LIC Jeevan Sangam is a new Endowment plan from Life Insurance Corporation of India (LIC). LIC is launching this policy on 4th March, 2015. LIC’s Jeevan Sangam is a participating, non-linked, savings cum protection and single premium plan. The risk cover in Jeevan Sangam is a multiple of single premium. This new plan is available for sale for a limited period of time i.e., 90 days from the date of launch (This plan is open for purchase till 1st June 2015).

In this plan, the proposer can choose the Maturity Sum Assured (MSA). The single premium amount is based on the chosen MSA and the age of the life insured.

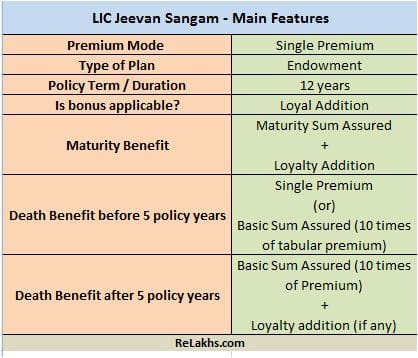

Features of LIC Jeevan Sangam :

- Jeevan Sangam is a Single Premium Endowment plan. It is a conventional / traditional plan (Savings cum protection policy).

- Minimum Entry Age – 6 years

- Maximum EntryAge – 50 years

- Minimum Maturity Sum Assured (MSA) – Rs 75,000

- Maximum MSA – No limit

- Basic Sum Assured (BSA)– 10 times the tabular single premium

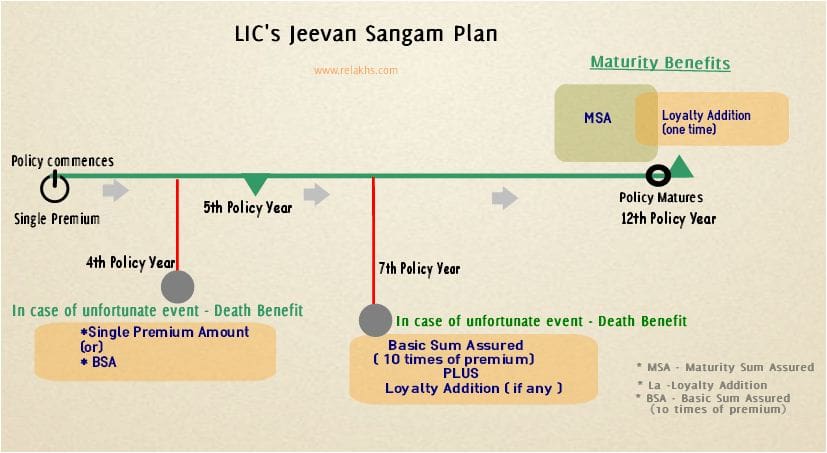

- Policy / Plan Term – 12 years

- Premium Mode – Single Premium

- Maturity Benefit in Jeevan Sangam : On policy maturity, the Maturity Sum Assured along with Loyalty Addition (if any) shall be payable.

Maturity Benefit = Maturity Sum Assured + Loyalty Addition

- Loyalty Addition : The Loyalty Addition shall be payable on death of the policy holder or on surrender of the policy, provided the policy has run for atleast five policy years, or on policyholder surviving till policy maturity.

- Death Benefit in Jeevan Sangam :

- On death during first five policy years:

Before the date of commencement of risk: Single premium amount paid will be refunded. After the date of commencement of risk: Basic Sum assured i.e. 10 times the tabular single premium shall be payable. (What is ‘Date of commencement of risk’ : In case the age at entry of the Life assured is more than 8 years or more, risk will commence immediately. If age is less than 8 years, the risk under this plan will commence from one day before the policy anniversary coinciding with or immediately following the age of 8 years.) - On death after completion of five policy years but before the stipulated Date of Maturity: Death Benefit is Basic Sum assured i.e. 10 times the tabular single premium along with Loyalty Addition, if any, shall be payable.

- On death during first five policy years:

- Surrender option & Surrender value : The policy can be surrendered at any time during the policy year. The Guaranteed Surrender Value allowable shall be as under:

- First year: 70% of the Single premium (excluding extra premiums paid and taxes).

- Thereafter: 90% of the Single premium paid (excluding extra premiums paid and taxes). (If policy is surrendered after completion of 5 years, Loyalty addition (if any) will also be paid)

Illustration of LIC’s Jeevan Sangam Plan

How does Jeevan Sangam plan work? As mentioned above, it is an endowment plan. The premium is dependent on your age and on the Maturity Sum Assured (MSA) you choose. You have to pay premium only once and risk cover is available through out the policy tenure. On maturity, you get MSA, along with Loyalty Addition (LA).

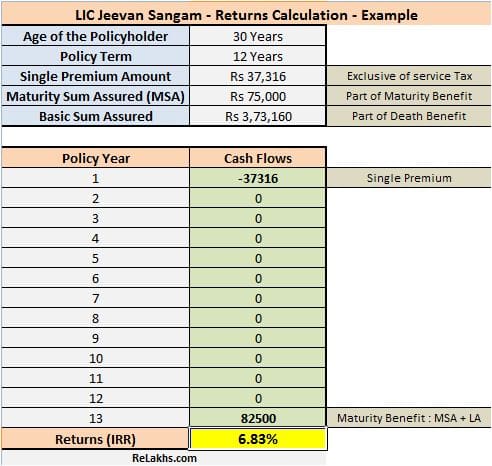

Calculation of Returns on LIC Jeevan Sangam

So, is this plan a good one or bad one? Is it worth your money? Let us calculate the returns with an example. I have used the IRR (Internal Rate of Return) function of Microsoft Excel (MS Excel) to calculate the returns on policy maturity.

As calculated above, the returns from LIC Jeevan Sangam can be around 6% to 7%. I have assumed 10 % of Sum assured as Loyalty Addition (which is on a higher side), still the returns are just 6.83% only. You may expect Loyalty Addition (LA) of around 8% of Sum Assured as one time payment. So, the returns are highly dependent on Loyalty Addition payout.

My opinion :

We are at the fag end of the Financial Year 2014/2015. People generally rush to buy tax-saving plans at the fag end of a financial year. So, its a perfect time to launch a traditional policy, that too a single premium plan. Let’s say, your Section 80C is still not complete and you can invest Rs 50,000 more. In this scenario, a single premium plan looks like a perfect investment to fill your Section 80C. Is this the right way of planning your taxes?…..NO….

Do not buy a Life Insurance plan, just to save some taxes. You will curse yourself if you buy a traditional plan in a hurry to save tax.

- Do not mix insurance with investment.

- You can expect returns of around 6% from these kind of policies.

- It is better to buy a simple Online Term Insurance plan (Read my article on “Top 9 Best Online Term Insurance Plans“)

What is your opinion on LIC Jeevan Sangam? Do share your views and comments.

Continue reading :

- Traditional Life Insurance Plan – A terrible Investment option?

- If Life is unpredictable, INSURANCE can’t be optional

- Life insurance : How to get rid off unwanted life insurance policies?

Join our channels

Dear sir, i need to invest 5000 annually for the benefit of my children whose age are girl 11 yrs and boy 3 yrs,which is the best option

Dear kokila,

May I know if you have adequate life insurance cover?

Kindly read below articles;

Kid’s education goal planning & calculator.

List of best investment options!

Hi Sreekanth,

To Cover 80C for my wife,

1. she is planning to invest in some one time investment plan by today/tomorrow only (as there is no time left).

2. She already has various LIC term insurance with 33k premium.

3. She needs to invest 90k to cover for 80C

4. She may leave the job next year, so she does not want to go for another term policy (moreover when amount is so high i.e. 90k)

Please suggest.

Regards

Ranjan

Dear Ranjan..I know this is a late reply ..

Suggest you to plan taxes from the beginning of the FY itself. This FY, plan your taxes from this month itself.

Read:

List of best investment options.

Best ELSS Funds.