Top 15 Best Mutual Funds 2021 & beyond | Top Performing Equity Funds

The year 2020 has been an year of ups and downs for Indian equity markets, much like a roller coaster. After a catastrophic drop in March 2020(due to the covid-19 pandemic), the Indian markets have recovered swiftly and are now trading at their life-time highs.

Sensex graph Jan 2020 to Jan 2021

The last calendar year has been a real-test of character for the so-called long-term and aggressive investors. Many of you might have actually redeemed your equity mutual fund units during Mar to Apr 2020 after a jaw-dropping fall loses (or) atleast would have given it a serious thought to redeem some of your MF units. Am I right??

If you have been investing for a long-term, these kind of market falls can actually be a great chance to make additional investments. You need to have conviction in your investment strategy.

A mere of selection of Best Equity Mutual funds is not enough, you got to stay invested and continue investing in them as per your investment objective. Hence, it is prudent to follow a goal-based approach rather than timing the market and with a proper Asset Allocation.

In this post, let us discuss – What are the Top 15 Best Mutual Funds 2021-22? How to select top & consistent Equity Mutual Fund performers? What are the best large-cap, flexi-cap, mid-cap, tax saving ELSS and Equity Hybrid funds to invest now?…

Top 15 Best Mutual Funds 2021 & beyond

As per my analysis, below is the list of best Equity Mutual Funds to invest in India (now in 2021);

Best Equity Mutual Funds Schemes to invest in 2021 & beyond!

I have considered both, the past performance and risk ratios of mutual funds to shortlist top rated Equity mutual fund schemes.

Below image gives you an idea on the parameters (to know, how consistent the funds have been..?) that one can consider while shortlisting right mutual fund schemes.

How to pick right & best equity mutual fund scheme based on Risk ratios?

Let’s now analyse category-wise best equity funds;

Best Large Cap Mutual Funds 2021-22

Below are the consistent and top performing large cap funds that can be considered to invest now;

UTI Nifty Index Fund

Axis Bluechip Fund

ICICI Pru Bluechip Fund

The above funds were listed even in my last year review as well.

Most of the large-cap funds have not out-performed their benchmark indices in the few years (after the implementation of SEBI’s re-categorization rules).

If you are planning to invest afresh, it is prudent to go for large-cap based index funds than actively managed large-cap Funds.

Considering the past performance, risk-return trade off and cost, advisable to stick / switch to any large-cap based index fund.

Best Flexi-Cap Mutual Funds 2021-22

As per the old guidelines, a Multi-cap Mutual fund scheme or Diversified Equity Scheme can invest a minimum of 65% of total assets across large, mid and small cap stocks. At present, fund managers of multi cap funds can invest across market capitalization as per their choice.

However, SEBI, in a recent circular, has tweaked the Asset allocation rules for multi cap mutual funds. The fund managers have to mandatorily allocate at least 25% each in large-, mid-, small-cap stocks. These new norms havetaken away the flexibility.

Hence, I believe, flexi-cap (new category) can be a better alternative to multi-cap oriented funds. Flexi Cap funds can invest minimum 65% of its assets in equity and equity related instruments with dynamic allocation across large cap, mid cap, and small cap stocks.

You may consider below Flexi-cap funds for your long term financial goals. In case, you have a large-cap fund and also a mid-cap based fund in your portfolio, can give this category a miss.

Parag Parikh Long Term Equity Fund is renamed as Parag Parikh Flexi Cap Fund.

It has 65.74% investment in Indian stocks of which 29.05% is in large cap stocks, 11.69% is in mid cap stocks, 21.92% in small cap stocks. Foreign Equity Holdings are around 28%.

The Financial Services, Technology & Consumer cyclical related stocks have been its favorite picks.

UTI Equity Fund is one of the oldest funds in Indian Mutual Fund industry. I have been keenly following UTI Equity fund from a long time. In fact, this fund was in my best multi-cap fund list earlier.

It has now been moved from muti-cap category to flexi-cap category.

The fund has given returns of around 14% pa in the last 15 years.

The Financial Services, Consumer cyclical & Technology related stocks have been its favorite picks.

Best Equity Mid-cap Mutual Funds to invest in 2021

Below are the top performing equity mid-cap & small-cap oriented funds;

Axis Mid-cap Fund

DSP Mid-cap Fund

SBI Small-cap Fund

The average category returns from mid-cap oriented funds have been around 14% in the last 10 years. We currently have around 27 mid-cap funds.

The key parameter to look in mid-cap funds is their standard deviation (volatility). The above funds have given good performance with lower risk.

In this year’s list, I have replaced Franklin Prima Fund with DSP Mid-cap fund. In case, you are investing in Franklin fund, can continue with your investments.

Axis Mid-cap fund has a current allocation of 12.18% in large cap stocks, 66.29% in mid cap stocks & 8.11% in small cap stocks.

DSP Mid-cap fund has good upside and downside capture ratios.

You may keep an eye on Invesco Mid-cap fund as well.

Best ELSS Tax Saving mutual Funds 2021

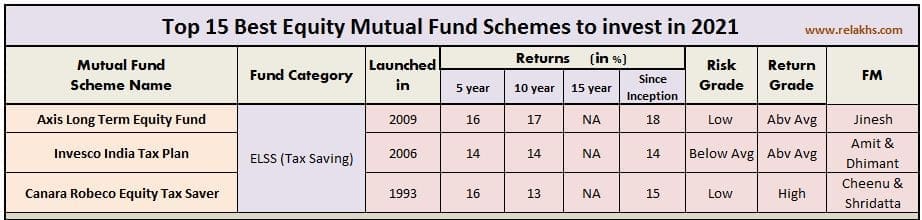

We currently have around 38 funds under the ELSS Fund category. The average returns from ELSS fund category are around 13.5% and 12% in the last 5 and 10 years respectively.

In my opinion, below are the consistent and best ELSS Mutual Funds to invest for tax saving and long term wealth creation;

Below are the best aggressive Equity Hybrid (Balanced) Funds ;

HDFC Hybrid Equity Fund

ICICI Prudential Equity & Debt Fund

Canara Robeco Equity Hybrid Fund

SBI Equity Hybrid Fund

There are currently around 45 equity hybrid funds. The average returns generated under this category have been around 14% in the last 7 years.

The risk grade has improved for funds of Canara and SBI, whereas, it has slightly deteriorated for HDFC Hybrid Equity and ICICI Pru funds.

HDFC Hybrid Equity Fund has 75.08% investment in Indian stocks of which 54.02% is in large cap stocks, 4.26% is in mid cap stocks, 8.8% in small cap stocks. It has 22.12% investment in Debt of which 6.33% in Government securities, 15.25% in funds invested in very low risk securities.

The ICICI Pru fund has 76.55% investment in Indian stocks of which 61.48% is in large cap stocks, 7.52% is in mid cap stocks, 6.3% in small cap stocks. It also has 17.93% investment in Debt of which 0.15% in Government securities, 17.03% in funds invested in very low risk securities.

The Canara Robeco Fund has 73.71% investment in stocks of which 49.4% is in large cap stocks, 12.42% is in mid cap stocks, 2.82% in small cap stocks. It has 15.26% investment in Debt of which 3.56% in Government securities, 11.7% in funds invested in very low risk securities.

SBI Equity HybridFund has 73.66% investment in Indian stocks of which 49.38% is in large cap stocks, 10.89% is in mid cap stocks, 3.56% in small cap stocks. The Fund has 18.77% investment in Debt of which 9.97% in Government securities, 8.13% in funds invested in very low risk securities.

You may track Mirae Asset Hybrid Equity Fund as well.

We (my spouse & myself) have decided to opt for ‘new tax regime‘, hence ready to forgo Section 80c tax deductions. So, I have decided to discontinue my future investments in Axis LTE ELSS Tax Saving Fund (will hold on to the existing units though).

I have recently redeemed my investments in Franklin Smaller Companies fund.

I have added one more Equity Hybrid Fund to my MF portfolio – SBI Equity Hybrid Fund.

So, I have been actively making investments in three Equity Mutual fund schemes for now;

HDFC Hybrid Equity Fund

UTI Nifty Next 50 Index Fund &

SBI Hybrid Equity Fund

My latest Equity Mutual Fund Portfolio

Mutual Fund Capital Gain Tax Rates for FY 2020-21 / AY 2021-22

One of the important amendments of the Financial Bill 2020-21 is ‘abolition of Dividend Distribution Tax’ in companies hands. As DDT will not be paid by the companies, dividend income (from April 2020) is taxed and paid by investor, at applicable individual tax slab rates.

Capital Gains Tax Rates on Mutual Fund Investments of a Resident Indian for FY 2020-21 are as below;

The STCG (Short Term Capital Gains) tax rate on equity funds is 15%.

The STCG tax rate on Non-Equity funds (or) Debt funds is as per the investor’s income tax slab rate.

The LTCG (Long Term Capital Gains) tax rate on equity funds is 10% on LTCG exceeding Rs 1 Lakh.

Some Important Points to ponder about Mutual Fund Investments :

Identify your Goals : Majority of us identify the products first and then try to shortlist best investment avenues. An investor has to first identify his/her financial goals and then try to short-list best available options. This is applicable for mutual fund investments also.

Set you Asset Allocation : Asset allocation is an exercise to invest across various avenues such as time-deposits, bonds, equities, gold etc., Set your allocation based on your investment objective, time-horizon and risk tolerance. For example : If your investment horizon is say 10+ years, objective is to wealth accumulation, you can consider an asset allocation of Equity to Debt as 60:40. Besides investing in Equity oriented products, it is equally important to invest in debt-oriented products (like PPF, EPF, VPF, Debt Funds etc.,) as well.

Is it good to invest in multiple Schemes from same Fund category? – Kindly do not invest in too many funds especially within the same fund category. Over-diversification is not beneficial and may lead to high portfolio overlap.

Consistency is the key parameter : A ‘good mutual fund scheme’ is the one that consistently manages to outperform its category returns and also it’s Benchmark’s. It is prudent to be with the consistent performers for long-term goals instead of churning your portfolio based on Star ratings or recent performances of the funds.

If you observe, the recent stellar performances have come from equity funds managed by the fund houses like Axis, Canara, DSP, UTI…The funds managed by HDFC, Franklin & Birla have taken a back seat. But, do not churn your portfolio based on recent performances alone. Look for consistency of returns and then take decision!

I am 60 years old, can I invest in Equity Funds? – Invest in Equity funds based on your future goals & financial resources and not based on your current age. For example – If you are a retiree (say 65 years) and have regular income which is more than your monthly living expenses, you can surely invest a portion of your surplus income in hybrid or equity oriented mutual funds.

Importance of Portfolio Performance – If one of the schemes in your MF portfolio is not performing well, do not immediately churn your portfolio. Also, do not churn your portfolio very often based on fund star ratings. The negative consequences of regularly churning the portfolio are undeniable. Do track that scheme’s performance for sometime (say 1 or 2 years) before deciding to drop it from your portfolio. Sometimes, it is prudent to analyze the overall portfolio performance than to get too worried about individual fund’s performance. Also, have realistic return expectation from your investments.

Shall I invest in Focused/Value oriented MF Schemes? – If you have created a core portfolio with say a Large cap fund / Index Fund, mid-cap fund (or index based funds) & Hybrid fund, you may invest a portion of your investible surplus in focused, value oriented, Funds of funds or Theme based funds. Ex : Parag Parikh Long Term Value Fund, Axis Focused 25 Fund etc.,

Shall I pick Index Funds? – If you are not comfortable investing in actively managed Funds, you can consider investing in Index based Funds. Ex : UTI Nifty 50 Fund (Large-cap), UTI Next Nifty 50 Index Fund (Large + Midcap) etc., It makes sense, to add one Hybrid Equity Fund to your Index based portfolio, to manage the volatility.

SIP or Lump sum? – Systematic Investment Plan (SIP) inculcates financial discipline. However, it is not a fair comparison to equate SIPs with investing in a lump sum. Both have their own pros and cons. It is better to have SIPs in place and at the same time, you can make additional investments (lump sum) when you believe that markets are down.

Suggest you not to remain invested in equity oriented funds till the goal target year. You may consider redeeming MF units by starting SWP (Systematic Withdrawal Plan)may be 2 to 3 years before the goal year. You can re-invest this amount in safe investment avenues. You may also re-balance your portfolio based on your Asset-allocation strategy (Equity : Debt allocation).

DIY / Advisor – If you are a DIY investor, pick Growth and Direct plans. In case, you are not comfortable investing in Mutual funds on your own or do not have the required time, do engage with a fee-only Financial planner.

Kindly note that the above list of top & best mutual funds 2021 is not an exhaustive one. Mutual funds’ returns are not guaranteed, their values/returns change frequently and past performance may not be repeated. MFs are subject to various market risks.

(Data Source & references : Valueresearchonline, Moneycontrol, Morningstar, Freefincal & The Economictimes)(Post first published on : 21-January-2021)

This post was last modified on July 12, 2023 6:11 pm

Sreekanth Reddy

Sreekanth is the Man behind ReLakhs.com. He is an Independent Certified Financial Planner (CFP), engaged in blogging & property consultancy for the last 14 years through his firm ReLakhs Financial Services . He is not associated with any Financial product / service provider. The main aim of his blog is to "help investors take informed financial decisions." "Please note that the views given in this Blog/Comments Section/Forum are clarifications meant for reference and guidance of the readers to explore further on the topics/queries raised and take informed decisions. The information provided, therefore, should not be viewed as financial, legal, accounting, tax or investment advice."

I have ongoing SIP’s in the following funds. My investment objective is retirement and timeframe is 12 years. Could you please review and advise if these are still good to continue SIP’s in?

1.Aditya Birla Sun life Tax Relief ’96 Fund - for 80c tax benefits

2.HDFC Hybrid Equity Fund

3.Axis mid cap Fund

4.SBI Large cap Fund

Your advise is greatly appreciated. Thank you.

Dear Sneha,

As your time horizon 12 years you can add small cap like : Tata Small Cap/ Quant Small Cap and discontinue HDFC Hybrid Equity Fund.

Hi Srikanth,

I have one flat. Loan is closed. Also I have some investments in Mutual funds. Please advise on investing in second flat for investment purpose. For this I have to redeem part of mutual funds.

I have covered all basics. I am following your blog last 5 to 6 years. Please advise.

Thanks,

Harinath

Dear Sreekanth,

of late, falling interest rates make me think about my RDs. I was investing 3000 per month in RDs. I want to invest same 3000 in mutual funds for wealth accumulation. my investment horizon is 15 years. Kindly advice me regarding funds to go about.

Hi Srikanth,

Me and spouse doing SIP in below MF's:-

- ICICI Bluechip fund

– HDFC Mid cap opportunities

– Mirae Asset Bluechip Long term

– Kotak Flexibcap

– Motilal N 100 FOF

– Kotak Gold Fund

Now,would like to add new SIP worth of 5k. Can you suggest some small/mid cap scheme. Looking for 7-10 years horizon

Dear Nimit,

For 7 to 10 years horizon you could consider the small cap :

1) Axis Small Cap Rs. 2500/- PM

2) Quant Small Cap Rs. 2500/- PM

Dear Srikanth,

I have few investments in L&T mid cap fund, DSP small cap fund. At present they delivered good returns compare to last year. Shall I redeem & keep in FD. So that I can make investments after few months or I will wait for small corrections to invest into a better performing funds.

Please suggest a better strategy.

Thanks,

Harinath

Hi Sir,

How would you rate Quant Active -G-Dir

for flexi cap fund ?

Thanks

JJ

Hi Srikanth,

I am having investment in Mirae asset large cap fund. Do you want me shift in staggered manner to UTI index fund.

Please suggest.

Dear Harinath,

Advisable to so if your investment horizon is long term (from now)..

But, watch out for tax implications.

If you are not comfortable with taxes then you can atleast make future investments go to index fund.

I am aware of Arbitrage fund as I do follow all your articles.

Just wanted some better returns than falling interest rate of bank FDs & RDs and after 3 yrs of time frame repay Home Loan, so suggested above Short-Term MF

1) Axis Short Term Dir Growth

2) ICICI Pru Short Term Dir Growth

as Arbitrage fund also give returns of approx. 6% for 3yrs

I am expecting 8% return for 3 yrs with less volatile, are above Short-Term Debt MF option good, I am still in 20% Income Tax bracket.

Dear Nitin,

If you are ok with taking risk (associated with debt funds), you may kindly go ahead with the above mentioned ones.

Kindly note that - A falling interest rate regime results in a lower return from short-term debt funds. However, long-term debt funds perform well in a falling interest rate regime.

We may be at the lower end of rate cycle as of now..

Hello Sreekanth,

Good afternoon!

How would you rate IIFL Bonds (annual rate of return 10 %) .

Objective is safety of capital .Can hold for 5-6 yrs.Is it advisable to look at it as a alternative to FD.

Thank you,

Roy

Dear Roy,

We are currently in a 'low interest rate' scenario.

Given this, a 10% return comes with certain risk, is n't it?

If your objective is 'safety of capital', you may kindly avoid this NCD series!

Hello Sreekanth,

Thank you for sharing valuable information related to Mutual Fund.

Just had small doubt, in falling interest rate of Banks Fixed Deposit & Recurring Deposit can Gilt fund like Axis Gilt Fund be alternative to invest for 3 plus years. Planning to repay Home Loan using that lumpsum amount after 3 plus years

Thank You and appreciate your time and effort for sharing information.

Sreekanth Ji,

Also if you think Short-Term Mutual Funds can be alternative for 3 years of time duration (Gilt fund), could you please suggest any one Short-Term MF from bellow ones:

1) Axis Short Term Dir Growth

2) ICICI Pru Short Term Dir Growth

Thank You

Dear Nitin,

Kindly note that Gilts can be highly volatile as they are sensitive to the interest rate movement. Are you ready to take this risk?

The returns on gilt funds rise when interest rates are falling and vice-versa.

The interest rate cycle can be at its bottom end. So, if rates start to raise then the returns from Gilt funds can be not so great.

Yes, I am aware of Arbitrage fund as I do follow all your articles.

Just wanted some better returns than falling interest rate of bank FDs & RDs and after 3 yrs of time frame repay Home Loan, so suggested above Short-Term MF

1) Axis Short Term Dir Growth

2) ICICI Pru Short Term Dir Growth

as Arbitrage fund also give returns of approx. 6% for 3yrs

I am expecting 8% return for 3 yrs with less volatile, are above Short-Term Debt MF option good, I am still in 20% Income Tax bracket.

{kind=link}

View Comments

Dear Srikanth,

I have ongoing SIP’s in the following funds. My investment objective is retirement and timeframe is 12 years. Could you please review and advise if these are still good to continue SIP’s in?

1.Aditya Birla Sun life Tax Relief ’96 Fund - for 80c tax benefits

2.HDFC Hybrid Equity Fund

3.Axis mid cap Fund

4.SBI Large cap Fund

Your advise is greatly appreciated. Thank you.

Dear Sneha,

As your time horizon 12 years you can add small cap like : Tata Small Cap/ Quant Small Cap and discontinue HDFC Hybrid Equity Fund.

Hi Srikanth,

I have one flat. Loan is closed. Also I have some investments in Mutual funds. Please advise on investing in second flat for investment purpose. For this I have to redeem part of mutual funds.

I have covered all basics. I am following your blog last 5 to 6 years. Please advise.

Thanks,

Harinath

Dear Sreekanth,

of late, falling interest rates make me think about my RDs. I was investing 3000 per month in RDs. I want to invest same 3000 in mutual funds for wealth accumulation. my investment horizon is 15 years. Kindly advice me regarding funds to go about.

Hi Srikanth,

Me and spouse doing SIP in below MF's:-

- ICICI Bluechip fund

– HDFC Mid cap opportunities

– Mirae Asset Bluechip Long term

– Kotak Flexibcap

– Motilal N 100 FOF

– Kotak Gold Fund

Now,would like to add new SIP worth of 5k. Can you suggest some small/mid cap scheme. Looking for 7-10 years horizon

Dear Nimit,

For 7 to 10 years horizon you could consider the small cap :

1) Axis Small Cap Rs. 2500/- PM

2) Quant Small Cap Rs. 2500/- PM

Dear Srikanth,

I have few investments in L&T mid cap fund, DSP small cap fund. At present they delivered good returns compare to last year. Shall I redeem & keep in FD. So that I can make investments after few months or I will wait for small corrections to invest into a better performing funds.

Please suggest a better strategy.

Thanks,

Harinath

Hi Sir,

How would you rate Quant Active -G-Dir

for flexi cap fund ?

Thanks

JJ

Hi Srikanth,

I am having investment in Mirae asset large cap fund. Do you want me shift in staggered manner to UTI index fund.

Please suggest.

Dear Harinath,

Advisable to so if your investment horizon is long term (from now)..

But, watch out for tax implications.

If you are not comfortable with taxes then you can atleast make future investments go to index fund.

Related article : Mutual Funds Taxation Rules FY 2020-21 (AY 2021-22) | Capital Gains Tax Rates Chart

Hello Sreekanth Ji,

I am aware of Arbitrage fund as I do follow all your articles.

Just wanted some better returns than falling interest rate of bank FDs & RDs and after 3 yrs of time frame repay Home Loan, so suggested above Short-Term MF

1) Axis Short Term Dir Growth

2) ICICI Pru Short Term Dir Growth

as Arbitrage fund also give returns of approx. 6% for 3yrs

I am expecting 8% return for 3 yrs with less volatile, are above Short-Term Debt MF option good, I am still in 20% Income Tax bracket.

Dear Nitin,

If you are ok with taking risk (associated with debt funds), you may kindly go ahead with the above mentioned ones.

Kindly note that - A falling interest rate regime results in a lower return from short-term debt funds. However, long-term debt funds perform well in a falling interest rate regime.

We may be at the lower end of rate cycle as of now..

Hello Sreekanth,

Good afternoon!

How would you rate IIFL Bonds (annual rate of return 10 %) .

Objective is safety of capital .Can hold for 5-6 yrs.Is it advisable to look at it as a alternative to FD.

Thank you,

Roy

Dear Roy,

We are currently in a 'low interest rate' scenario.

Given this, a 10% return comes with certain risk, is n't it?

If your objective is 'safety of capital', you may kindly avoid this NCD series!

Hello Sreekanth,

Thank you for sharing valuable information related to Mutual Fund.

Just had small doubt, in falling interest rate of Banks Fixed Deposit & Recurring Deposit can Gilt fund like Axis Gilt Fund be alternative to invest for 3 plus years. Planning to repay Home Loan using that lumpsum amount after 3 plus years

Thank You and appreciate your time and effort for sharing information.

Sreekanth Ji,

Also if you think Short-Term Mutual Funds can be alternative for 3 years of time duration (Gilt fund), could you please suggest any one Short-Term MF from bellow ones:

1) Axis Short Term Dir Growth

2) ICICI Pru Short Term Dir Growth

Thank You

Dear Nitin,

Kindly note that Gilts can be highly volatile as they are sensitive to the interest rate movement. Are you ready to take this risk?

The returns on gilt funds rise when interest rates are falling and vice-versa.

The interest rate cycle can be at its bottom end. So, if rates start to raise then the returns from Gilt funds can be not so great.

Are you aware of Arbitrage funds?

Thank you for replying Sreekanth Ji

Yes, I am aware of Arbitrage fund as I do follow all your articles.

Just wanted some better returns than falling interest rate of bank FDs & RDs and after 3 yrs of time frame repay Home Loan, so suggested above Short-Term MF

1) Axis Short Term Dir Growth

2) ICICI Pru Short Term Dir Growth

as Arbitrage fund also give returns of approx. 6% for 3yrs

I am expecting 8% return for 3 yrs with less volatile, are above Short-Term Debt MF option good, I am still in 20% Income Tax bracket.

Hello Sreekanth Ji,

Any thought on this.....