With healthcare expenses in India increasing year after year, many families find their basic health insurance cover insufficient. Top-Up and Super Top-Up health insurance plans offer an affordable way to bridge this gap.

At first glance, Top-Up and Super Top-Up health insurance plans appear almost identical. Both promise a large sum insured at a relatively low premium, which makes them look like smart and affordable upgrades to a basic mediclaim policy.

However, the real difference emerges at the time of hospitalisation and claim settlement. The way these two plans apply deductibles and pay claims is very different, and this difference can significantly impact how much you pay from your own pocket. To make this easy to understand, let’s break it down using a simple, illustration-based explanation.

Before comparing the two, it’s important to understand deductible.

What Is a Deductible?

A deductible is the amount you must pay from your own pocket before the Top-Up or Super Top-Up plan starts paying. This deductible is usually equal to;

- Your existing base health insurance cover;

- This existing cover could be your corporate group mediclaim provided by your employer, an individual health insurance policy, or a family floater plan.

- Alternatively, an amount you are comfortable self-funding (from your own pocket).

In simple terms, the Top-Up or Super Top-Up policy does not cover any expenses until your hospital bills cross this fixed deductible amount.

You can think of this just like topping up your mobile balance. Your regular mobile plan gives you a base balance or data limit. Once that is fully used, the top-up recharge kicks in and gives you additional balance. Similarly, your basic health insurance cover (or your own out-of-pocket payment) pays first, and only after that limit is exhausted does the Top-Up or Super Top-Up policy come into action.

Difference between Top-up & Super Top-up Health Insurance Plans

While Top-Up and Super Top-Up plans are often discussed together, the real difference lies in how they handle deductibles and claims. To understand this clearly, it helps to look at each plan individually. Let’s start by understanding how a Top-Up health insurance plan works.

How a Top-Up Health Insurance Plan Works

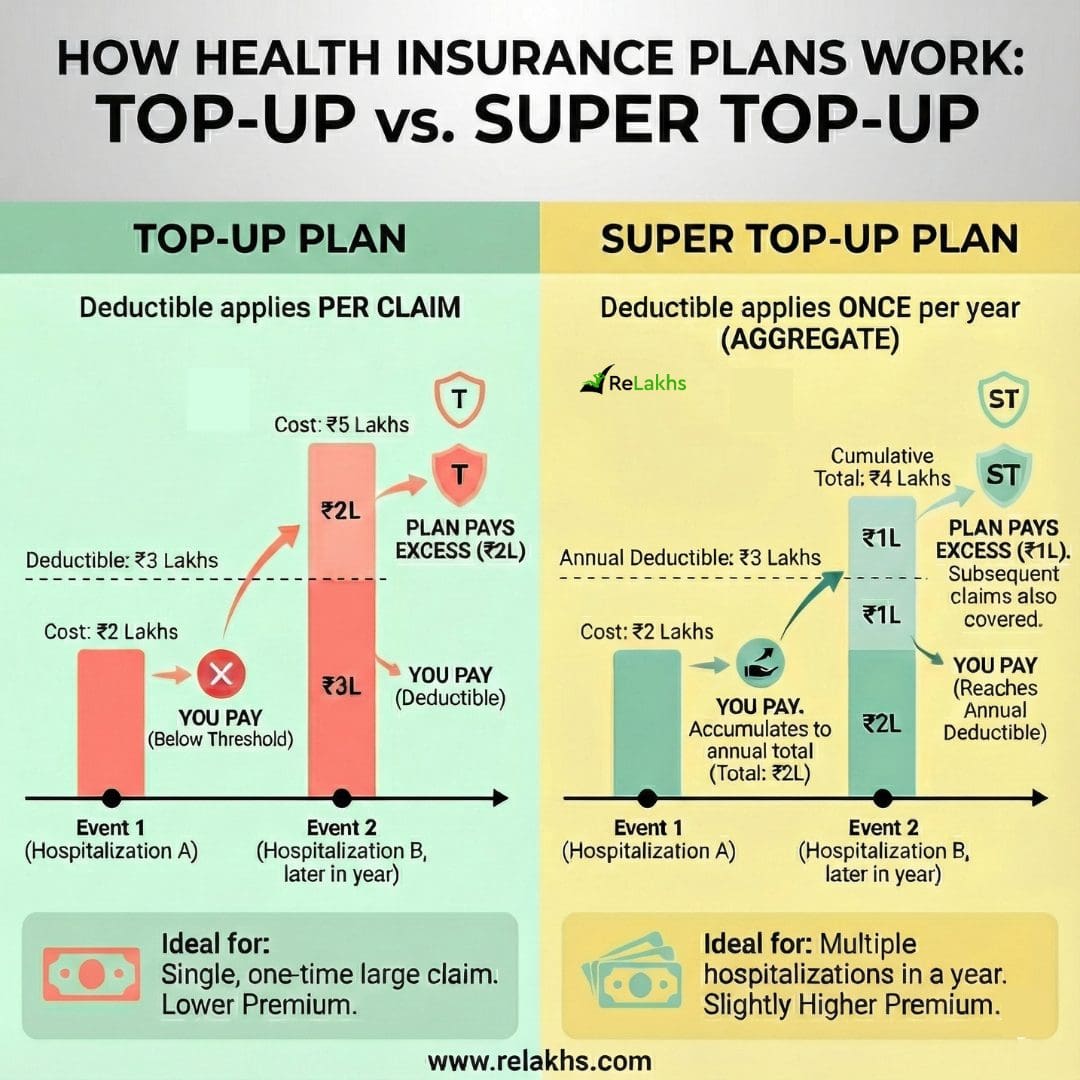

A Top-Up health insurance plan works on a per-claim basis, which means the deductible is applied separately to each hospitalisation. In simple terms, every time you are admitted to a hospital, the deductible limit starts fresh. The Top-Up policy will pay only if the bill for that single hospital stay crosses the deductible amount.

To understand this better, let’s consider an example.

Example (as shown in the illustration)

- Deductible: ₹3 lakhs

- Event 1 hospital bill: ₹2 lakhs

- Below deductible → You pay or your existing base plan pays ₹2 lakhs

- Event 2 hospital bill (later in the year): ₹5 lakhs

- You pay deductible: ₹3 lakhs

- Top-Up plan pays: ₹2 lakhs

To understand this even better — Suppose you have a Top-Up plan with a deductible of ₹3 lakhs. If you are hospitalised for the first time in a year and the hospital bill comes to ₹2 lakhs, the entire amount is below the deductible. In this case, you will have to pay the full ₹2 lakhs yourself, either from your base health insurance policy or from your own pocket. The Top-Up plan will not pay anything for this claim.

Now, assume you are hospitalised again later in the same year, and this time the bill is ₹5 lakhs. Here, the deductible of ₹3 lakhs is first adjusted. After this, the remaining ₹2 lakhs is covered by the Top-Up plan. Even though your total hospital expenses for the year add up to ₹7 lakhs, the Top-Up policy looks at each claim separately, not the total expenses across the year.

Because of this structure, Top-Up plans are best suited for situations where there is one large hospitalisation in a year, such as a major surgery or a serious accident. They are usually available at a lower premium compared to Super Top-Up plans and can work well as a backup cover for catastrophic or high-cost medical events, rather than for multiple or recurring hospitalisations.

When Top-Up Works Best

- Single, large hospitalization

- Lower premium requirement

- Backup for catastrophic medical events

How a Super Top-Up Health Insurance Plan Works?

A Super Top-Up health insurance plan works on an aggregate basis for the entire policy year. Unlike a regular Top-Up plan, the deductible is applied only once in a year, not separately for each hospitalisation. This means all your hospital bills during the year are added together, and the Super Top-Up plan starts paying once the total expenses cross the deductible amount.

To understand this better, let’s consider an example.

Example (as shown in the illustration)

- Annual deductible: ₹3 lakhs

- Event 1 hospital bill: ₹2 lakhs

- You pay ₹2 lakhs (accumulates, like carry forward)

- Event 2 hospital bill: ₹2 lakhs

- Cumulative expenses = ₹4 lakhs

- Deductible crossed by ₹1 lakh

- Super Top-Up plan pays ₹1 lakh

To understand this even better — Assume you have a Super Top-Up plan with an annual deductible of ₹3 lakhs. If your first hospitalisation in the year results in a bill of ₹2 lakhs, you will pay this amount using your base health insurance policy or from your own pocket. This ₹2 lakhs is counted towards the deductible but does not yet cross the limit, so the Super Top-Up plan does not pay anything at this stage.

Now, suppose you are hospitalised again later in the same year and incur another bill of ₹2 lakhs. Your total hospital expenses for the year now add up to ₹4 lakhs. Since the deductible of ₹3 lakhs has been crossed by ₹1 lakh, the Super Top-Up plan will pay this excess amount of ₹1 lakh. Once the deductible is exhausted, any further hospitalisation expenses during the same policy year are covered by the Super Top-Up plan, even if each individual bill is small.

Because of this cumulative approach, Super Top-Up plans are especially useful for people who may face multiple hospitalisations in a year, such as those with chronic illnesses, recurring treatments, or families with higher medical needs. Although the premium is slightly higher than a regular Top-Up plan, Super Top-Up policies offer far better real-world protection and are generally the more practical choice for most individuals and families.

When Super Top-Up Works Best

- Multiple hospitalizations in a year

- Chronic conditions or recurring treatments

- Better real-world protection

| Feature | Top-Up Health Insurance | Super Top-Up Health Insurance |

|---|---|---|

| How deductible applies | Deductible applies to each individual claim | Deductible applies once per policy year on total expenses |

| Claim evaluation | Each hospitalisation is treated separately | All hospital bills in a year are added together |

| Benefit for multiple claims | Limited benefit if there are multiple hospitalisations | Very effective for multiple hospitalisations |

| Premium | Lower premium | Slightly higher than Top-Up |

| Real-world usefulness | Moderate | High |

| Best suited for | One large hospitalisation in a year | Multiple or recurring medical expenses |

| Ideal users | Budget-conscious buyers with low claim expectation | Families, senior citizens, chronic conditions |

How much do Top-up or Super Top-up Health Insurance plans cost?

Here’s a rough estimate table of health insurance premiums in India from a popular private insurer and general pricing illustrations for 30-year-old families (2 adults & 2 kids). These figures are ballpark quotes will vary by age, health history, city, and deductible chosen.

| Policy Type | Coverage (Sum Insured) | Approx Annual Premium (₹) (2A + 2C) |

|---|---|---|

| Family Floater (Base/deductible) | ₹5 lakh | ~₹18,000/year |

| Top-Up Plan | ₹15 lakh above ₹5 lakh deductible | ~₹5,000–₹6,000 |

| Super Top-Up Plan | ₹45 lakh above ₹5 lakh deductible | ~₹16,000 |

To sump it up;

- Base family floater gives primary coverage — it pays from day one up to the sum insured.

- Top-Up adds extra high-value cover above a deductible per claim.

- Super Top-Up adds extra cover above a deductible aggregated yearly — usually better if you expect multiple claims.

With rising hospital costs in India, relying only on a basic mediclaim or employer-provided cover can be risky. Top-Up and Super Top-Up plans are simple, affordable tools to bridge this gap — provided they are chosen correctly. Take a fresh look at your family’s health insurance coverage and upgrade smartly, not expensively.

Continue reading:

- All LIC Plans Returns Analysis 2026: How Much Do LIC Policies Really Return?

- Latest Health Insurance Incurred Claim Ratio 2025 | Top Health Insurance Companies List

(Post first published on : 16-Jan-2026)

Join our channels