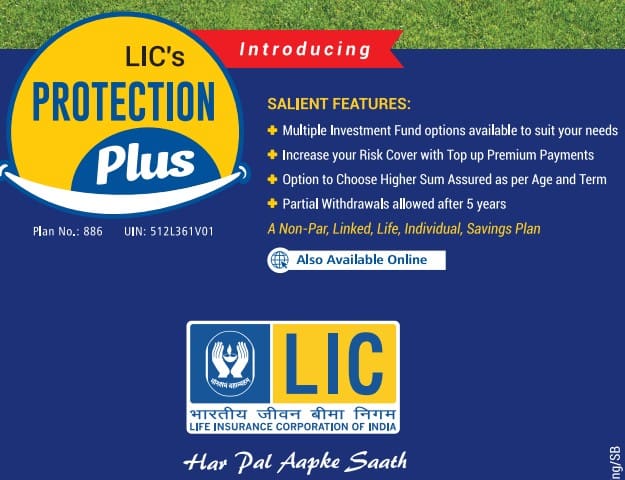

LIC Protection Plus (Plan 886) is a new non-participating ULIP (Unit Linked Insurance Plan) from LIC that combines life cover with market‑linked savings.

LIC’s Protection Plus is a non-par, linked, individual life insurance savings plan, i.e., a ULIP where your premiums are invested in market-linked funds while also providing life cover during the policy term.

This means it is not tied to traditional bonus declarations but invests in a fund (unit-linked), offering both insurance cover and potential fund growth. The plan is available from 3 December 2025 for Indian residents through LIC branches/agents and the LIC website.

What are ULIPs? ULIPs are life insurance policies with the dual purpose of providing an insurance cover as well as earn you a return by investing in equity and/or debt oriented securities. The insurance company floats different kinds of funds, just like the mutual fund house, to gather money from investors. It then invests this pooled money across assets like stocks, bonds etc.,

The key features that are offered by LIC’s Protection plan are; choice of funds, the ability to increase/decrease sum assured, pay top-up premiums, and allow partial withdrawals after a lock-in period

LIC Protection Plus – Features

- Type: Non-par, linked, life, individual, savings plan (ULIP).

- Entry age: Minimum 18 years; maximum 65 years (age restrictions may vary by term/option).

- Policy term: Broadly 10 to 25 years (subject to maximum maturity age)

- Premium payment options: Regular premium

- Limited premium payment (5, 7, 10, 15 years)

- Basic Sum Assured (minimum) : 7 times of annualized premium for entry age below 50 and 5 times annualized premium for entry age 50 or more.

- Flexibility : Policyholders can choose how much premium (subject to minimum) they want to pay. Based on that premium, the Basic Sum Assured (death cover) is determined.

- Optional “Top-Up” Premiums: You’re allowed to make additional (top-up) premium payments beyond the base premium — which gets invested in the fund to increase your maturity benefit. Top-up premiums can be paid at any time during the term of the policy, except during the last 5 policy years, provided the policy is in-force

- Partial withdrawal facility: After 5 years from the start of the policy, partial withdrawals are allowed.

- Maturity Benefit :

- On survival to the maturity date, the policyholder receives the Unit Fund Value as on the date of maturity

- Special feature : Refund of mortality charges (cost of life cover) on survival till the date of maturity

- Investment Fund Options :

- Protection Plus offers multiple ULIP funds with different risk-return profiles, ranging from conservative bond-oriented funds to aggressive equity-linked funds.

- Typical fund buckets include:

- Bond / income-focused fund with low equity exposure and lower risk.

- Secured / balanced funds with a mix of equity and debt for moderate risk.

- Growth / flexi equity funds with higher equity allocation (including Nifty-based strategies) for higher long-term return potential but higher volatility.

- Policyholders can choose one or more funds (as allowed) and have a limited number of free switches per year, after which a small charge applies. During a given policy year, four switches will be allowed free of charge. Subsequent switches shall be subject to a switching charge of Rs.100 per switch.

Charges Under LIC Protection Plus Plan

These charges directly impact investment returns, so long-term investors should review the benefit illustration carefully before buying. While exact charge slabs differ by premium amount and channel (online vs offline), the main charges are:

- Premium allocation charge (higher in first year, lower in later years; lower rates for online purchase compared to offline).

| Policy Year | For Offline Sale | For Online Sale |

|---|---|---|

| First Year | 8.00% | 3.00% |

| 2nd to 5th Year | 5.50% | 2.00% |

| Thereafter | 3.00% | 1.00% |

- Fund management charge (around 1.35% p.a. of fund value, adjusted in NAV daily). And 0.50% p.a. of Unit Fund for Discontinued Policy Fund.

- Policy administration charge (nil for first five years, then a fixed monthly amount with gradual escalation, subject to a cap).

| Policy Year | Policy Administration Charges |

|---|---|

| First 5 Years | NIL |

| Year 6 | – Annualized Premium less than ₹60,000: ₹85 per month – Annualized Premium equal to or greater than ₹60,000: ₹100 per month |

| Thereafter (7th year onwards) | Applicable Policy Administration Charges in 6th year escalating at the rate of 5% p.a. |

- Mortality charges (refunded at maturity as per plan conditions). The rate of mortality charge per annum per Rs. 1000/- Sum at Risk for some of the ages in

respect of a healthy life are as under:

| Age (years) | Mortality Charge (`) |

|---|---|

| 25 | 1.17 |

| 35 | 1.50 |

| 45 | 3.22 |

| 50 | 5.55 |

| 60 | 13.95 |

- Charges for switches, partial withdrawals, and alteration requests beyond free limits.

Should you invest in LIC Protection Plus ULIP plan?

I strongly believe insurance and investments should never be mixed. For pure life cover, term insurance is unbeatable. For long-term growth, mutual funds work best.

Mutual funds outperform ULIPs for pure investment goals due to lower costs, higher liquidity, and better long-term returns, though ULIPs provide bundled life insurance.

Keep these points in mind before deciding to invest in LIC Protection Plus (or not).

- As discussed above, ULIPs offer insurance and investment returns. So, obviously there are costs involved for offering both these features. A portion of the premium that you invest in an ULIP scheme goes towards providing life cover while the remaining gets invested in a Fund chosen by you, after adjusting for the above mentioned charges.

- The way performance returns are calculated in mutual funds is more transparent than in ULIPs. The returns data given in ULIP product brochures can be net off FMCs but exclusive of Mortality charges, Premium allocation charges and other charges (if any). To arrive at exact returns on your ULIP, you need to deduct all types of charges and then arrive at accurate returns.

- In case, your ULIP fund does not meet your return expectation (under-performs), you do not have much choice than to switch to some other fund within the same ULIP. Though switches among the various funds within an ULIP are tax free (does not attract capital gain), you have limited choice and may not meet your original investment objective/strategy.

- If you plan to make additional investment in ULIPs (Top-ups), mortality charges are applicable on these Top-ups as well, besides other ULIP charges.

- Kindly note that the minimum holding period of top-up premiums is 5 years. Top-up premiums are not allowed during the last 5 years of the policy term. These kind of restrictions are not applicable in case of Mutual Fund investments. Each Top-up premium once paid cannot be withdrawn from the Top-up fund for a period of 5 years from the date of receipt of the Top-up premium, except in case of complete surrender of the policy.

- There is no doubt that the cost structure of ULIPs is very competitive now and they have been improving drastically, but I still prefer mutual funds for long-term wealth accumulation. Let’s not forget the fact that a mutual fund house’s core competency is investment and the primary function of an Insurance company is managing risk. So, as an Investor, may be you are better off with Mutual Funds for Investments, on any given day.

Before choosing any financial product, evaluate its costs, potential returns, and alignment with your goals. Do you agree? Share your thoughts. Cheers!

Related articles :

- Mutual Funds Vs ULIPs – Which is better?

- LIC Fixed Deposit Scheme? Awareness Post

- LIC Bima Kavach Term Insurance Plan | Unbiased Review

(Post first published on : 105-Dec-2025) (Please note that this article is based on the limited available information and will be edited/updated, if required)

This post is for information purposes only. We are not biased towards any insurance company or Fundhouse. Mutual funds are subject to market risks.

Join our channels