Many people in India still believe that filing an Income Tax Return (ITR) is necessary only if their income crosses the basic exemption limit. But that’s not entirely true anymore!

Under the latest rules for Assessment Year 2026–27, there are several cases where you must file an ITR—even if your income is below the taxable limit or you don’t owe any tax.

Let’s understand these situations in a simple and practical way.

Basic Exemption Limits for FY 2025–26:

Before looking at the “mandatory” scenarios, note the updated basic exemption limits:

- New Tax Regime: ₹4,00,000

- Old Tax Regime: ₹2,50,000 (for individuals below 60 years)

Even if your income falls below these limits, there are certain conditions under which filing an ITR still becomes mandatory.

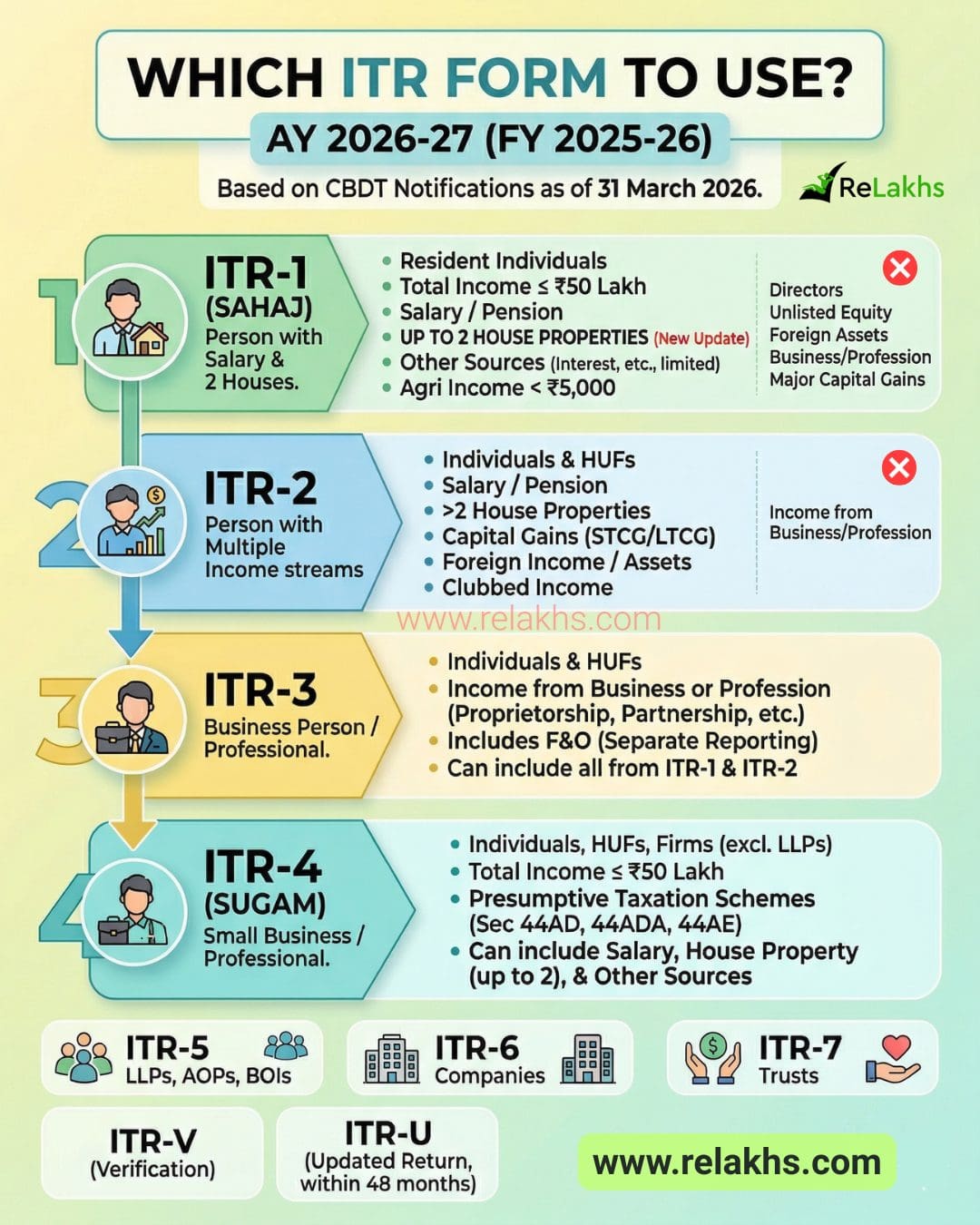

Before understanding mandatory filing scenarios, it’s important to know which ITR form applies to you. Here’s a quick visual guide based on latest CBDT rules (March 2026).

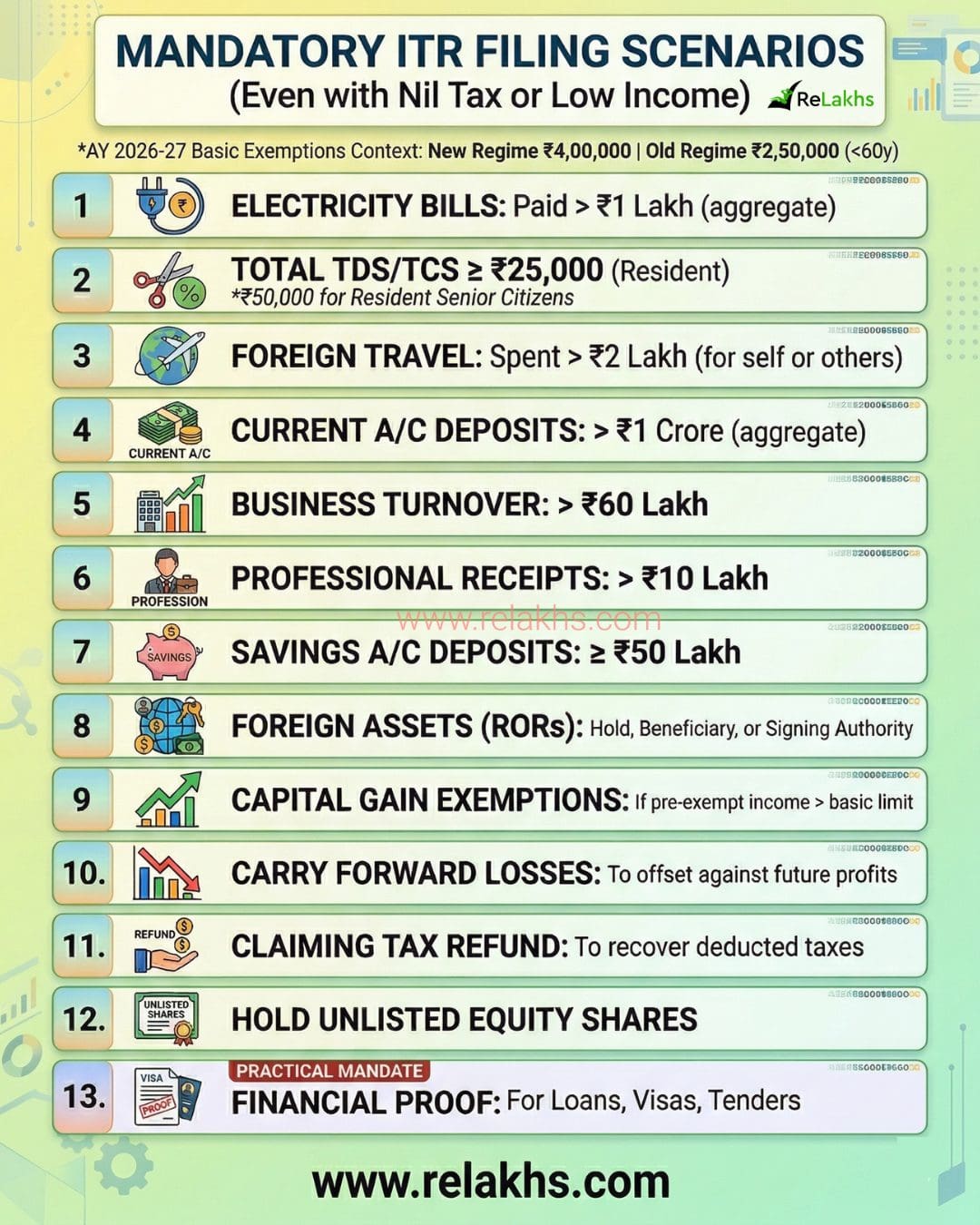

ITR Filing AY 2026-27: Mandatory Even with Nil Tax

In the world of tax compliance, “No Tax” doesn’t always mean “No ITR.” Here are the mandatory scenarios where you must file an Income Tax Return for AY 2026-27, regardless of your income level.

1-High Electricity Consumption

If you’ve spent more than ₹1 lakh on electricity bills during the financial year, filing your ITR becomes mandatory. The Income Tax Department keeps track of such high-value transactions through reports submitted by electricity providers.

2-TDS/TCS Deducted Above the Limit

If the total TDS or TCS deducted during the financial year is ₹25,000 or more (₹50,000 for senior citizens), you’re required to file your ITR. Even if your overall income is below the taxable limit, once tax has been deducted, ITR filing becomes mandatory.

3-Foreign Travel Expenses

If you (or someone on your behalf) spend ₹2 lakh or more on foreign travel in a financial year, it’s mandatory to file your ITR. This includes expenses for personal trips, family holidays, or any other international travel.

4-High Deposits in Current Account

If total deposits in your current account exceed ₹1 crore during the financial year, filing an ITR is mandatory. This applies even if the funds are from business receipts or internal transfers.

5-Business Turnover Above ₹60 Lakh

If your business turnover crosses ₹60 lakh, you must file your ITR — even if your actual profits are low or you’ve declared a loss. This ensures your income and business activity are properly reported to the department

6-Professional Receipts Above ₹10 Lakh

For professionals like freelancers, doctors, consultants, or designers, if gross receipts exceed ₹10 lakh, ITR filing becomes compulsory. The rule applies regardless of your actual taxable income.

7-Large Deposits in Savings Account

If deposits in one or more of your savings accounts total ₹50 lakh or more during the year, you’re required to file your ITR. The Income Tax Department uses such transactions to track potential undeclared income.

Related Article : New PAN Rules from April 2026: Limits & Impact

8-Holding Foreign Assets (ROR Status)?

If you’re a Resident and Ordinarily Resident (ROR) in India and you either own foreign assets, or are a beneficiary or signatory to any foreign account, filing your ITR is mandatory—no matter what your income level is. This rule helps ensure transparency in reporting overseas assets.

9-Claiming Capital Gains Exemption?

If you’re claiming exemptions under sections like Section 54 or Section 54F (for reinvestment of capital gains), you must file your ITR if your income before claiming exemption exceeds the basic exemption limit. The ITR is necessary to report both the capital gain and the corresponding exemption.

10-Carry Forward of Losses

Planning to carry forward a loss—say a capital loss or business loss—to future years? You’ll need to file your return within the due date to do so. Missing the deadline means you lose the right to set off those losses later.

11-Claiming a Tax Refund?

If you’ve had TDS or TCS deducted during the year and want to claim a refund, filing your ITR is mandatory. Without filing, the refund cannot be processed by the Income Tax Department.

12-Holding Unlisted Equity Shares?

If you hold unlisted equity shares—for example, shares in a private limited company—at any time during the financial year, you are required to file your ITR. The rule applies even if you haven’t earned any income from those shares.

13-For Financial Proof (Practical Requirement)

Even when you’re not legally required to file, having an ITR often becomes practically essential for:

- Loan approvals

- Visa applications

- Government or business tenders

So, filing your ITR regularly helps you stay compliant and financially credible.

Key Takeaways & Final Thoughts

Filing your Income Tax Return (ITR) is no longer just about taxable income—it’s about financial transparency and compliance. The government now closely tracks high‑value transactions, so even if your income is below the taxable limit, you may still be required to file.

Non‑filing in such cases could invite notices, penalties, or scrutiny—something every taxpayer should avoid.

Filing your ITR is not only a legal necessity but also a smart financial habit. It builds your credibility, maintains financial discipline, and ensures your records are clean.

If you fall under any of the above situations, don’t skip filing your ITR for AY 2026‑27. When in doubt, it’s always better to file your return voluntarily than risk non‑compliance later.

Continue reading:

- Income Tax Deductions FY 2026-27: Complete Guide to Old vs New Tax Regime

- Latest TDS Rates Tax Year 2026-27 – Complete Chart

- New Income Tax Rules 2026 | 10 Key Changes Explained

(Post first published on : 02-April-2026)

Join our channels