Most of us constantly look at “returns” on our investments. But very few of us think about the real enemy that quietly eats into those returns – inflation. The logic is very simple: if your money is not growing faster than inflation, you are actually getting poorer year after year.

Let me walk you through this with a simple, real-life example.

Think about a simple family dinner at a restaurant. Around 10–12 years ago, a decent outing for the whole family used to cost roughly ₹800–₹1,000. Today, the same kind of dinner easily comes to ₹4,000–₹5,000 in many cities.

Did the quantity become a lot more? Did the quality improve so much that the jump is fully justified? Not really.

This is inflation at work.

Prices keep going up over time, and your money keeps losing its purchasing power. ₹100 today will not buy you the same things 10 or 20 years from now. That’s exactly why inflation is an important factor in every financial decision you make.

Why Inflation Is Important for the Economy?

Inflation is not always a villain. In fact, a moderate level of inflation is actually healthy for the economy.

Why? Because:

- It nudges people to spend and invest instead of just hoarding cash.

- It gives businesses room to gradually increase salaries and grow profits.

- It helps support overall economic growth.

That’s why central banks like the RBI aim to keep inflation at a manageable level, around 4% (their comfort zone). But at a personal level, inflation can quietly become a big problem, especially when you’re planning long-term goals like retirement, children’s education, or buying a house.

Why Inflation Matters for Individuals?

For individuals like you and me, inflation hits us mainly in three ways:

- Purchasing power:

- Your money keeps losing strength over time.

- Example: ₹1 lakh today will not give you the same lifestyle 20 years from now.

- Financial goals become costlier:

- A goal that costs ₹10 lakh today may cost ₹30–₹40 lakh in the future, depending on inflation.

- So, if you don’t account for inflation, you’ll seriously underestimate how much you actually need.

- Investments must beat inflation:

- If your investments are growing at 6% but inflation is 7%, your real return is negative.

- On paper it looks like you’re earning, but in reality your money is losing purchasing power.

That’s why inflation is a key input in every proper financial plan and goal calculation.

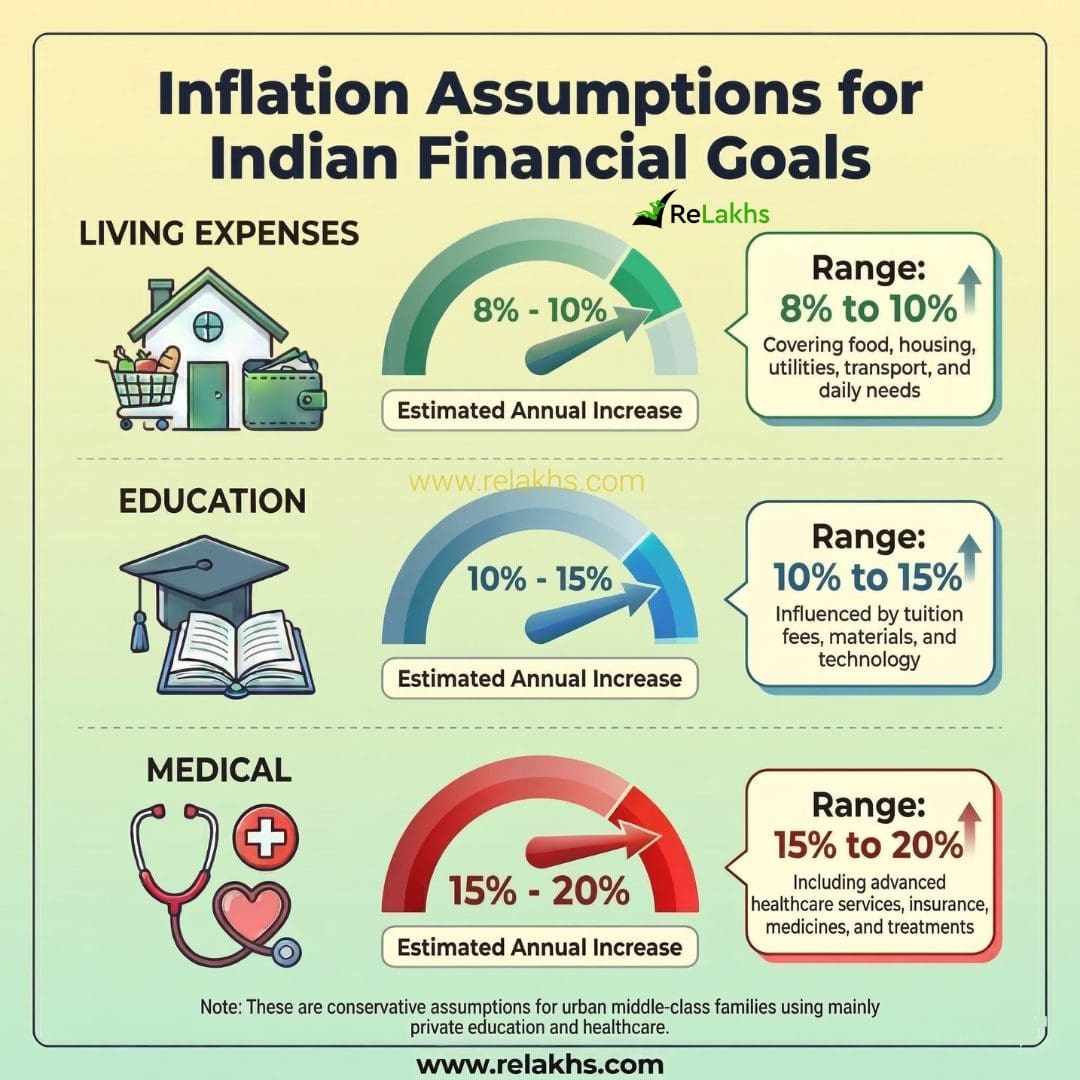

Inflation Assumptions for Financial Planning in India

Different expenses grow at different inflation rates. Based on long-term trends in India, it is advisable to assume the following ranges.

| Financial Goal | Typical Inflation Range | Why |

|---|---|---|

| Living Expenses | 8% – 10% | Food, rent, utilities, transport |

| Education | 10% – 15% | Tuition fees, private education costs |

| Healthcare | 15% – 20% | Medical treatments, hospital costs, technology |

A Real Example of Education Inflation

Education costs in India are shooting up fast, especially in private schools and colleges.

Take this example – private schools in Karnataka recently proposed a 15% fee hike for 2025–26, blaming inflation and rising costs. Many already charge ₹50,000–₹75,000 per year, while premium ones easily hit ₹2 lakh+.

That’s why financial planners use 10–15% education inflation when calculating future costs. Ignore this, and you’ll seriously underestimate how much you need to save for your child’s education.

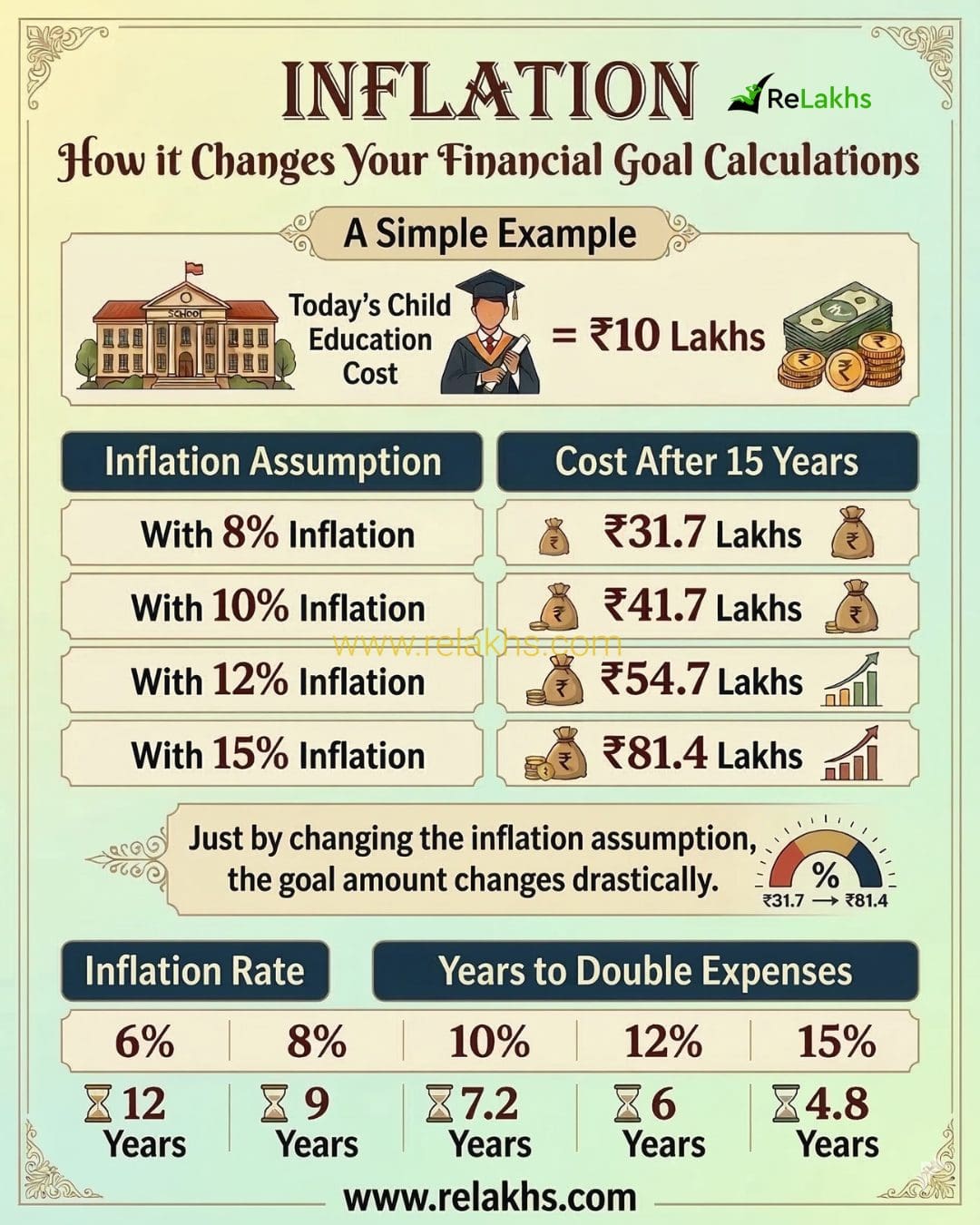

How Inflation Changes Your Goal Calculations

Let us take a simple example. Suppose your child’s college education costs ₹10 lakh today.

Just changing the inflation assumption can drastically change the goal amount. This is why correct inflation assumptions are critical while planning investments.

We can also understand this with a simple rule – The Rule of 72.

Years to double ≈ 72 ÷ Inflation Rate

| Inflation Rate | Years for Expenses to Double |

|---|---|

| 6% | 12 years |

| 8% | 9 years |

| 10% | 7.2 years |

| 12% | 6 years |

| 15% | 4.8 years |

• At 10% inflation, your expenses double every 7.2 years

• At 15% inflation, they double every 4.8 years

Now imagine planning retirement or kid’s education without considering this. Your financial plan could collapse.

Why Inflation Is Critical in Retirement Planning

When planning your retirement corpus, inflation is your silent partner you can’t ignore. Think about it – if you need ₹50,000 per month today to live comfortably, in 20 years that same lifestyle might cost ₹1.5–2 lakh after 8–10% inflation.

So, while saving, aim for investments that beat inflation consistently (equities, mutual funds typically target 10–12% returns). Underestimating this means your retirement nest egg will fall short, forcing you to cut corners later.

Even more critical is the withdrawal phase.

Once retired, inflation doesn’t stop – it keeps eroding your corpus. If you withdraw a fixed ₹1 lakh monthly without adjusting, you’ll run out faster as prices rise. Smart planners use a “safe withdrawal rate” of 3–4% initially, increasing it annually by inflation (like 6–7%). This way, your savings last 25–30 years without depleting.

In financial planning, ignoring inflation is like building a house on weak foundations — it may stand today, but it won’t last tomorrow.

Key Takeaways

- Inflation silently eats away at your purchasing power.

- Every financial goal needs inflation adjustment in calculations.

- Different goals mean different inflation rates.

- In India, typical planning assumptions:

- Living expenses → 8–10%

- Education → 10–15%

- Healthcare → 15–20%

- In India, typical planning assumptions:

- Even small inflation differences explode your future goal amounts.

The biggest financial planning mistake? Not low returns — it’s ignoring inflation.

Because the real question is not: “How much money will I have?”

The real question is: “What will that money be able to buy?”

Continue reading:

- 6 Banking Rules Every Bank Customer Should Know in 2026

- Latest Health Insurance Incurred Claim Ratio 2025 | Top Health Insurance Companies List

(Post first published on : 16-March-2026)

Join our channels