Filing your Income Tax Return (ITR) is not just about meeting deadlines—it’s about choosing the right option based on your situation.

What if you missed the due date? What if you already filed and later found a mistake? What if you discovered some income was left out? Picking the wrong route can mean extra tax, penalties, or even losing your refund.

This guide explains the difference between Belated Return, Revised Return, and Updated Return (ITR-U), with latest rules, in a simple, practical way.

ITR Belated vs Revised vs ITR-U – Key Differences Explained (2026)

| Feature | Belated Return | Revised Return | ITR-U (Updated Return) |

| Section of IT Act | Section 139(4) | Section 139(5) | Section 139(8A) |

| When to use | Missed original deadline | Correct errors/omissions | Disclose missed income late |

| Original ITR needed? | No (It’s the first filing) | Yes | Either (filed or not) |

| Deadline | Dec 31 of the AY | Mar 31 of the AY* | Up to 4 years (48 months)** |

| Frequency | Once | Multiple times | Only Once per AY |

| Carry Forward Losses? | ❌ No (except House Prop.) | ✅ Yes | ❌ No |

| Can Reduce Tax? | ✅ Yes | ✅ Yes | ❌ No (Must pay more) |

| Can Claim Refund? | ✅ Yes | ✅ Yes | ❌ No |

| Nil Return Allowed? | ✅ Yes | ✅ Yes | ❌ No (Must have tax liability) |

| Penalty / Fee | ₹1,000–₹5,000 (u/s 234F) | Nil | 25%–70% additional tax |

*Note: Deadline for Revised Return was extended to March 31 of the Assessment Year (AY) under Finance Bill 2026. Note: The ITR-U window was increased from 24 months to 48 months effective April 1, 2025.

Belated Return – If You Missed Filing

If you didn’t file your ITR within the due date (typically July 31/August 31), you can still file a Belated Return.

Key points:

- Deadline: 31 December of the assessment year

- Late fee: ₹1,000 if income is up to ₹5 lakh, ₹5,000 if income is above ₹5 lakh

- Interest: May apply under Section 234A

- Loss carry forward: Generally not allowed

👉 Use this option only if you have not filed your return at all.

Revised Return – Best Option to Fix Mistakes

If you have already filed your ITR and later find a mistake, this is usually the best and safest option to correct it.

You can fix missed income, wrong deductions, and incorrect personal or bank details. The big advantage is that you can usually avoid penalty, reduce extra tax where applicable, and still claim a refund if you are eligible.

Deadline for Revised Return

- You can revise your return up to March 31 of the relevant Assessment Year

- Or before completion of assessment, whichever is earlier

Processed vs Assessed – Critical Difference

Many taxpayers think once their ITR is processed, they can’t change it. That’s incorrect.

Processing under Section 143(1) is just an automated system check—you might get a refund or intimation, but you can still revise your return.

Assessment under Section 143(3) is different: detailed scrutiny by a tax officer. Once completed, revision isn’t allowed.

Simple Rule – Processing is not final. Scrutiny assessment is final.

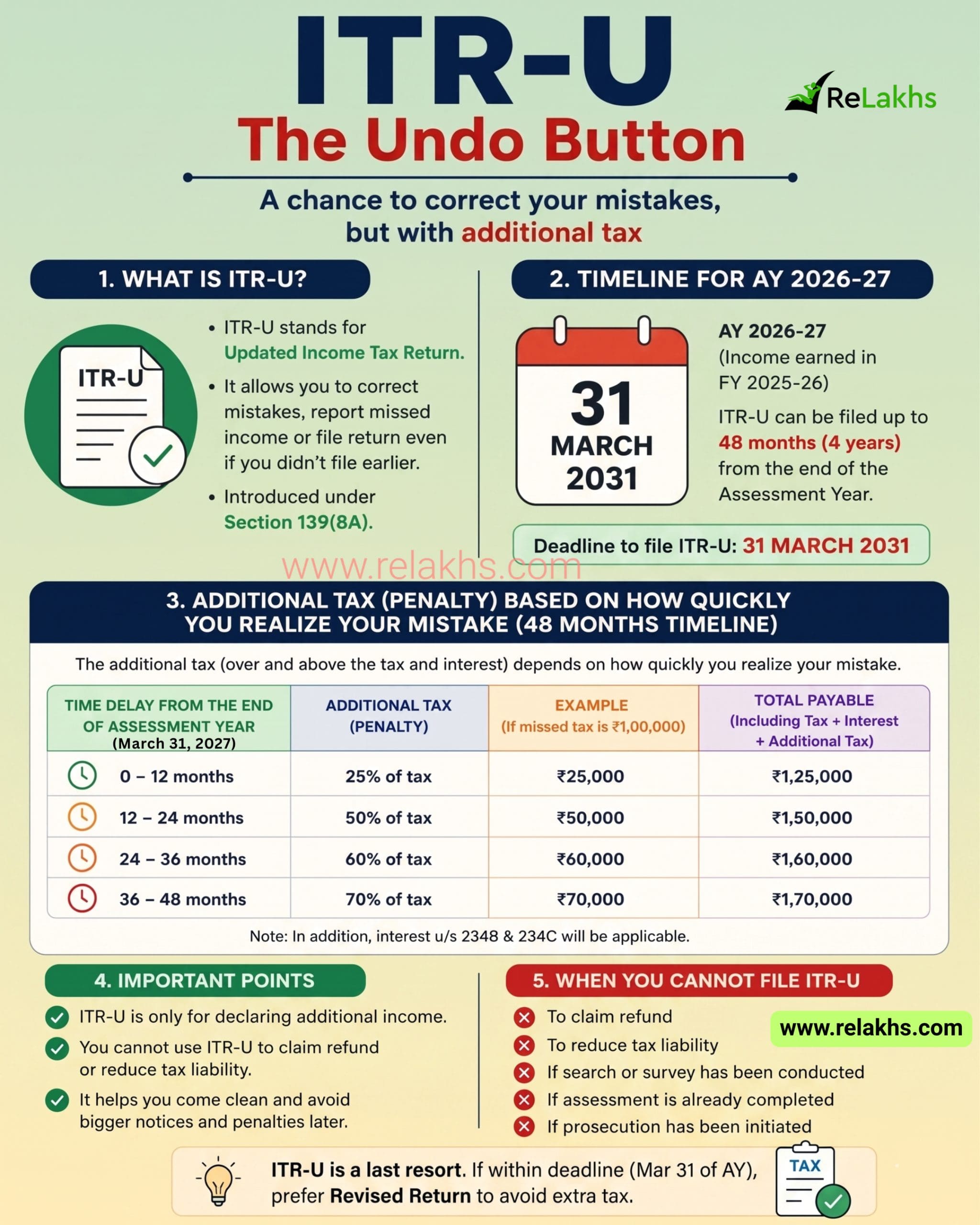

ITR-U (Updated Return) – Last Resort Option

ITR-U lets you voluntarily disclose missed income even after all regular deadlines pass. You can file it up to 4 years from the end of the relevant Assessment Year.

Additional Tax (time-based):

- Within 12 months: 25%

- 12–24 months: 50%

- 24–36 months: 60%

- 36–48 months: 70% (Over and above regular tax + interest)

Key restrictions include no refunds, no reduction in tax liability, and no increase in losses—making ITR-U a penalty-heavy last resort, not a correction tool.

Bottom line: ITR-U is a penalty-heavy final option, not a correction tool.

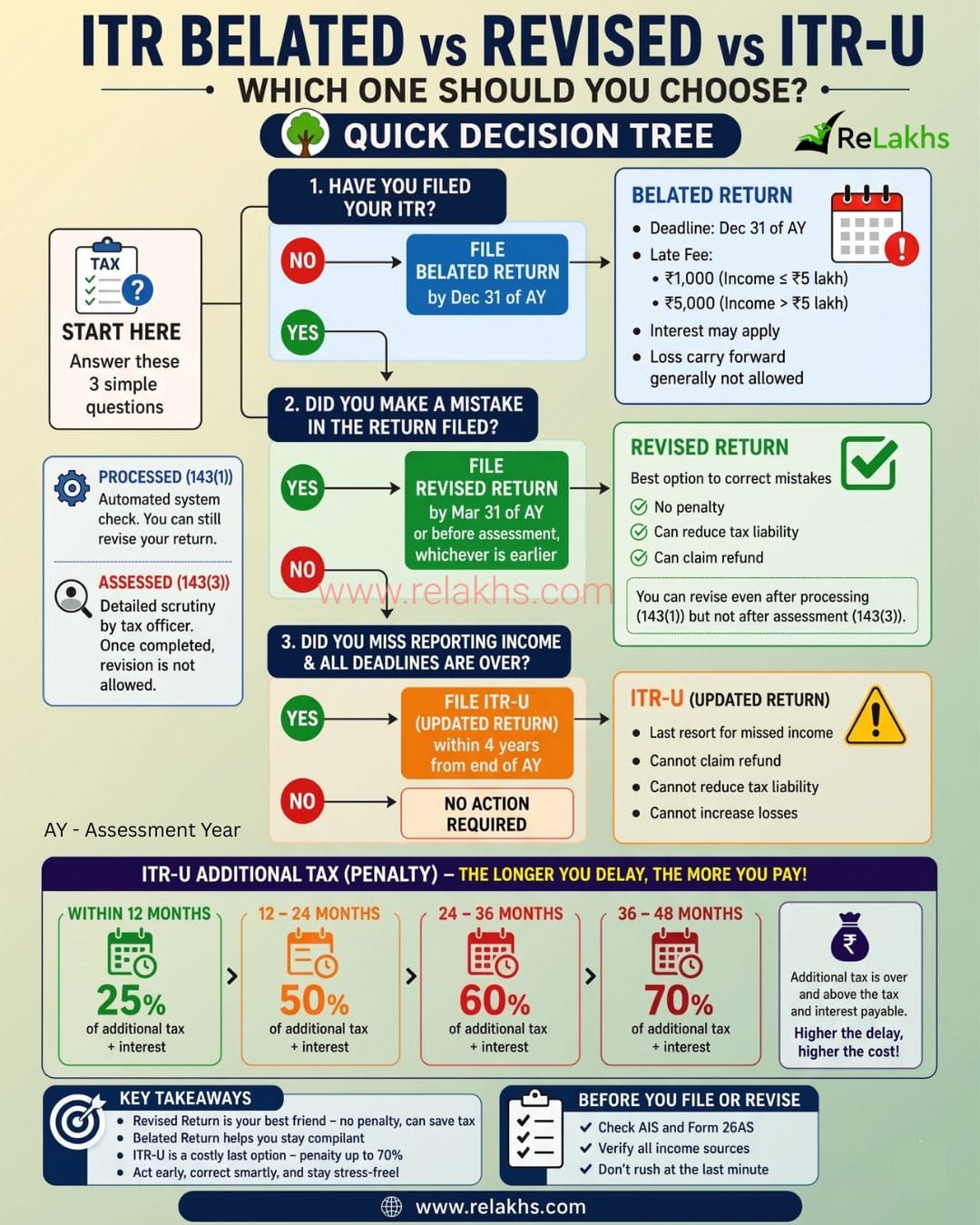

Which One Should You Choose? (Decision Guide)

o make this even simpler, refer to the infographic above—it visually walks you through a quick decision tree based on your situation. Just answer three questions: whether you’ve filed your return, whether there’s a mistake, and whether any income was missed after deadlines. The flow leads you to the correct option—Belated Return, Revised Return, or ITR-U.

It also highlights the penalty ladder for ITR-U, showing how the additional tax increases with delay. This visual summary helps you make the right choice at a glance without getting lost in technical details.

Real-Life Scenarios:

Scenario 1: Filed your return but later found missed FD interest? File a Revised Return (even if already processed).

Scenario 2: Didn’t file your return at all? File a Belated Return.

Scenario 3: Missed income discovered after all deadlines? File ITR-U.

Final Thoughts

If you keep it simple—Revised Return is always your best option because there is no penalty and you can still correct mistakes comfortably. Belated Return is just a compliance fallback if you missed filing. And ITR-U should be treated as a last resort, because it comes with a clear cost.

The longer you delay in filing ITR-U, the higher the additional tax—going up to 70%.

Before filing or revising your return, don’t rush blindly. Take a few minutes to check your AIS and Form 26AS, verify all your income sources properly, and act early instead of waiting till deadlines. A little review now can save you both tax and stress later.

Best approach? File your ITR within the original due date and avoid all these complications.

Continue reading:

- Income Tax Deductions FY 2026-27: Complete Guide to Old vs New Tax Regime

- Latest TDS Rates Tax Year 2026-27 – Complete Chart

(Post first published on : 29-April-2026))

Join our channels