When Karthik’s father had a medical emergency, he decided to pursue one of the many loan/credit card offers he receives on a daily basis. Initially, all looked positive as the over-enthusiastic bank representative excitedly pointed all the benefits Karthik would receive and how this was truly the best decision of his life.

However, Karthik was only interested in getting loan approved as fast as possible and get his father’s treatment started. He had inquired about the eligibility criteria and he was told all he needs is a valid Address proof & Id-Proof. He waited for 4 days for the bank to finish all the formalities and then get to see his phone buzz with an SMS from the bank. With a sigh of relief he read the message, but his heart sank. The message read:

“Dear Customer, We Are Sorry To Inform Your Profile Has Been Rejected”.

He frantically called the bank representative and to his shock, all his attempts to reach him were ignored. Karthik was absolutely baffled. He could not understand why this would have happened to him. But, he had no time to waste after this he started contacting his friends/family for help.

This was Karthik’s story. But, it could be anyone one of us.

With banks/credit lending companies are doing everything they can to educate you about the benefits of their product, what they usually do not tell is that there are several layers of checks that are done before they approve you for the loan. So, it is a dichotomy. On the one hand, you are constantly told all you need to get approved is a valid Id-proof/address proof and on the other hand, they check things about you that you yourself might have forgotten.

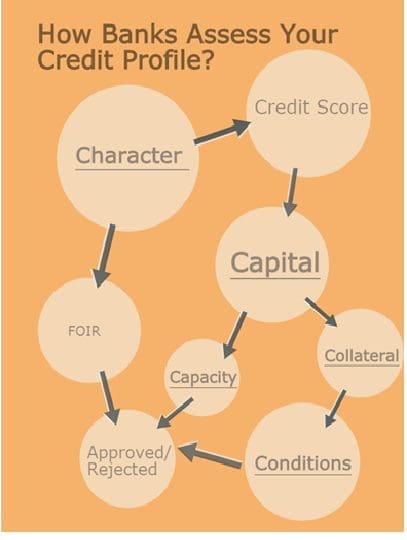

This method of analysis is very well known as the 5 Cs of credit in the banking/lending industry. Let’s discuss on – how banks assess whether or not you are financially healthy enough to be approved for a loan.

5 Cs Banks Use For Assessing Your Credit Health

Do You Have an Intention of Paying Back the Loan? – Character

When deciding the degree of risk of default a prospective customer poses, the banks/lending companies try to establish whether or not he/she has an intention to pay.

Confused?

How will they know you have the intention to pay?

It’s fairly easy actually. They do it via the help of looking at your Credit Reports.

Just like your academic report card, a credit report is a detailed analysis of your financial performance till date. A credit report attaches a credit score to each individual, which is a number that reflects your credit worthiness to the bank. In India, we have four credit information companies that are Equifax, CRIF high mark, Experian, & CIBIL.

Among these, the most commonly looked at report is the one by CIBIL. Most banks and lending companies look at your CIBIL score as the first eligibility check with help of your PAN card number.

Here’s what a CIBIL score is able to tell about you-:

- Each time you are late or you have defaulted on a payment in the past.

- If you have multiple credit products (cards/loans/credit line) and you have a high utilization rate on all of those while the repayment burden is also high. This essentially means that you are using all sources of credit you have, but you are not paying back enough on time.

- If your CIR (Credit Information Report) reflects that you have taken a higher percentage of unsecured loans.

- If you are regularly seeking new means of credit, then your profile is a cause of concern for the banks.

What if you lost your job? Will you still be able to pay back – Capital

Once the bank assess that you have a good credit score (and your intentions are established), the next thing is whether or not you have some capital in the form of financial assets such as fixed deposits that you can use in case you of any unfavorable circumstances.

Do you have a stable income source? – Capacity

Next, the banks assess whether or not you have a stable monthly income which you can use to payback the borrowed sum.

Banks also calculate your FOIR (Fixed Obligations to Income Ratio) to gauge whether or not you are capable to repay your loan. Essentially, what happens is that banks work under the assumption that you need 45 to 50% of your monthly income to meet your expenses. These include the active EMIs and other debts. Now, if you are utilizing more than 50% of your income for these expenses, then banks consider you as a risky customer.

FOIR = Sum addition of all installments / Monthly Income

Thus, to be approved, you should have a low FOIR along with a high credit score.

Is there any unfavorable circumstance that could affect you and your ability to pay in the future? – Conditions

This is more specific to business loans. The banks try and ensure that the economics and market conditions of the industry you work in are stable and you will not have difficulty in generating and repaying the debt.

In case of default, can the bank still recover its principal? – Collateral

Most loans such as car/home loans they are only approved in return of some tangible asset (collateral) which has both quality and salability.

So, these were the 5 Cs which most banks usually consider while deciding whether or not to give you a loan. They do seem scary, but in reality, all you need to do is keep paying back in time and maintaining healthy borrowing habits so that your profile does not become a risky one for your potential lenders.

Few Things to Keep in Mind :

- If you apply for multiple credit products at the same time, then with each enquiry your CIBIL score is hit negatively by a few points. Also, when the banks see that you are making several inquiries at the same time, it is considered a negative sign.

- You can calculate your FOIR beforehand before applying for a loan. This will help you decide whether or not to pursue applying for loans. For instance, if your FOIR is above 50%, you can decide to first payback the existing debt, so that it reduces and then you can apply for a new loan. This will improve your chances of getting approved.

This is a guest post by Ms Suruchi of MoneyTap.

Author & Company Bio :

MsSuruchiKhandelwal is currently leading content marketing at MoneyTap. She has been into the content business for the last 5 years now. MoneyTap is India’s 1st app-based credit line which is working towards improving the availability of credit for the middle-income group in India.

Continue reading other related articles :

- How to get your Free Credit Score & Annual Credit Report online?

- A Negative Credit Score can hurt your Job Search!

- 5 ways of making Creditor Proof Investments

Kindly note that ReLakhs.com is not associated with MoneyTap. This is a guest post and NOT a sponsored one. We have not received any monetary benefit for publishing this article. The content of this post is intended for general information / educational purposes only.

(Image courtesy of Stuart Miles at FreeDigitalPhotos.net) (Post published on 26-September-2017)

Join our channels

Hi,

I have settled my Axis Bank Credit Card in the year of 2009 for 30,000/- while the total amount pending was 45,000/-. Now I have requested the bank to provide the Masking amount to get the account to closed status in CIBIL and Axis Bank have sent me a quote of 3,36,200/- to be paid. Im really shocked on seeing this as I was expecting it at a maximum of 30,000/ Please let me know if this a right amount and on what basis they calculate this? Also let me know if these Banks still add interest to pending amount even after getting it settled?

Dear Sreekanth,

Happy Dasara to You and Your family and all staff of relakhs.com. Very Well explained article and all the details are very well covered.

regards

RAJ

Dear Raj..Thank you so much for your wishes.

Happy Dasara to you all too!