Banks in India have become easily accessible for getting loans for use by individuals. Debt and Loans are becoming common these days. The amount of total financial liabilities held by Indian households justifies this statement.

As per the RBI’s statistical data on Indian Economy (2016) ;

- Around Rs 2,605 billion were taken as Loans and advances from the Banks during 2014-15. This figure is around Rs 3,544 for the FY 2015-16.

- Loans taken from other Financial institutions (NBFCs) during 2014-15 & 2015-16 were Rs 591 billion and Rs 657 billion respectively.

- The total financial liabilities of the households have increased from Rs 3,204 billion (in 2015) to Rs 4,212 billion (in 2016).

If you have taken a loan (credit card advance, home loan, personal loan etc.,), things are good until you make regular payments (EMIs). However, if you make late payments and/or start defaulting then things can get really murky for you.

If you are a self-employed or professional, there can be more risks involved in your personal financial life. You might have to take business loans, hand loans, SME loans etc., to meet your capital requirements.

In case of loans where collaterals are available, banks may auction them and get back their money. But, if there is no collateral (security) or it is not adequate enough to recover their dues, the lenders/creditors may arrive at your doorstep and they have the power to attach assets to recover their dues. They can approach court and can get the attachment order. (The situation can be the same if the borrower dies..the lenders can attach borrower’s personal investments.)

Hence, its prudent to have a clear demarcation between your personal assets and business assets. Even, if you are a salaried person, you can be pro-active and make investments in Creditor proof instruments.

Kindly note that this article is not to encourage you to default on your loan payments, but to encourage you to be pro-active. Make sure you invest in these creditor proof investments even before you acquire the liability (loan/debt), otherwise there are chances that your arrangement can be challenged in court of law and can be termed as fraudulent.

What are Creditor proof investments ? – The investments that can not be attached by the court of law and can not be claimed by the creditors. The claim proceeds are free from creditors, court and tax attachments.

Popular ways of investing in Creditor proof investments

1) Provident Fund (PPF & EPF) :

PPF (Public Provident Fund) is a very popular Small Savings Scheme in India. It falls under Exempt-Exempt-Exempt tax category and the returns are guaranteed.

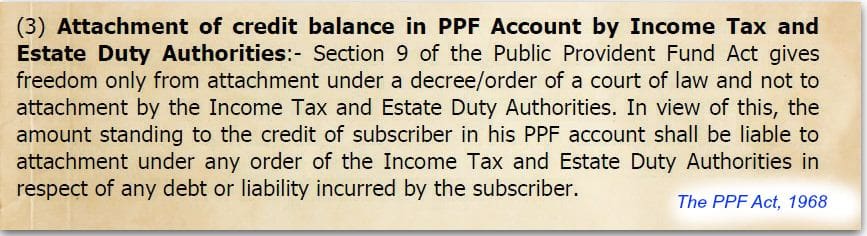

The deposits in PPF account have protection against any court attachment and creditors. However, Income Tax Authorities can attach PPF deposits.

EPF (Employees Provident Fund) is also creditor‑proof: the balance in a member’s EPF account cannot be attached by a court to satisfy debts of the member or the nominee.

Section 10(1) of the Employees’ Provident Funds and Miscellaneous Provisions Act, 1952 states that the amount standing to the credit of any member in the Fund is not capable of being assigned or charged and “shall not be liable to attachment under any decree or order of any court.”

Creditors cannot claim or attach EPF money even after the member’s death; the law explicitly protects the amount payable to the nominee or heirs from such claims. n simple terms, neither the deceased member’s personal creditors nor the nominee’s own creditors can get a court to attach that EPF amount.

Gratuity. Under the Payment of Gratuity Act and Section 60 of the CPC, your gratuity is legally shielded from attachment. It’s your hard-earned safety net.

2) Investments in National Pension System (NPS) :

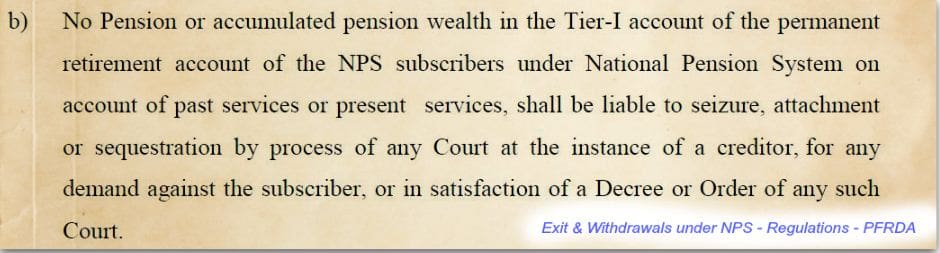

As per the PFRDA (Exits and Withdrawals under NPS) Regulations 2015, “No pension or accumulated pension wealth in TIER 1 account under national pension system, shall be liable to seizure, attachment or sequestration by process of any court at the instance of creditor for any demand against the subscriber, or in the satisfaction of a decree or order of any court.”

3) Assignment of Life insurance Policy

Assignment of a life insurance policy means transfer of rights from one person to another. You can transfer the rights on your insurance policy to another person / entity for various reasons. This process is referred to as ‘Assignment’.

The creditors can get a court order and claim their dues by attaching the proceeds of life insurance policies. But, the ‘assigned’ insurance policies can not be attached. They can not claim the proceeds of an ‘assigned’ life insurance policy.

The person who assigns the insurance policy is called the Assignor (policyholder) and the one to whom the policy has been assigned, i.e. the person to whom the policy rights have been transferred is called the Assignee.

Once the rights have been transferred from the Assignor to the Assignee, the rights of the policyholder stands cancelled and the assignee becomes the owner of the insurance policy.

(Related Article : ‘How to assign a Life Insurance Policy?‘)

4) Life Insurance policy under MWP Act

Married Women’s Property Act was created to protect the properties owned by women from relatives, creditors and even from their own husbands. The Act has been created to protect women’s rights, even after marriage. MWP act is applicable for all married women of all religions. ‘Section 6‘ of the MWP Act covers Life Insurance plans.

If you take an insurance policy under MWP Act, your life insurance policy is treated as a TRUST and you can be assured that the policy money will be given to your nominee(s) only. The claim proceeds are free from creditors, court and tax attachments.

Related Articles :

- How to get an Insurance Policy under the MWP Act?

- Nominee or Legal heir ? Who can claim the Death Benefit of a Life Insurance policy?

5) Creation of Trusts

You can protect your Personal Assets by transferring them to a Private Trust. Once you form a TRUST, it is treated as a separate entity and it can not be attached by court, unless it is proved that it has been created only to defraud the creditors. Kindly note that once the assets are transferred to a trust, they can not be taken back. One should consider taking advice from a Chartered Accountant, before creating a Trust.

Conclusion

- Above are the legal ways to protect your personal assets / investments, kindly opt for them if they meet your investment objectives and not just for the ‘protection of assets’ from your prospective creditors.

- Do watch out for lock-in period, tax implications and pre-mature withdrawal rules & penalties (if any). Also, you may avoid buying traditional life insurance policies but can take Term insurance under MWP Act.

- Professionals should consider taking indemnity insurance.

Debt can be easily acquired, but it is your responsibility to clear it off in time. You may consider making your investments creditor proof, but with good intentions!

(Image courtesy of iosphere at FreeDigitalPhotos.net) (Post published on : 18-August-2017)

Join our channels

Hi,

1) How about Sukanya Samrudhi account.

2) And about PPF account in name of Spose.

Are they creditor-proof-investment ?

Dear Anand,

PPF is yes, but I dont think SSA is a creditor proof investment.

Thanks for this post. I did not know that NPS had this feature! If I am a self employed person then I think a combination of PPT and nps can make up a decent secure nest egg in case things go wrong in professional life.

Dear Tarun.. Kindly go through the rules, pros and cons about NPS and then take prudent decision..

Kindly read : NPS – Benefits & drawbacks..

Thanks!