‘Roti, Kapda aur Makan‘ ( food, clothes and shelter) are basic requirements for an individual to survive. It is a known fact that most of us would like to own a home. Owning a home is one of the cherished dreams for many of us.

But due to high land prices and high cost of construction, an average Indian always feels short of funds for his dream home when he ventures into the property market. So, home loan is the only preferred option for a majority of home buyers.

The eligibility to get a home loan is mostly dependent on the income levels. So, if your income is very less (salaried or self-employed), it is very tough to get a home loan from a lending institution or a bank.

There is no need to mention separately about families falling under LIG (Low income group) or EWS (Economically Weaker Section). They just cant afford to buy a home.

To ensure that families (who live in urban areas) get a affordable housing solution, the central govt has launched a scheme called Pradhan Mantri Awas Yojana (PMAY – Urban) in May, 2015.

Objectives of Pradhan Mantri Awas Yojana (Urban)

The main objectives of PMAY Sc heme are;

- Rehabilitation of existing slum dwellers

- Promotion of ‘Affordable Housing’ for weaker section through credit linked subsidy (Home loan subsidy)

- Affordable housing through public-private partnerships

- Subsidy for beneficiary-led individual house construction or house enhancement or renovation

PMAY – Features & Eligibility rules

Below are the eligibility rules and key features of the scheme;

- Who can apply for Pradhan Mantri Awas Yojana scheme? – A beneficiary under PMAY has been defined as:

- A family comprising of husband, wife and unmarried children

- Beneficiary should not own a pucca house either in their name or in the name of any member of their family in any part of India to receive central assistance under the Mission &

- Meeting income criteria defined under the scheme.

- What are the income norms (criteria)? Who is eligible for PMAY? – The income norms for EWS / LIG categories are defined as follows:

- EWS households with an annual income up to Rs. 3 Lakh.

- LIG households with an annual income between Rs. 3 Lakh to Rs. 6 Lakh.

- Middle Income Groups (MIG) which fall under the bracket of annual incomes of above Rs 6 lakhs to Rs 18 lakhs are eligible for interest subsidy on housing loans under the new Credit Linked Subsidy Scheme (CLSS). (latest update : 24-March-2017). People whose housing loans have been approved and whose applications are under consideration since January 1, 2017 are eligible for subsidy under MIG – CLSS.

- Eligibility criteria under MIG – I group are : Household income range – Rs 6 Lakh to 12 Lakh, maximum carpet area

90 Sq mt / 970 Sq ftincreased to 120 Sq mtincreased to 160 Sq mt (1,722 sq ft), Maximum loan tenure – 20 years, Maximum interest subsidy – Rs 2.35 Lakh (4%). (Updated on 13-June-2018) - Eligibility criteria under MIG – II group are : Household income range – Rs 12 Lakh to 18 Lakh, maximum carpet area

110 Sq mt / 1190 Sq ftnowhas been increased to 150 sq mthas been increased to 200 sq mt (2,153 sq ft), Maximum loan tenure – 20 years, Maximum interest subsidy – Rs 2.3 Lakh (3%). (Updated on 13-June-2018) - Latest Update (22-Sep-2017) :

Interest subsidy scheme on home loans under MIG category has been extended from 31st Dec, 2017 to 31st March, 2019. - Latest Update (02-Jan-2019) : Interest subsidy scheme on home loans under MIG category has been extended from 31st Dec, 2019 to 31st March, 2020.

- Eligibility criteria under MIG – I group are : Household income range – Rs 6 Lakh to 12 Lakh, maximum carpet area

- What is Credit Linked Subsidy Scheme? – One of the main aims of PMAY is to provide subsidy on home loans taken under this scheme. Below are few details about the subsidy scheme;

- If the loan amount is less than Rs 6 Lakh then interest rate on loan is charged at 6.5% to the beneficiary. To avail this subsidy, the loan tenure has to be less than or equal to 15 years.

- If the loan amount is more than Rs 6 Lakh, the interest rate of 6.5% is applicable on loan amount of up to Rs 6 Lakh and the remaining balance loan amount will be subject to normal prevailing market rates. For example : If you apply for home loan under PMAY scheme for Rs 10 Lakh, up to Rs 6 Lakh the interest rate is charged at 6.5% and the balance Rs 4 Lakh is charged at prevailing interest rates by your bank or lending institution.

- If home loan amount is up to Rs.9 lakhs then the beneficiary will get home loan interest subvention / rebate of 4% per annum. This means if the prevailing interest rate is 10% then the home loan will be provided at 6% interest rate. (updated on 02-Jan-2017)

- Similarly, if the home loan amount taken in 2017 is up to Rs.12 lakhs then the beneficiary will get home loan interest subvention of 3% per annum. This means if the prevailing interest rate is 10% then the home loan will be provided at 7% interest rate.

- In villages, those wanting to build or expand their homes will get loans of up to 2 lakh, with a 3% interest relief.

- How much subsidy will I get? –

- It would be computed at a rate of interest of 6.5% p.a on a maximum loan amount of Rs. 6 Lakh or the loan amount whichever is lower, for 15 years tenure with discounting rate of 9%.

- For 6 Lakh the interest subsidy comes to around Rs. 2,20,000.

- Hence an upfront subsidy of Rs. 2,20,000 would be claimed by your bank from NHB (National Housing Bank) and the same would be adjusted against the outstanding amount in your Loan Account.

- The loan outstanding would reduce and result in lower EMI of approximately Rs. 2,000 for you. (Kindly click on the below image to calculate your subsidy amount.)

- Illustration – If you avail a loan for Rs. 8 Lakh then the maximum subsidy works out to Rs. 2,20,000. The amount Rs. 2,20,000 would be reduced upfront from your loan account (i.e., the loan would reduce to Rs. 5,80,000) and you would pay EMIs on the reduced amount of Rs. 5,80,000 only. (Kindly note that 6.5% is the rate of interest up to Rs 6 Lakh & prevailing rate is charged for the remaining Rs 2 Lakh.)

- Do I have to give any additional documents to avail this subsidy? – No, there is no additional documents except a Declaration of not owning a pucca house. If you do not have any income proof then you are required require to submit an Affidavit.

- What is the rate of interest on home loan under PMAY? – As mentioned above, the rate of interest is 6.5% for the loans up to Rs 6 Lakh. Any amount which is over and above this limit will be subject to normal market interest rates.

- Should I buy a house which is provided under PMAY only? – The Govt is planning to build around 2 crores of affordable houses by 2022 in a phased manner. You can apply for a house which is provided under this scheme (or) you can buy a house from a project (pvt) where 30% of affordable houses in the project are ear-marked for EWS category (or) you can build your own house or renovate the existing house.

- What is the maximum loan amount that I can apply? – As such, there is no loan amount limit under this category of loans.

- I have one own house. Can I apply for second house under PMAY? – No, you can not apply for this scheme.

Latest News (25-Jan-2018) : GST for homes purchased under the Credit Linked Subsidy Scheme (CLSS) would be 8% w.e.f 25th January, 2018. For under-construction homes that form a part of CLSS will now be charged GST at 8 percent instead of 12 percent, a cut of 4 percent. However, people who are not eligible for CLSS will continue to pay higher GST.

The concessional rate of GST of 12 percent (effective rate of 8 percent after deducting one-third of the amount charged for the house towards the cost of land) will henceforth (from January 25) be applicable for houses constructed or acquired under the CLSS for Economically Weaker Sections (EWS) / Lower Income Group (LIG) / Middle Income Group-1 (MlG-1) / Middle Income Group-2 (MlG-2) under the Housing for All (Urban) Mission/Pradhan Mantri Awas Yojana (PMAY Urban).

How to apply for PMAY Scheme? How to get Home Loan Subsidy under Awas Yojana?

If you meet the above income norms of EWS / LIG (or) if you are a slum dweller, you can apply through the following modes;

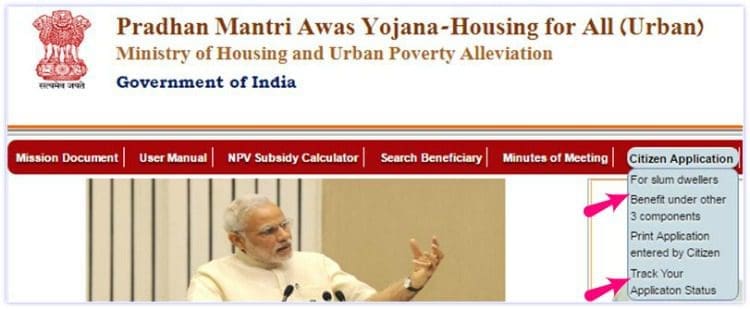

- Govt’s PMAY portal : You can submit online application to buy a house provided under PMAY Scheme in your locality. Below is the procedure;

- Kindly visit PMAY, Govt Portal.

- Click on ‘Citizen Application’.

- Click on ‘Slum dweller’ and submit Format-A application.

- If you belong to EWS or LIG category then click on ‘benefit under 3 components’ and submit Format-B application.

- Kindly save the reference number or application number for future use.

- You can track your application status by clicking on ‘track your application status’.

- You can also search for your name, whether it is in the beneficiary list or not.

- Kindly visit PMAY, Govt Portal.

- CSC Centre : You can also apply for a house under PMAY at any of your nearest CSC centre (Common Services Centers). Click here to locate a CSC centre. (This facility has been launched on 02-Nov-2016)

- State Land Nodal Agencies : Another option is to apply through any ‘Nodal Agency’ designated by the State Governments for implementing the Mission.

How to apply for Home loan Subsidy under PMAY? (Credit linked Subsidy Scheme)

Let’s say you meet the income norms and other eligibility criteria, have applied for a house under PMAY, and you have been allotted a house. What if you do not have the money to buy the house?

(The States/Union Territories would decide on an upper ceiling on the sale price of EWS houses in rupees per square meter of carpet area in such projects with an objective to make them affordable and accessible to the intended beneficiaries.)

Under such a scenario, you can apply for a home loan under Pradhan Mantri Awas Yojana Scheme and can get the subsidy. You can also apply for a home loan to construct a new house or renovate your existing house.

You can apply for a loan through any Scheduled Commercial Banks (like SBI, ICICI Bank, Canara Bank etc), Housing Finance Companies, Regional Rural Banks (RRBs), State Cooperative Banks, Urban Cooperative Banks or any other institutions as may be identified by the Ministry.

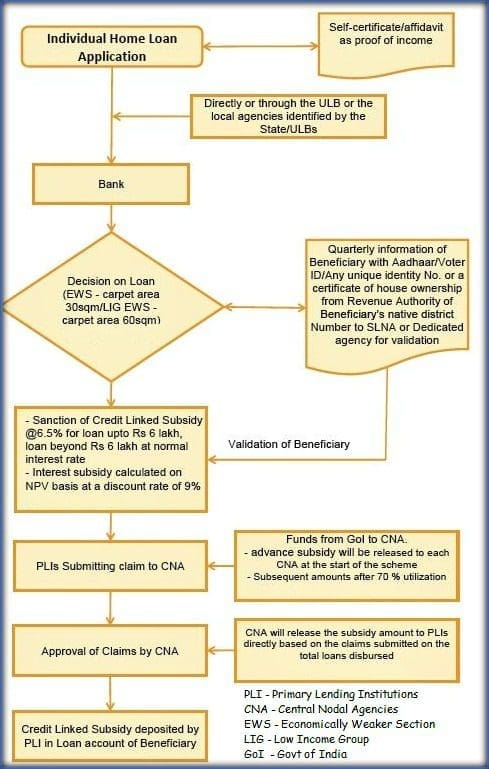

Below is the detailed flow-chart on how the home loan application under PMAY is processed and how the subsidy amount is credited to your loan account (beneficiary account).

(Kindly note that you can avail the subsidy of Rs 1.5 lakh for construction of new houses under the mission. You have to approach your Urban Local Body to avail the subsidy. Families belonging to EWS categories are eligible for this assistance.)

My Opinion : If the houses provided under this scheme are of good quality with the basic amenities, and if the subsidy amounts are claimed by the deserving families then Pradhan Mantri Awas Yojana can be a successful scheme and the mission of ‘housing for all’ in urban areas can be accomplished in the next few years.

Latest news (31-December-2016) : PM Narendra Modi announces new Housing Schemes with rebates/discounts on Home Loan interest rates under Pradhan Mantri Awas Yojana (PMAY). Two new middle income categories have been created under the Pradhan Mantri Awaas Yojana in urban areas. Home loans of up to 9 lakhs, will get a 4% interest benefit. For home loans of up to 12 lakhs, an interest rate waiver of 3% will be provided. In villages, those wanting to build or expand their homes will get loans of up to 2 lakh, with a 3% interest relief.

Latest update (22-June-2017) : EPFO (Employees Provident Fund Org) & HUDCO (Housing & Urban Development Corp) plan to tie up for providing housing subsidy to members of EPF Scheme, under PMAY. As per the recent notification, EPFO now allows its subscribers who want to buy a house property from Housing Societies / Agencies to withdraw up to 90% of their EPF accumulations to buy homes.

(Reference & source : Ministry of Housing & Urban Poverty Alleviation, Government of India)

(Image courtesy of atibodyphoto at FreeDigitalPhotos.net) (Post published on : 03-November-2016)

Join our channels

it is a very good nformation

Hi,

I have applied PMAY after 2 years and while verification they found we are not staying on same home so it will be one of the reason to deny PMAY subsidy if no then how can i re-apply or escalate that issue.

Dear Sameer,

You may submit your grievance to ;

grievance-pmay@gov.in

NHB: 1800-11-3377

1800-11-3388

HUDCO: 1800-11-6163

I purchased home at August 2019 by taking loan from LIC hfl with PMAY included in it. They are not providing the assessment ID to check my PMAY status, Is there any other way to get the assessment ID

I have applied loan on 31st Aug 2018 also applied for pmay. But IIFL says your file already sent to NHB on 21st march 2019, But NHB not releasing payment after march due to election. is this correct information?

Dear PRAVEEN,

I am not very sure on this!

The Govt has already been formed. Suggest you to escalate this issue at IIFL or with NHB.

After all details entered and press save button there is error records not saved ,why this happened I checked one again very carefully still showing same error

Sir, I tried applying for PMAY by clicking first on ‘citizen assessment ‘ then ‘benefit under other 3 components’.

I got a page saying enter Aadhar number and name printed as on aadhar ,after I entered the correct Aadhar no. Without space and name correctly it was showing the same new page even after many trials (though my Aadhar no. Is correct). Sir, can you please suggest me how can I proceed further?

Dear Amit,

The same has been reported by few other blog readers as well..looks like there is a technical glitch with the portal..

Unable to check adhar even after entering correct adhar number and name as on Aadhar.. unable to reach toll free helpline.. pls suggest how to go about further..

Dear Srikanth,

I have purchased a House with Homeloan from HDFC.In this my brother is co-owner and we both are married.But neither we nor our wife own a property in any part of India.This is the first property we own.

Are we eligible for PMAY?

Dear Dwivedi,

Kindly check other eligibility criteria as well..Suggest you to kindly talk to your banker on this ..

I am fulfilling other criteria under MIG II option,but my banker is telling that if two brothers are coowner we are not eligible.But in other bank its showing eligible.

Dear DWIVEDI,

The eligibility criteria is same across all the banks.

Not sure, why your banker is denying the subsidy..

May be they are referring to ;

A beneficiary under PMAY has been defined as:

A family comprising of husband, wife and unmarried children..

Yes,they are referring to this point only.Is there anywhere I can get a note or something which states that siblings can also apply.

Dear DWIVEDI,

You may refer to the below links..

Link – 1

Link – 2

Hi Dwivedi,

I also purchased a house with co-owner as my brother. I am looking for PMAY eligibility. Did you apply for PMAY scheme. Please let me know the process. Your help will be very much appreciated.

Thank you.

Hi Sreekanth,

My mother has applied for pmay housing for all scheme and a week back we got a message stating that a flat has been allotted to us

Can u pleaase let us know how to proceed further and how to know the status as we are not sure about the assessment id.

Please help us.

Thanks,

Yamini

Dear Radha,

You may kindly check on this by visiting PMAY portal..

Hello Srikanth Reddy…i have seen many people who belongs to a wealthy family but still applying to get the PMAY URBAN HOUSING scheme. So i would like to know that is it possible to get the scheme by a government employee wife or husband who have already have a pucca or brick houses…if no where or how should i complain…im asking this becos our local MLA and local agents are not complying the eligibility of the scheme…thanks.

Dear Jenpu,

You may try submitting your grievance here through this link…

Hi Srikanth,

i have applied for loan amount 30 lakhs with Axis Bank.

Loan applied on my name & co applicant as Father ( Axis bank says co applicant is mandatory)

i falls under An unmarried independent person (female /male earning person) may be considered as a separate household

but my father name is added in loan account.

Do i eligible for PMAY ?

Salary structure is MIG 1 below 12 lakhs

Dear Muthu,

As your father is also a co-borrower, you may suggest him to apply for the subsidy. Kindly check on this with your lender..???

i applied for subsidy but got rejected saying that family reason not satisfied.

My home registered only on my name.

however in MIG 1 family definition says “A family comprising of husband, wife and unmarried children”

Axis bank guys are also not clear & day by day i am getting different information.

Dear Muthu,

Yes, eligibility criteria says so..

In case, your property is not co-owned by your father then your loan account may not be eligible for subsidy..

Will I be eligible for the PMAY scheme for my new housing loan if my father as a co-applicant for my home loan? i and my wife owns 100% of the new property (for which home loan applied), and my father just a co-applicant(my father already a owner of hosue).

Dear Pankaj,

One of the eligibility conditions is – “Beneficiary should not own a pucca house either in their name or in the name of any member of their family in any part of India to receive central assistance under the Mission.”

So, mostly you may not be eligible to apply for home loan under this scheme.

Kindly cross-check with your Lender/banker..

Hello,

I tried applying for pmay by clicking first on ‘citizen assessment ‘ then ‘benefit under other 3 components’.

I got a page saying enter Aadhar number and name printed as on aadhar ,after I entered the correct Aadhar no. Without space and name it was showing the same new page even after many trials (though my Aadhar no. Is correct).Can anyone please suggest me how can I proceed further?

Dear Kumar,

Kindly contact them through Toll free numbers :

CLSS Toll-Free Helpline Numbers

NHB: 1800-11-3377

1800-11-3388

HUDCO: 1800-11-6163

1.Is it mandatory to apply for PMAY via the lender bank at the time of applying for loan?

2. I have applied for loan 2 days back so can I apply for PMAY via that government website for the same?

3. The account information in website, is that the salaried account or loan account? If am applying personally how can I get the loan account number as loan approval is still under process?

Dear Deepak,

1 – It is not mandatory. But, if the loan applicant is eligible for PMAY then why not to apply and take the benefit of available Subsidy.

2 & 3 – I believe you can. You may also check with your Banker/Lender.

Hi Sreekanth,

Have few queries related to CIDCO Lottery 2018

1.Is it compulsory to have PMAY registration ?(No where mentioned its compulsion

2.I tried to register under PMAY on website, but after entering Aadhar no and Name nothing appears on the screen,

how can I proceed to register myself under PMAY?

3.As of now, for applying to lottery nowhere mentioned any assessment id for PMAY registered, can I proceed with the same and register under PMAY later?

It would be immense help if you can address above query.

Thanks.

Dear babalalex,

1 – I believe that it is not compulsory.

2 & 3 – The same has been reported by other blog readers as well. You may dial to these helpline numbers..

Hello,

I tried applying for pmay by clicking first on ‘citizen assessment ‘ then ‘benefit under other 3 components’.

I got a page saying enter Aadhar number without space ,after I entered the correct Aadhar no. Without space it was showing the same new page even after many trials (though my Aadhar no. Is correct).Can anyone please suggest me how can I proceed further?

Hi, Facing same issue. Any solution for this?

If BDA allots a site for me and purchased through loan against the site, will I get the benefits of PMAY?

Dear Nagendra,

Yes, I believe that you can claim the subsidy but provided you meet the eligibility criteria..

Hello, I am engaged and soon to be married (before december 2018). Can I and my fiancee book a house and avail benefits of PMAY?

Dear Nik,

Generally Banks may hesitate to give a joint home-loan to friends (before getting married).

You can apply for a joint-home loan under PMAY (provided you meet the eligibility conditions).

Related article : Joint Home Loan : Eligibility rules & Income Tax Benefits

Sir. I recently bought a under construction 2 bhk flat in Kolkata which is 750 sq ft .I took a loan from sbi and loan was sanctioned on oct 2017 but before sanctioned I know that pmay clss money may received after registration of my flat but my flat registration already done .then I m trying to fill pmay form&SBI pmay form also but I can’t do this. Then what can I do plz help me .my registration held on 5 the June…

Dear Pinky,

I did not get your query..Are you meeting the eligibility requirements?

What is your banker/lender saying?

Yes our income 5.8 lakhs PA .I took a loan from SBI for 19. 35 sanctioned on Nov 2017 & start disburse 1 St instalment of 10 75000 & from Dec 2017 my first emi was start .my second instalment of 8 60000 paid on 5 june2018 .in this case am I eligible for pmay susidy &how it’s proceed…

Dear Pinky .. Kindly check with your banker.

Hi sir ; is pmay eligible for resale apartment?

Dear Venkat ..I believe that PMAY is applicable fore re-sale ones as well..

Hi, I took the loan with LIC HFL and we applied for PMAY while applying the loan. Its been 6 months and I did not get benefited. When I check with regional branch they also doesn’t have the information. Is there any way to get the status?

Dear Ganesh,

You may check the status at PMAY official website. Kindly follow it up with LIC HFL.

Thanks for the info, I have tried to check the status with official website and it is asking to enter assessment ID which I doesn’t have. I checked with LIC HFL guys and they also doesn’t have.

I am not sure whom to approach to get the exact status.

Dear Ganesh,

I believe that LIC HFL has to provide you the required assitance.

In case, they don’t, just let them know that you are going to switch the home loan balance to some other lender, then they may provide you the required support.

Hi sreekanth

I have few questions on this. Any Information on this would be of great help for me.

We have purchased a home.Agreement of sale and Construction aggreement is done and paid 20% of the property value to the seller.

As we are buying from the owners share he is saying that we have to pay 12 percent GST on the Government value for that property. When I showed all the proofs Regarding the slashed GST rates(8%) for applicants under PMAY, he is not accepting and he is demanding 12%.

Unfortunately, we have to pay GST to the flat owner here not to the Govt directly.

Please suggest how to procced further on this.

One more thing is that shall I apply for PMAY just after the aggreement before the flat registration.What could be right time to apply for PMAY?

Regards,

Prasanna

Dear Prasanna,

The right time to apply for PMAY is as soon as you acquire a home loan.

In case, you pay GST, get the property invoice bill with GSTIN from your Seller.

Hi

Acquiring the home means,as soon as the home loan got approved or after the funds got released.

And, if we get the property invoice bill with GSTIN, shall I claim GST returns and get that 4 percent back?

Are there any chances or possibilities to get that extra GST refunded?

Regards,

Prasanna

Dear Prasanna,

You can ask your Lender/Banker to route your home loan application under PMAY scheme itself.

Regarding the refund of GST, i am not sure..you may consult a CA.