For many Indian investors, retirement planning often comes down to two broad approaches: investing through the National Pension System (NPS) or building a portfolio using mutual funds.

Recently, a new category of mutual fund schemes — Life Cycle Funds — has been introduced. These funds aim to simplify retirement investing by automatically adjusting asset allocation as investors age.

At first glance, this concept may sound familiar. That’s because NPS already offers a similar structure through its Auto Choice (Life Cycle) option. This naturally raises a question:

Are mutual fund Life Cycle Funds an alternative to NPS, or are they simply a different wrapper for the same idea?

Related Article : SEBI 2026 Mutual Fund New Rules: What Investors Need to Know

NPS Auto Choice vs Mutual Fund Life Cycle Funds

NPS Auto Choice and mutual fund Life Cycle Funds both use a glide path that reduces equity exposure as investors age. The key difference is that NPS offers tax benefits and lower costs but has withdrawal restrictions, while Life Cycle Funds offer greater flexibility and liquidity. Let’s take a closer look.

What Are Mutual Fund Life Cycle Funds?

Life Cycle Funds automatically adjust your investments based on your age—they’re like target-date funds. The main advantage of this structure is that the investor does not need to manually rebalance the portfolio.

Here’s the simple logic:

- When you’re young: More in stocks for growth potential.

- As retirement nears: Shifts to safer debt for stability.

This automatic shift is called the “glide path.” A simplified example might look like this:

| Age | Equity Allocation | Debt Allocation |

|---|---|---|

| 30 | 80% | 20% |

| 40 | 65% | 35% |

| 50 | 45% | 55% |

| 60 | 20% | 80% |

What Is NPS Auto Choice?

NPS has something called Auto Choice that works just like Life Cycle Funds. It auto-adjusts your mix of stocks, corporate bonds, and government securities based on your age.

NPS offers three main Auto Choice options:

- Aggressive Life Cycle Fund (LC75)

- Moderate Life Cycle Fund (LC50)

- Conservative Life Cycle Fund (LC25)

The number here indicates the maximum equity exposure allowed at age 35. Each one follows a set “glide path” that cuts equity as you near retirement.

Example: NPS Aggressive Life Cycle Fund (LC75)

| Age | Equity (E) | Corporate Debt (C) | Government Securities (G) |

|---|---|---|---|

| 35 | 75% | 10% | 15% |

| 45 | 65% | 15% | 20% |

| 55 | 45% | 20% | 35% |

| 60 | 15% | 10% | 75% |

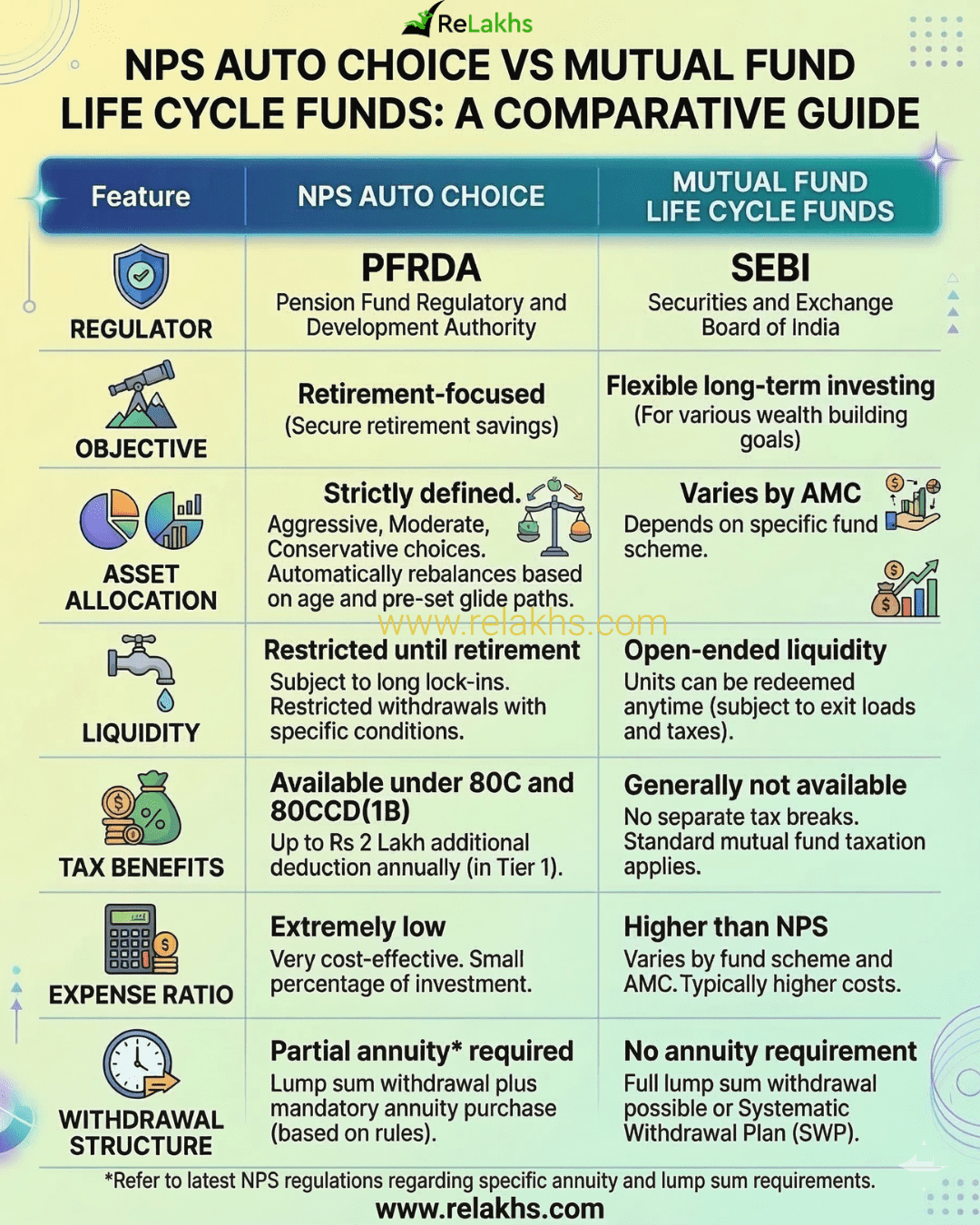

MF Life Cycle Funds vs NPS Auto Choice: A Structural Comparison

Although the underlying concept is similar, the structure, flexibility, and objectives differ significantly.

| Feature | NPS Auto Choice | Mutual Fund Life Cycle Funds |

|---|---|---|

| Regulator | PFRDA | SEBI |

| Objective | Retirement-focused | Flexible long-term investing |

| Asset Allocation | Strictly defined (Aggressive, Moderate, Conservative) | Varies by AMC. |

| Liquidity | Restricted until retirement | Open-ended liquidity |

| Tax benefits | Available under 80C and 80CCD(1B). Upto Rs 2 Lakh | Generally not available |

| Expense ratio | Extremely low | Higher than NPS |

| Withdrawal structure | Partial annuity* required | No annuity requirement |

Asset Allocation: Unlike NPS, each mutual fund house may design its own glide path. Both structures can eliminate behavioral mistakes, but NPS is more rigid while MF funds offer scheme variety.

NPS withdrawal structure at retirement (2026 update) — Private sector & All Citizens: 20% corpus for annuity, 80% tax-free lump sum (small corpus exceptions apply). Government employees: 60% lump sum withdrawal allowed, 40% mandatory annuity purchase.

NPS vs Mutual Fund Life Cycle Funds: Which Is Better for Retirement?

Choose NPS Auto Choice if: You want the lowest possible cost, a disciplined “hands-off” glide path, and you are comfortable with a 40% or 20% annuity to provide a “base” pension.

Choose MF Life Cycle Funds if: You want 100% control over your money at age 60, higher equity exposure in your 40s/50s, and you prefer the flexibility of an SWP (Systematic Withdrawal Plan) over an annuity.

A Contrarian Insight

The real debate may not actually be NPS vs Life Cycle Funds. The bigger question is whether investors really need a product to enforce discipline.

Both NPS Auto Choice and Life Cycle Funds are built on the assumption that investors may struggle with asset allocation and periodic rebalancing. So the product does it automatically through a predefined glide path.

But investors who are comfortable managing their portfolios can achieve something very similar by periodically rebalancing their equity and debt allocation themselves — often with more flexibility.

In that sense, these structures are not entirely new investment strategies. They are behavioural solutions packaged as financial products. For some investors, that structure can be extremely helpful. For others, it may simply add another layer of packaging.

Neither approach is universally better. Ultimately, the right choice depends on how much structure, flexibility, and control you want in your retirement strategy.

Continue reading:

- Best Mutual Funds for 2026: Picking “Consistency Kings” Over Performance

- My Latest Mutual Fund Portfolio 2025-26 | My 16-Year MF Journey & Lessons Learned

(Post first published on : 11-March-2026)

Join our channels

There are new pension schemes based on 100% equity. Kindly do a blog on those.