Insurance Regulatory Development Authority (IRDA) has released its Annual report for 2015-2016 on 15th December, 2016. Based on the annual report, I had listed down Top 10 Best best Life Insurance companies. The criteria for the selection is Individual Death Claim Settlement Ratio 2015-16.

What is Death Claim Settlement Ratio w.r.t Life Insurance?

Claim settlement is one of the most important services that an insurance company can provide to its customers. Insurance companies have an obligation to settle claims promptly. For instance, if a life insurance company receives 100 death claims and settles 95, the claim settlement ratio of that company would be 95%. We can also calculate Claim Settlement Ratio based on benefit/claim amount paid.

Based on IRDA’s annual report 2016, I have collated some important points as below;

Life Insurance Business in India in 2015-16

- The share of life insurance business in India was at 79% while that of non-life insurance business was at 21 %.

- India’s share in global life insurance market was 2.24% during 2015 where as it was 2.08% in 2014.

- At the end of March 2016, there are 54 insurers operating in India of which 24 are life insurers, 24 are general insurers and 5 are health insurers exclusively doing health insurance business. In addition, GIC is the sole national re-insurer.

- The Life insurance penetration in India saw a slight increase in 2015 reaching 2.72 % when compared to 2.6% in 2014.

- Life insurance industry recorded a premium income of Rs 3,66,943.23 crore during 2015-16 as against Rs 3,28,102 crore in the previous financial year, registering growth of 11.84%.

- During 2015-16, the growth in renewal premium was 6.20 per cent (10.72 per cent in 2014-15). First year premium registered a growth of 22.53 % in comparison to a decline of 5.81 % during 2014-15.

- Unit-linked products (ULIPs) registered a growth of 12.62 percent premium from Rs 41,617.80 crore in 2014-15 to Rs 46,871.58 crore in 2015-16. On the other hand, the growth in premium from traditional products was at 11.72 per cent, with premium Rs 3,20,071.65 crore as against Rs 2,86,484.20 crore in 2014-15.

- On the basis of total premium income, the market share of LIC decreased from 73.05 per cent in 2014-15 to 72.61 per cent in 2015-16. The market share of private insurers has increased from 26.95 per cent in 2014-15 to 27.39 per cent in 2015-16.

Life Insurance : Death Benefits paid in 2015-16

- In the year 2015-16, the life insurance companies had settled 8.54 lakh claims on individual policies, with a total payout of Rs 12,636.66 crore.

- The number of claims repudiated/rejected was 15,157 for an amount of Rs 736.51 crore.

- Settlement ratio of LIC had increased to 98.33 percent during the year 2015-16 when compared to 98.19 percent during the previous year.

- The industry’s settlement ratio had slightly increased to 97.43 percent in 2015-16 from 96.97 percent in 2014-15.

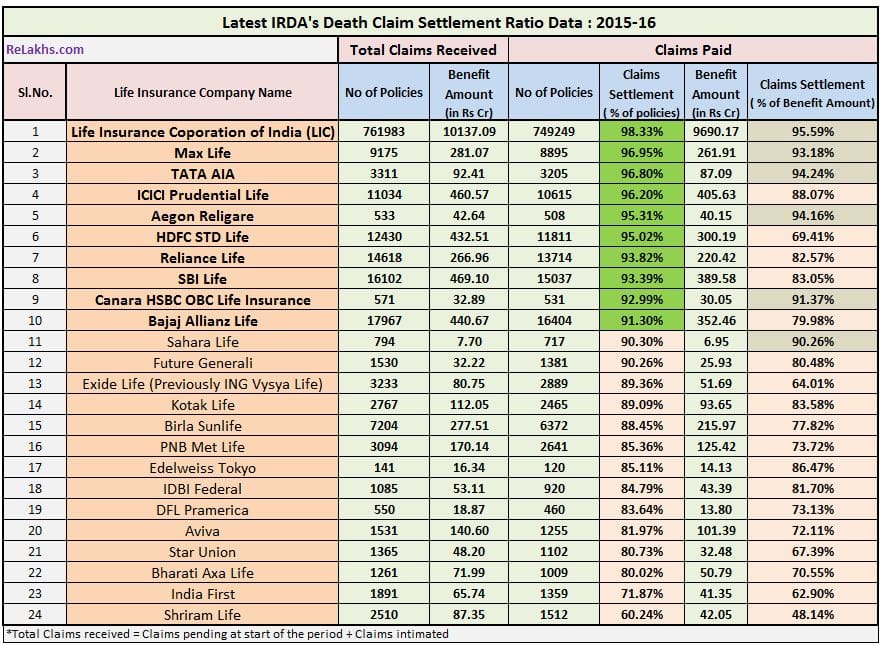

Latest IRDA Claim Settlement Ratio 2015-16 data

Below is the latest individual death claim settlement ratio based on IRDA’s 2015-16 annual report;

How to read above IRDA Claim Settlement Ratio Table?

Let me explain on how to understand the numbers given in the above table. Let us consider Sl.No. 1 which has data regarding LIC. During the period 2015-16 the total number of claims (no of policies) received by LIC of India are 7,61,983. This is inclusive of last period’s pending claims (if any) and this period’s (2015-16) claims that are booked or intimated.

7,49,249 policies out of total 7,61,983 policies were settled during the period 2015-16. This translates into a death claim settlement ratio of 98.33% for LIC.

The total claimed amount (Benefit Amount) on LIC policies during 2015-16 was Rs 10,137 Cr. Out of which Rs 9,690 crore worth of claims were settled.

As per the above explanation LIC gets 98.33/100. So, what happened to 1.67% (100-98.14%) of claims (no of policies)?

These claims fall under the category of claims repudiated or pending or written back. (Repudiated means Claim rejected. Pending are yet to be settled and Written back claims are ‘sent back for more information.)

Top 10 Best Life Insurance Companies based on Claim Settlement Ratio 2015-16

- The claim settlement ratio of LIC has increased slightly to 98.33% from 98.19%.

- The second place has again been retained by Max life with CSR of 96.95% in 2015-16.

- TATA AIA Life insurance

- ICICI Prudential Life insurance

- Aegon Religare

- HDFC Standard Life

- Reliance Life’s claim settlement ratio has increased considerably 83.84% to 93.82%

- SBI Life

- Canara HSBC OBC Life insurance

- Bajaj Allianz Life

Important Points to ponder upon

- The claims settlement ratio does not talk about the type of policies i.e., whether the claims that were received are Term insurance plans or endowment or money back plans.

- Before buying any type of plan, do look at the company’s Claim Settlement Ratio. But kindly note that Claim ratio is just one of the factors and not THE factor when buying a Life Insurance Policy.

- Though Claim Settlement record is one of the important factors while choosing your life insurance plan, it is advisable to go for only Term Insurance. You can opt for a Term plan based on the claim settlement record. The other deciding factors can be cost of premium, features, optional riders, quality of service and your comfort level with the Brand. (You may like reading : Top 7 Best Term Insurance Plans).

- Do not hide any facts while filling the proposal form. This will ensure that your claim (in any unfortunate event happens) is settled.

- As per the recent amendment to Section 45 of the Insurance Act, If your policy is 3 yrs old, no matter what happens, the life insurance company will not be able to deny the claims. So, your life insurance company has only 3 years in hand to reject the policy based on any mis-representation or mis-statement. Once 3 policy years are completed then the life insurance company has to settle the claims and can not reject them.

Most companies cite incomplete documentation or concealment of facts as a reason for rejecting claims. Hence, while buying a life insurance it is of utmost importance that you furnish accurate information and ensure that all paper work is into place. Give importance to claim settlements record and do not get swayed away by higher returns / tax benefits alone.

(Image courtesy of Stuart Miles at FreeDigitalPhotos.net) (Source & Reference : IRDA Annual Report 2015-16) (Post published on 21-December-2016)

Join our channels

Hi Sreekanth,

I am 28Y old and my annual income is around 47K. I am not into any LIFE Insurance Term Plan till now.

I had went through IRDA CSR 2015-2016 and policy features of different Insurance companies.

I am about to take EXIDE LIFE Insurance Life Smart Term Plan(114N083V01) for 30Y with an annual Premium 10201/- + Service Tax (384/-) for sum assured 50L. I see annual Premium is bit higher than other companies but the guaranteed Maturity benefit is 306,030/- . Can you suggest me whether we can trust and opt for it where it has less CSR when compared to your TOP 5 Term Insurance Plans.

Dear Ravan,

Exide Life Smart Term Plan, offers you comprehensive protection and returns the premiums paid by you on completion of policy term.

Since you are getting back all the paid premiums, the premium rate is on the higher side.

Suggest you to buy a basic cover term insurance plan (without return of premium option) from a company of your choice.

You need to just disclose all the required details in the proposal form honestly and accurately.

Dear Sir,

Can you please guide we what are the point which need to be keep in mind while purchasing a term life insurance product. As there are so many similar product but to whom rely upon. so in future the dependent should get trouble in case insurer is not available/ upon death.

Dear Mani ..You may kindly go through this article, can be useful to you : Best Term insurance plans.

Hi Sreekanth,

Could you please try to procure data for “Latest IRDAI’s Claim Settlement Ratio 2016-17” (same as above table)? It would be very helpful to understand who others are consistent performer other than LIC.

Thanks.

-Manan

Dear Manan .. We may have to wait till this year end to get latest annual report of IRDA.

i was given a project on failure of life insurance in india and i guess i got the wrong home work or can any one help me

Can I claim multiple insurance ? Like I have insurance on hdfc, LIC, Max life. 25 lakhs per insurance. If anything happened means, Will my family will get the amount from 3 companies ??

Dear kathiresh,

Yes, provided all the required information in respective proposal forms have been provided accurately and honestly.

Dear Sreekanth,

with regard to home loan protection, Is it better to buy a new term plan or to go for home loan protection insurance? kind request to you to suggest any suitable plan. Loan quantum is 25 L and tenure 18 yrs. bank is asking to assign a policy equal to quantum & tenure of loan.

regards

RAJ

Dear Raj,

Do you already have adequate life cover? (through term insurance plan??)

Basic Term insurance is a better alternative than a mortgage insurance policy. The term plans are cheaper and also provide high cover to the borrower.

Dear Sreekanth,

Thank you very much for your kind reply. YES, I have term cover as per your advice in the blog ” IF LIFE IS UNPREDICTABLE, THEN INSURANCE CAN’T BE OPTIONAL”. But i dont want to assign it to bank. So i thought i will buy a new term cover with the sole intention of home loan coverage.

regards

RAJ

Dear Raj ..Then it is advisable to buy a new Term plan with basic cover option.

Dear Sreekanth,

Thanks a lot.

regards

RAJ

I HAVE PURCHASED A HEALTH INSURANCE POLICY FROM APOLLO MUNICH HEALTH INSURANCE FOR A SUM ASSURED OF RS. 5 LACS AND THE PREMIUM IS RS.7300 IS IT BETTER POLICY FOR ME PLEASE TELL ME ABOUT OTHER POLICY WHICH IS BETTER THEN THIS

Dear Rahul,

Kindly read:

Best Portals to compare health insurance plans.

Evaluate these factors when buying a health plan.

Hi

Recently I buy a term insurance from Aviva life insurance of amount 50 lac for myself. Is this a good decision of I should change the insurance company as I am also aware of section 45 of insurance act. I am perfectly fit and fine and I am married with 2 children.

Thanks

Amit

Dear Karan,

You may stick to your buying decision, assuming you have disclosed all the required info to your insurer.

Hi Srikanth

A advise require my mother age 53, filing ITR also , please suggest good term insurance or whole life insurance for her. She is fine and good in health just overweight. Advise require

Thanks

Karan Giri

Dear KARAN,

Does she has any one as dependents on her financially? May I know why would you like to take Life cover in her name?

No independent on her, also she would like to pay for herself

Dear Karan,

If she does not have any dependents and/or does not have any financial liabilities/obligations then life insurance cover is not required in her name.

You can suggest her to buy a Health insurance plan (if she does not have one).

Hi Srikanth,

Very useful and very informative.

I have two queries.

1. Is the CSR is for only Death or all other inclusive..like ULIP and no death occurred and final amount settled..

2. I have policy with Aegon life. But here it is mentioned as Aegon Relligare. Initially it was Aegon Religare. But now name changed. But why then still IRDA is giving same name..

Dear Ashok,

1 – These are individual death claims related data.

2 – Yes, its been renamed as Aegon life sometime in dec 2015 i guess, may be IRDA will publish new name from next annual report onwards..

Thank you Very much..I got clarified.

Hi Sreekanth,

Very nice article again. I personally feel that instead of CSR, people should look at Percentage of benefit amount settled amount. It tells clearly about the companies intentions, for ex: if you observe the claim settlement ratio and percentage of benefit amount for HDFC life, its gone really WORST in percentage of benefit amount. and this is the 3rd or 4th successive year their ratio has gone very bad. This tells that its an unreliable company as far as life insurance is concerned. HDFC life is here to make profit and they are not serious about their customers. rest all companies have maintained a decent ratio. Do you really think HDFC deserves 6th position in ranking? They dont settle big amounts intentionally even though they insure people for big amounts and take premiums. All other companies have done good work otherwise.

regards

RAJ

Dear Raj,

Thank you for sharing your views.

I do not understand why IRDA does not provide Claim settlement information as per Product wise, Term plan- Endowment-ULIPs etc., I think they do have this data but not providing it in their annual report.

If they do so then benefit amount Vs Claimed amount can really be a good factor to consider.

Hi Sreekanth,

you are very right. IRDA does not give stats about term plan claim settlement ratios. my assumption is, if you look at Benefit amount and percentage of benefit amount settled, it fairly indicates, how fast the insurance companies settle big amount claims easily. for ex;

ICICI benfit amount 460 crores and settled amount is 406 crores, means fairly ok.

Kotak life benefit amount 112 crore and settled 93 crores

Max life benefit amount 281 crores and settled 262 crores

HDFC benefit amount 432 crores and settled amount is 300 crores ???? where is rest 132 crores? its a huge amount they have not settled. Please note that they dont have much traditional plans to offer. its majority Ulips and term plans in HDFC. So, it means that big amount claims being usually term plans are NOT settled easily. By simple mathematics, that is the reason for WORST benefit settled ratio. A ratio of 80% plus will be decent indicator of companies intentions.

regards

RAJ

Dear Raj,

Agree with your view point.

This is the reason why I have also tried to provide details of both number of policies settled & benefit amount paid. Probably, have to put one chart taking into amount settled scenario as well 🙂

Hi Sreekanth, Basis above table can I say Aviva is better than HDFC in terms of CSR. Though Aviva is behing HDFC in terms of CSR {% of policies} they are above HDFC in terms of CSR {% of claim settlements}. Please share your view.. Regards,

Dear vikram,

The difference between the two in terms of % of policies is bit high when compared to the diff between % of Benefit amount paid.

Let’s note that CSR is only one of the important factors that need to be considered when buying a life insurance policy, there are many other factors too…