Big news from RBI! From April 1, 2026, you don’t need just gold for a quick loan—now, your silver jewellery and coins can unlock funds for you too! Till now, only gold loans were widely offered by formal banks and NBFCs (Non-Banking Financial Companies). But with silver prices shooting up and popularity growing, RBI has decided to allow secured lending against silver too.

The RBI has laid down comprehensive guidelines for lending against gold and now silver, which all RBI-regulated lenders must comply with by April 1, 2026.

While the RBI’s framework on ‘loan against silver’ is now notified, the real-world execution, pricing, borrower response, and lenders’ appetite will become clearer only after implementation. The long-term success of silver loans will depend on regulatory clarity, loan performance, and silver’s inherent price volatility.

RBI Guidelines on Loans Against Silver (Effective 1 April 2026)

The Reserve Bank of India (RBI) has issued new regulations called the “Lending Against Gold and Silver Collateral Directions, 2025”, which will allow:

- NBFCs and housing finance companies

- Commercial banks (including small finance banks and regional rural banks)

- Urban & rural co-operative banks

to offer loans against silver jewelry and coins starting April 2026-—but under strict conditions.

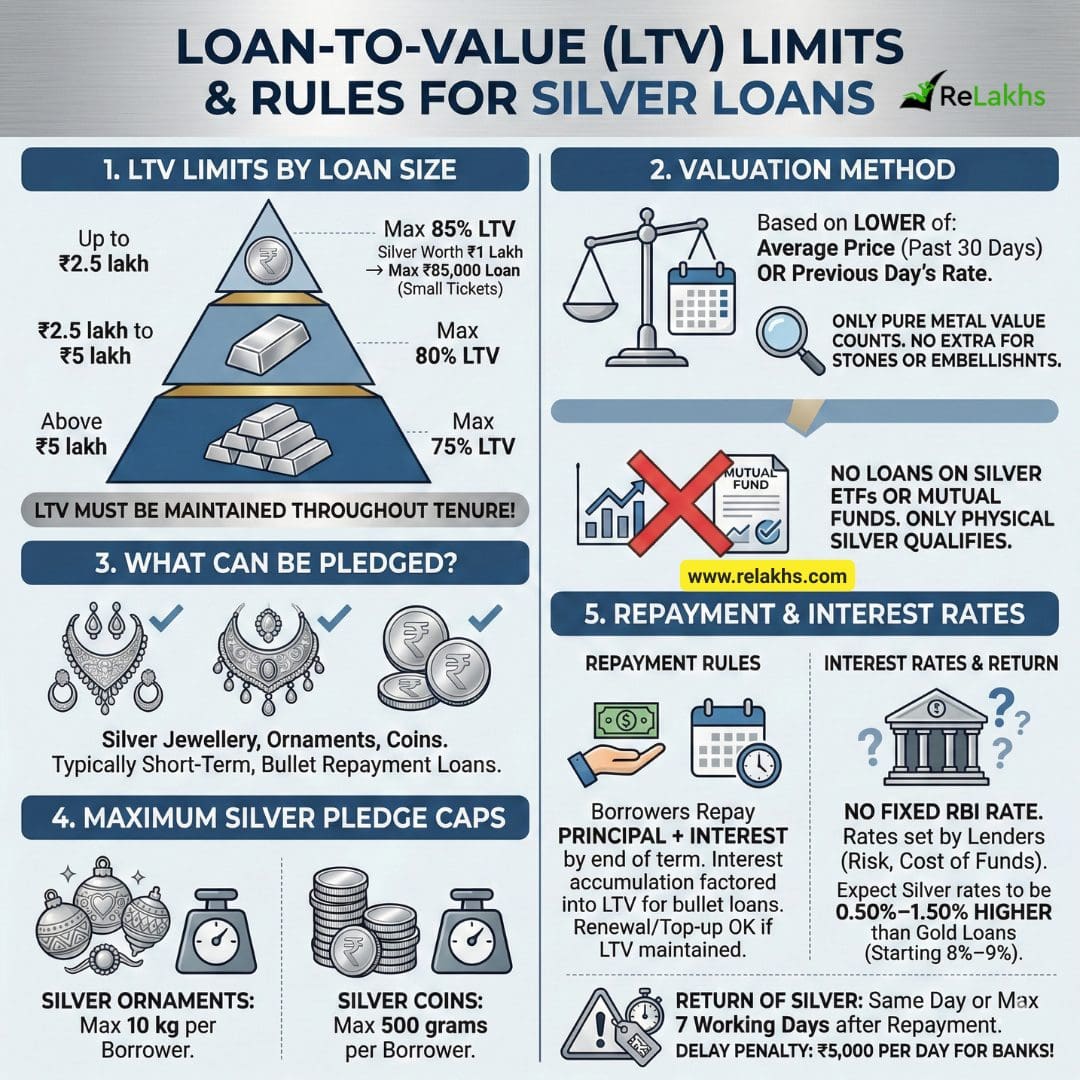

- Loan-to-Value (LTV) Limits: The maximum loan amount depends on the total loan size:

- Up to ₹2.5 lakh loan amount → Maximum 85% LTV. That means, if your silver is worth Rs 1 lakh, you could get up to ₹85,000 as loan for small tickets

- ₹2.5 lakh to ₹5 lakh → Maximum 80% LTV

- Above ₹5 lakh → Maximum 75% LTV

- This LTV must be maintained throughout the loan tenure, not just at sanction time.

- Valuation: : The value is calculated based on the average price of silver over the past 30 days or the previous day’s rate, whichever is lower. Only the pure metal value counts—no extra for stones or embellishments!

- What Can Be Pledged? – Borrowers can pledge:

- Silver jewellery

- Silver ornaments

- Silver coins

- Just like gold loans, these are typically short-term loans, often structured as bullet repayment loans.

- Kindly note that no Loans on Silver ETFs (Exchange Traded funds) or Mutual Funds. Only physical silver jewelry, ornaments, and coins qualify as eligible collateral.

- Maximum Silver You Can Pledge: The RBI has placed clear caps to avoid excessive exposure-

- Silver ornaments: Maximum 10 kilograms per borrower

- Silver coins: Maximum 500 grams per borrower

- Repayment Rules:

- Borrowers must repay both principal and interest by the end of the loan term.

- For bullet repayment loans, interest accumulation is factored into LTV calculations.

- Renewal or top-up loans are allowed only if LTV norms are maintained.

- If you repay the loan, your silver must be returned the same day or maximum within 7 working days—or else, banks pay a penalty of ₹5,000 per day of delay!”

- Interest Rate for Silver Loans: The RBI guidelines (Lending Against Gold and Silver Collateral Directions, 2025) do not specify a fixed interest rate for loans against silver. Instead, interest pricing is left to individual lenders (banks, NBFCs, co-ops), based on their credit policies, risk assessments, cost of funds, and external benchmark frameworks.

- Since gold is more stable, gold loans currently start around 8%–9%. Silver loans will likely carry a risk premium of 0.50% to 1.50% over gold loan rates.

My Take:

India holds far more silver than gold by weight, particularly in rural and semi-urban households. From wedding utensils and temple silver to inherited coins passed down generations, silver has always carried value—but almost no formal liquidity. In rural and semi-urban India, silver is often called the “Poor Man’s Gold.”

In 2025 alone, India imported roughly 6,000 metric tons of silver, accounting for nearly 25% of global demand.

For years, silver owners had only two options during cash crunches– sell the metal outright or borrow informally, often at unfavourable terms. With RBI formally allowing loans against silver, that dormant value finally enters the formal credit economy.

However, this shift may come with limitations;

- Silver’s lower price per gram and higher price volatility naturally restrict loan sizes to low or medium ticket amounts, even when large quantities are pledged.

- Interest rates are unlikely to be cheap.

- Unlike gold, silver purity testing is not yet uniformly standardised across all branches, and in rural areas, conservative or aggressive undervaluation is a real possibility—at least initially.

- The first couple of years of implementation will likely be uneven. Processes will stabilize, pricing will adjust, and lenders will learn from early loan performance.

Borrowers would do well to wait, compare across lenders, and avoid rushing in just because the option now exists. Silver may have entered the formal lending system—but maturity will take time. So, silver in your locker now not only shines, it can support you in emergencies—securely and formally! This move is likely to benefit households and small traders alike.

Continue reading:

(Post first published on : 07-Feb-2026)

Join our channels