If you’re in your 50s or 60s, you’ve probably heard someone say, “Those were the days… banks used to offer 12% interest on fixed deposits!” And if you’re a younger investor, you may have wondered, “Did FD rates really go that high?”

The answer is yes. But the story behind those rates is much more interesting.

In this article, let’s take a look at how one-year bank fixed deposit rates in India have changed over the last 35 years, why they moved the way they did, and what investors can learn from that journey.

Why This Topic Is Personal to Me?

This isn’t just another article with charts and numbers. It reminds me of a phase from my own life.

In 1992, I lost my father unexpectedly. He was working in a public sector bank. After his death, our family received the life insurance and accident insurance claim amounts. My mother was later given a compassionate appointment at a lower level in the same bank, but her salary was low. She suddenly became responsible for managing the family’s finances, and she had never handled investments before. She wasn’t familiar with stocks, or real estate.

Like many families at that time, her first priority wasn’t to earn the highest return. It was to protect the money. So she deposited almost the entire amount in bank fixed deposits.

Looking back today, I feel we were fortunate in one important way. During the early 1990s, bank FD interest rates were quite high, often around 10% to 12%. The monthly and annual interest from those deposits became one of our family’s main sources of income. It helped my mother manage household expenses and, most importantly, supported the education of both me and my sister.

Even now, whenever someone says, “FDs are boring investments,” I smile. For our family, those bank deposits weren’t just investments. They gave us stability during one of the most difficult phases of our lives.

That experience taught me an important lesson: sometimes the right investment isn’t the one with the highest return. It’s the one that helps your family sleep peacefully at night.

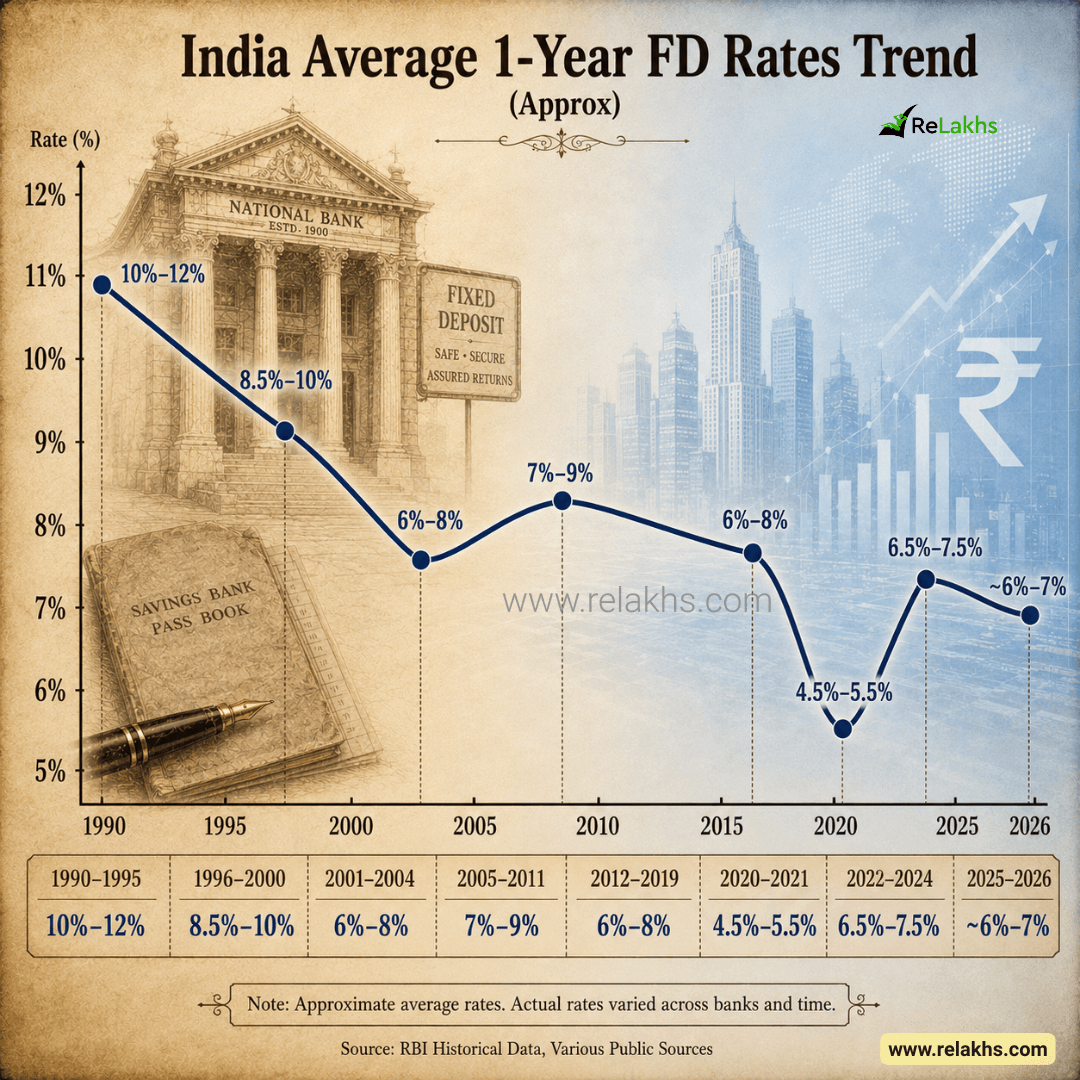

India’s Average 1-Year Bank FD Rates (1990–2026)

As you can see, FD interest rates have gone through several ups and downs over the past three and a half decades.

They don’t move randomly. They generally follow the interest-rate cycle in the economy. Let’s understand the journey.

| Time Period | Average 1-Year Bank FD Interest Rate (Approx.) |

|---|---|

| 1990–1995 | 10%–12% |

| 1996–2000 | 8.5%–10% |

| 2001–2004 | 6%–8% |

| 2005–2011 | 7%–9% |

| 2012–2019 | 6%–8% |

| 2020–2021 | 4.5%–5.5% |

| 2022–2024 | 6.5%–7.5% |

| 2025–2026 | Around 6%–7% |

Why Were FD Rates So High During the 1990s?

Many people still fondly remember earning 10% to 12% on bank fixed deposits in the 1990s. But those attractive returns came in a very different economic environment.

In 1991, India faced a severe balance of payments crisis, with foreign exchange reserves barely enough to cover a few weeks of imports. That period also triggered the landmark Liberalisation, Privatisation and Globalisation (LPG) reforms, which opened the economy to global competition and investment. At the same time, inflation was relatively high and interest rates across the economy were elevated.

Banks offered higher FD rates because lending rates were also much higher. Home loans, business loans, and personal loans often carried double-digit interest rates, so borrowing was far more expensive than it is today. In simple terms, high FD returns were not a free lunch — they reflected the broader realities of the economy, including higher inflation, tighter monetary conditions, and a higher cost of money.

So while depositors enjoyed attractive interest income, borrowers had to pay a much steeper price. A 12% FD may sound impressive today, but in that era, inflation was also higher, which reduced the real purchasing power of those returns.

This is an important reminder that FD rates do not move in isolation. They are closely linked to inflation, RBI policy, economic growth, and the overall demand and supply of money in the economy.

Why Did FD Rates Gradually Decline?

As India’s economy matured, inflation became more stable and interest rates gradually declined. The Reserve Bank of India’s monetary policy also evolved over the years, with a stronger focus on maintaining price stability. As a result, bank deposit rates slowly moved lower.

The COVID-19 Period

The lowest point in recent history came during the COVID-19 pandemic. To support the economy, the RBI reduced policy rates significantly. Banks had surplus liquidity and loan demand slowed sharply. As a result, one-year FD rates at many banks fell to around 4.5% to 5.5%. Many retirees and conservative investors felt the impact during this period.

The Rise After 2022

As inflation rose after the pandemic, the RBI began raising interest rates. Banks also started competing more aggressively to attract deposits. Consequently, FD rates climbed back to around 6.5%–7.5% before easing slightly again.

What Can Investors Learn?

One important lesson is that interest rates move in cycles. When rates are high, many investors assume they will stay high forever. When rates are low, many believe they will never increase again. History tells a different story. Interest rates rise, then fall, and then rise again.

Instead of trying to predict the perfect time, investors should align their FD strategy with their financial goals and cash-flow needs.

Final Thoughts

Whenever I see discussions comparing today’s FD rates with those of the 1990s, I remember my family’s journey. Those fixed deposits gave us financial stability when we needed it the most. They funded our education and gave my mother confidence during an uncertain phase of life.

Every investment has a purpose. Mutual funds help build long-term wealth. Equities help beat inflation over time. But bank fixed deposits continue to play an important role by offering stability, predictability, and peace of mind. Perhaps that’s why, even after all these years, they remain one of India’s most trusted investment options.

If you can afford to take risk and have already built an emergency fund, it’s worth considering moving beyond FDs and exploring other options. That’s exactly what India’s household savings trend shows us. While FDs are still loved, younger investors with easy access to digital platforms are increasingly taking risk and investing in other financial assets like mutual funds, gold ETFs, and stocks.

I’d Love to Hear Your Story;

For my family, high FD interest rates provided financial stability during one of the most challenging phases of our lives.

What about you? Do you remember the highest FD interest rate you or your parents ever received? Was there a special reason your family relied on Fixed Deposits?

Share your memories in the comments. It’s always fascinating to see how personal finance connects with our life stories across different generations.

Continue reading:

- What is CRR, SLR, Repo Rate & Reverse Repo Rate?

- RBI cuts Repo rate : Impact on your HOME LOAN

- What are the best Risk-free, Safe & Tax-free Investment Options?

(Post first published on : 26-June-2026)

Join our channels