Retirement planning in India is often misunderstood. Many people think any long-term savings or investment plan can give them a pension, but that’s not true. Only a few options are actually designed to give you a regular income after retirement.

That difference matters because retirement is not just about building a corpus. It’s about making sure money keeps coming in even after your active income stops.

In India, true pension options are limited. There are many savings and investment products, but only a handful really qualify as pure pension schemes—those that turn your contributions into a monthly income during retirement. Some of these are mandatory depending on your job, while others are voluntary and need you to opt in.

In this article, let’s break down the five main pension schemes in India—

- Employees’ Pension Scheme (EPS)

- National Pension System (NPS)

- Atal Pension Yojana (APY)

- Insurance-based pension plans and

- Superannuation schemes.

We’ll keep it simple and cover their features, eligibility, lock-in rules, and pros and cons so you can see which ones actually fit your retirement plan.

Pension Oriented Schemes in India – Complete Guide

Planning for retirement is no longer just about “saving”; it’s about choosing the right vehicle to combat inflation and ensure a steady income. Here is a breakdown of the top 5 pension-related schemes in India

1) Employees’ Pension Scheme (EPS)

Managed by the EPFO, this is a social security scheme for organized sector employees.

- Who can subscribe: Any employee who is a member of EPF.

- Key feature: 8.33% of the employer’s contribution goes into this pension fund.

- Eligibility: At least 10 years of service and age 58.

- Lock-in / Exit: Locked till retirement, though early pension can start from age 50 with a reduced payout.

- 2026 update on withdrawal: The pension part can now be withdrawn only after 36 months of leaving the job, instead of 2 months.

- Also, at least 25% of your PF balance must stay untouched until retirement so you keep a basic pension base.

Pros: Guaranteed lifelong pension, plus survivor benefits for spouse and children.

Cons: Returns are fixed and formula-based, so usually lower than market-linked schemes. It is mandatory for employees earning up to ₹15,000 basic salary.

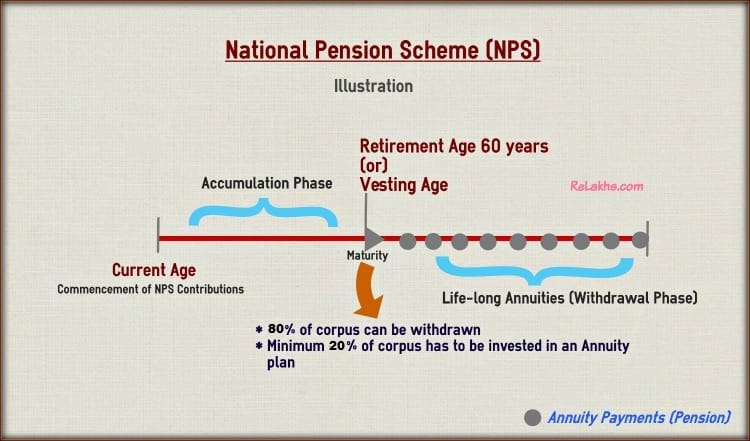

2. National Pension System (NPS)

A market-linked, voluntary retirement scheme regulated by the PFRDA. It is widely considered the most flexible pension tool in 2026.

- Who can subscribe: All Indian citizens (including NRIs and OCIs) aged 18–85.

- Key Features: Choice of investment (Equity, Corporate Bonds, Government Bonds). Includes NPS Vatsalya for minors.

- 2026 Update – Withdrawal Rules:

- Maturity (Age 60): You can now withdraw up to 80% as a tax-free lump sum (increased from 60%). The remaining 20% must be used for an annuity.

- Full Exit: If the total corpus is ≤ ₹8 Lakh, you can withdraw 100% without buying an annuity.

- Premature: Partial withdrawals (up to 25% of own contributions) allowed for specific reasons (education, illness) after 3 years.

Pros: High return potential; extra tax deduction of ₹50,000 (Sec 80CCD(1B)); lowest management fees globally.

Cons: Market-linked (returns aren’t guaranteed); annuity income is taxable.

Important Note: Unlike traditional pension schemes, NPS itself does not guarantee a pension. It builds a retirement corpus, and you must convert a portion of it into an annuity to generate monthly income. You need to buy an annuity plan from a life insurer. The quality of your pension under NPS depends not just on your corpus, but also on the annuity rates available at retirement.

Update: Unified Pension Scheme (UPS)

The government has introduced the Unified Pension Scheme (UPS) for central government employees as an alternative framework alongside NPS. Unlike NPS, which is market-linked, UPS aims to provide a more predictable pension structure (Assured pension + contribution-based structure). However, this scheme is currently limited to government employees and is not available for the general public.

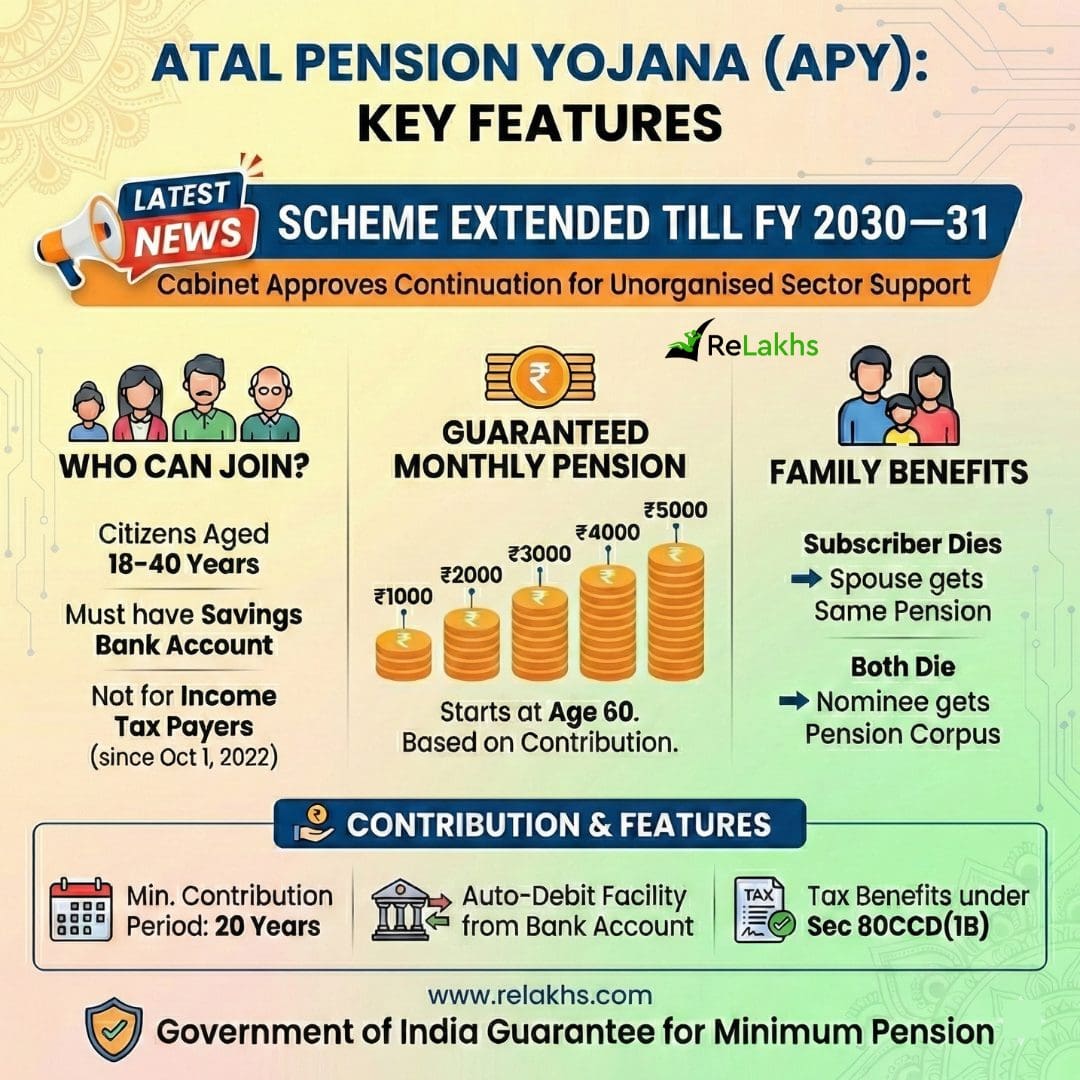

3. Atal Pension Yojana (APY)

Government-backed scheme mainly for unorganized sector workers, guaranteeing a minimum pension.

- Who can join: Indian citizens aged 18–40.

- Note: Income tax payers can’t join since 2022.

- Key features: Fixed pension options—₹1,000, ₹2,000, ₹3,000, ₹4,000, or ₹5,000 monthly.

- Withdrawal rules:

- Maturity: Auto-starts at age 60

- Premature: Not allowed (except terminal illness or death)

Pros: Govt guarantee + triple benefit (you → spouse → corpus to nominee). Suitable for low-income individuals

Cons: Entry capped at 40 years; fixed pension won’t beat high inflation.

4. Life Insurance Pension Schemes

Private/Public insurance companies (like LIC, SBI Life) offer “Annuity” or “Retirement” plans.

- Who can subscribe: Anyone (typically entry age 18–70).

- Eligibility: Based on the specific policy’s health and age criteria.

- Key Features: Two phases—Accumulation (paying premiums) and Vesting (receiving pension/annuities).

- Types of Annuities:

- Deferred annuity: Build corpus first (accumulation phase), then convert to pension later.

- Immediate annuity: Pension starts right away after one-time investment.

- Withdrawal Rules:

- Lock-in: Typically 3–5 years.

- Maturity: Usually, 60% can be taken as a lump sum (tax-free rules apply per Section 10(10D)), and 40% is annuitized.

Pros: Fixed, guaranteed income options (traditional plans); death benefit (life cover) often bundled.

Cons: High surrender charges if exited early; lower returns compared to NPS.

5. Superannuation (Super Annuity)

Employer-sponsored pension scheme managed via approved superannuation funds. It is a corporate pension program where the employer contributes to a fund for the employee’s retirement.

- Who can join: Employees of companies offering superannuation benefits.

- Key features: Employer contributes up to 15% of basic salary (defined contribution or benefit).

- Withdrawal rules:

- Retirement: Withdraw 1/3rd (33.3%) tax-free lump sum. Remaining 2/3rd → must buy annuity. (Similar to NPS structure)

- Job change: Transfer to new employer’s fund or keep until retirement or Withdraw (tax implications).

Pros: Big corpus from employer money + tax-free contribution up to ₹1.5 lakh.

Cons: Only for corporate employees; rigid 1/3rd withdrawal rule.

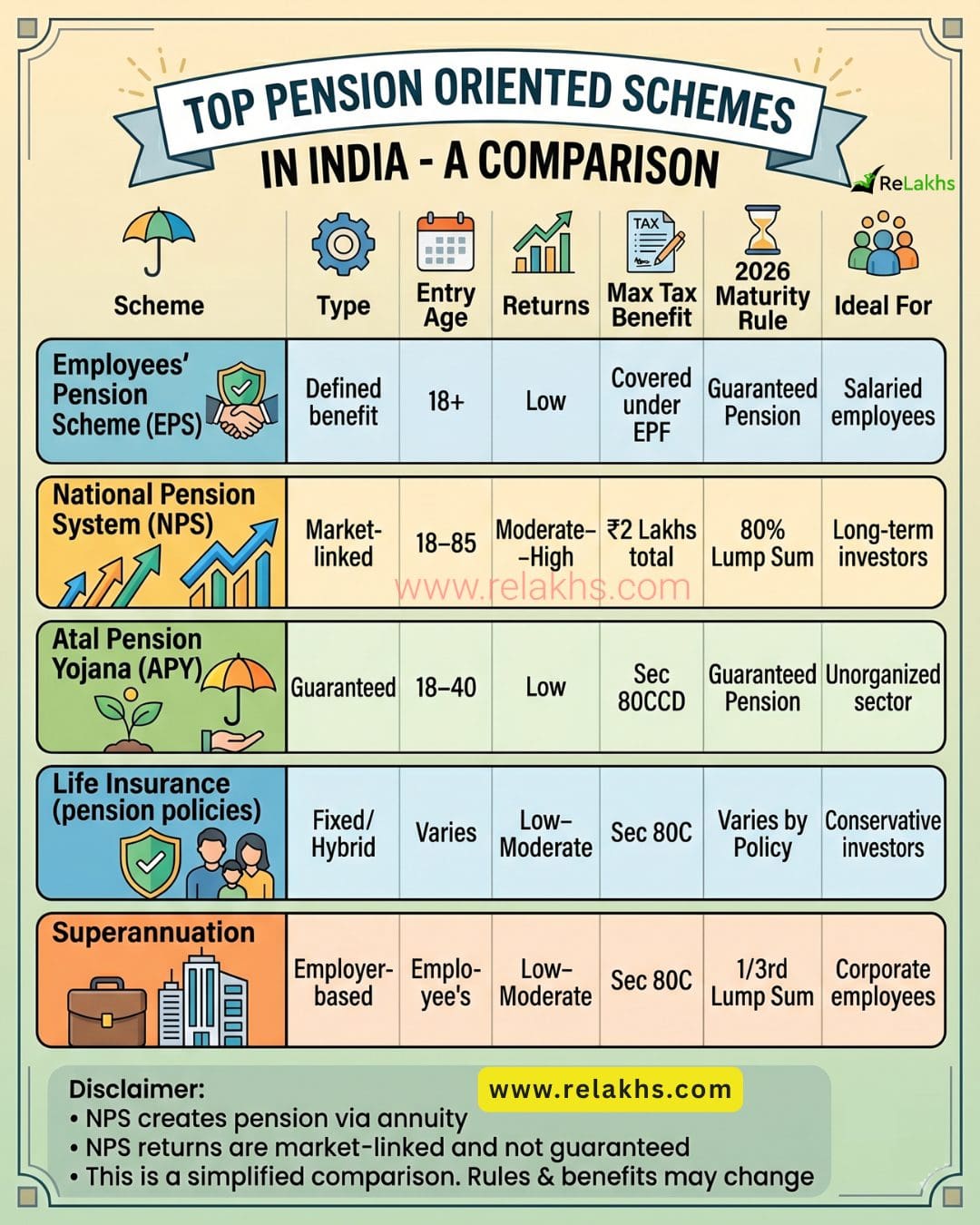

Pension Schemes – Quick Comparison Table

| Scheme | Type | Entry Age | Returns | Max Tax Benefit | 2026 Maturity Rule | Ideal For |

|---|---|---|---|---|---|---|

| EPS | Defined benefit | 18+ | Low | Covered under EPF | Guaranteed Pension | Salaried employees |

| NPS | Market-linked | 18–85 | Moderate–High | ₹2 Lakhs total | 80% Lump Sum | Long-term investors |

| APY | Guaranteed | 18–40 | Low | Sec 80CCD | Guaranteed Pension | Unorganized sector |

| Life Insurance | Fixed/Hybrid | Varies | Low–Moderate | Sec 80C | Varies by Policy | Conservative investors |

| Superannuation | Employer-based | Employee | Low–Moderate | Sec 80C | 1/3rd Lump Sum | Corporate employees |

Other Pension-like Income Options

Not Exactly Pension Schemes… But Useful for Retirement Income

These aren’t true pensions (no guaranteed lifelong payout), but they can create steady retirement cash flow:

- PPF: Tax-free, safe, but 15-year lock-in (extensions possible).

- SCSS: 5%+ interest for seniors (60+), 5-year tenure.

- Post Office MIS: 7%+ monthly interest, low-risk.

- Mutual Fund SWP: Flexible withdrawals from equity/debt funds (market-linked).

Key difference: Pensions pay for life. These have fixed tenures or flexible withdrawals.

“While the above are not pure pension schemes, they play a crucial role in retirement planning. In reality, a combination of pension schemes like NPS along with income options like SCSS or SWP can create a stable and inflation-beating retirement income.”

Final Thoughts

No single scheme can take care of your entire retirement. A solid retirement plan is always a combination of growth, safety, and income strategies.

The most practical approach for Indian investors is to combine:

- NPS for long-term, market-linked growth

- EPF/PPF for stability and tax efficiency

- Mutual Funds for flexibility and inflation-beating returns

- SCSS (post-retirement) for steady income

When it comes specifically to pure pension oriented schemes, each serves a different purpose:

- For growth & flexibility: NPS stands out in 2026 due to its low cost and market-linked returns

- For safety & guaranteed income: APY and EPS offer predictable pension, though with limitations

- For high-net-worth individuals: Life insurance pension plans can provide structured, guaranteed annuities along with legacy planning benefits

Ultimately, there is no “one-size-fits-all” solution. The right mix depends on your age, risk appetite, income stability, and retirement goals. The earlier you plan and diversify across these options, the more secure and stress-free your retirement can be.

Continue reading:

(Post first published on : 24-April-2026)

Join our channels