? What is the difference between Normal income and Special rate income?

Normal Income Vs Special Rate Income

Normal Income refers to your regular incomes like Salary, business profits, rental income or wages. These incomes are charged at below applicable (revised) slab rates.

As per the new proposal, income up to Rs 12 lakh has no tax liability. What if you have say Rs 7 lakh as salary income and Rs 5 lakh as Short Term Capital Gains arising out of your stock trading? Does this Rs 5 lakh is also eligible for tax rebate?

The answer is NO!

The Capital Gains are considered as Special rate incomes and are taxed at different rates. The Tax rebate is not applicable on these incomes. So, the tax relief is applicable only on your Rs 7 lakh salary income and tax rate @ 15% is applicable on STCG of Rs 5 lakh. Another example for special rate income is ‘income from lotteries’.

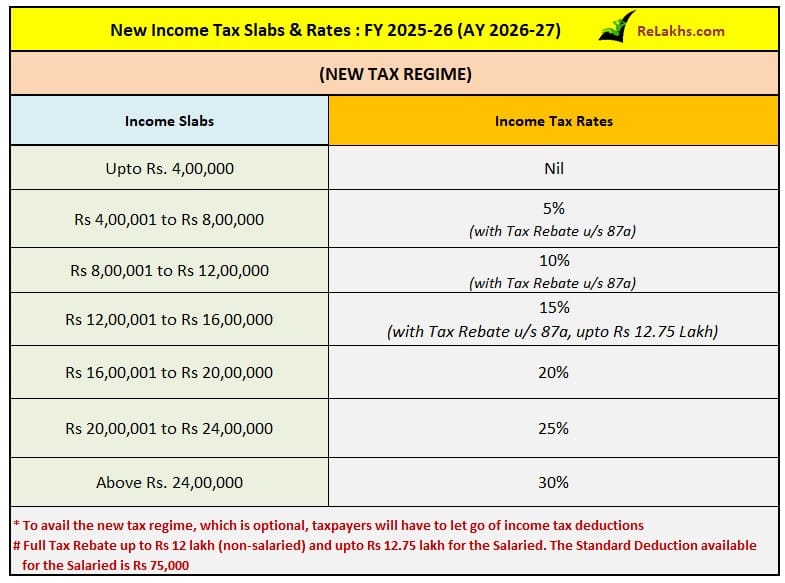

So, the Finance Minister has revised the basic exemption limit to Rs 4 lakh and those earning between Rs 4 lakh and Rs 12 lakh will pay taxes at a reduced rate (5% & 10% depending on income), which, combined with the tax rebate, leads to zero tax. But, these earnings should be the standard incomes and not special rate ones. The relief measures strictly apply to standard income taxed under Section 115BAC. (Reduced rate is also referred as slab rate reduction.)

Income chargeable u/s 115BBE like unexplained cash credits, investments, money, bullion, jewelry, or other valuable articles is also considered as special income.

Kindly note that this article will be updated/edited as and when more information is available.

(Post first published on : 01-February-2025)

Join our channels

Easy to understand the difference between normal income and special rate incomes.

Thank you dear for your kind words

Thanks for the detailed analysis of the taxation