With the recent repo rate cuts by the Reserve Bank of India (RBI), banks have started reducing fixed deposit (FD) interest rates across tenures. As a result, traditional bank FDs are no longer offering the kind of returns many fixed-income and conservative investors have relied on in the past.

In this falling interest rate environment, investors are naturally searching for better yet relatively stable alternatives to park their money. One option that has started gaining renewed attention is Company (Corporate) Fixed Deposits — which typically offer higher interest rates than bank FDs, but also come with different risk considerations.

So, are company fixed deposits really a smart alternative in 2026? Should conservative investors consider them, or do the higher returns come with hidden risks?

Is interest rate alone a sufficient criterion while choosing a company FD? Which are the best & high interest rate company fixed deposit options in 2026, and more importantly — should you invest in corporate FD schemes at all?

In this article, we explain what company fixed deposits are, how they work, the returns they offer, the risks involved, and who they are suitable for — helping you make a well-informed investment decision.

What are Company Fixed Deposits?

Company Fixed Deposits refer to deposits accepted by companies from investors for a fixed tenure at an agreed interest rate. These are typically offered by financial corporations, housing finance companies, and NBFCs. They refer to fixed deposits accepted by companies from the public, instead of banks.

- Note that in India, the terms Company Fixed Deposits (Company FDs) and Corporate Fixed Deposits (Corporate FDs) are same and used interchangeably.

Best Company Fixed Deposits 2026 | Interest Rate Table Jan 2026

Some of the popular and top Corporate Fixed Deposit schemes (cumulative) that are currently open for investment are as below ;

| Company / Issuer | Credit Rating | 1 Year | 2 Year | 3 Year | 4 Year | 5 Year | Additional Rate for Sr. Citizens (in %) | Min Amount |

|---|---|---|---|---|---|---|---|---|

| Bajaj Finance Ltd | FAAA By CRISIL, MAAA By ICRA | 6.60 | 6.95 | 6.95 | 6.95 | 6.95 | 0.35 (upto 3cr) | 15000 |

| HUDCO | CARE AAA | 7.00 | 7.00 | 7.1 | NA | 6.85 | 0.25 | 10000 |

| ICICI Home Finance Co. Ltd | AAA by CRISIL, ICRA & CARE | 6.85 | 7.10 | 7.15 | 7.15 | 7.15 | 0.35 (Up to 2.99 cr) | 10000 |

| LIC Housing Finance Sanchay | CRISIL AAA/STABLE | 6.70 | 6.80 | 6.85 | NA | 6.9 | 0.25 | 20000 |

| Mahindra & Mahindra Financial Services Ltd cumulative Samruddhi | CRISIL AAA | 6.60 | 7.00 | 7.00 | 7.00 | 7.00 | 0.25 | 5000 |

| Muthoot Capital Services | CRISIL A+ / Stable | 7.90% | 8.65 | 8.95 | 8.75 | 8.50 | 0.25 | 1000 |

| PNB Housing Finance | IND AAA (Stable) | 6.85 | 7.00 | 7.10 | 7.10 | 7.10 | 0.25% (Upto 1 cr at PAN level) | 10000 |

| Shriram Finance Ltd (For Resident Individual) | ICRA AA+ STABLE | 7.00 | 7.25 | 7.60 | 7.60 | 7.60 | .50(senior citizen) ( .05% women) (.15 renewal) | 5000 |

| Shriram Finance Ltd (For NRIs) | ICRA AA+ STABLE | 7.00 | 7.25 | 7.60 | NA | NA | .50(senior citizen) ( .05% women) (.15 renewal) | 5000 |

Note : Company FD Rates can change without notice, and may vary by tenure, cumulative or non-cumulative, payout frequency, or offer type (e.g., Online FD vs regular). Always verify at the NBFC’s or respective company’s official portal before investing. If you choose a Monthly Interest Plan or an Annual Payout, the base interest rates are slightly lower.

Muthoot Capital FD Scheme: It remains the highest interest rate scheme in this list. While it offers significantly higher returns (reaching 9.20% for Senior Citizens at 3 years), remember that it is an A+ rated instrument, placing it a few places below the “High Safety” of the AAA issuers like Bajaj or LIC HFL.

How to choose best Company Fixed Deposit?

If you’re planning to invest in Company (Corporate) Fixed Deposits, don’t just look at the interest rate. Here are a few important things I always suggest checking before choosing a scheme.

- Interest Rate – Don’t Get Carried Away: Higher interest is the main reason people look at company FDs. Companies usually offer rates better than banks. But if you see a company offering something like 12% per annum when others are offering 7–8%, please be cautious. Very high returns often mean higher risk.

- Time Period vs Interest Rate: Generally, the longer the tenure, the higher the interest rate offered. But remember, the biggest risk in company FDs is default risk — the company may fail to pay interest or principal on time. So, I personally do not recommend very long tenures like 8–10 years in corporate FDs.

- Diversification – Don’t Put All Eggs in One Basket: Instead of investing your entire amount in one company FD, it’s better to split the money across 2 or 3 good-quality schemes. This helps reduce risk.

- Credit Rating – Very Important: Before investing, try to understand how strong the company is and why it is raising money from the public. If doing this analysis feels difficult, at least check the credit rating of the FD scheme. Just remember this simple rule:

- Higher-rated FDs usually offer lower interest rates

- Lower-rated FDs offer higher interest, but with higher risk

- For conservative investors, it’s better to stick to AAA rated schemes.

- Credit ratings are given by agencies like CRISIL, ICRA, CARE, etc.

- Special Benefits: Some company FD schemes offer extra interest for- Senior citizens, Shareholders or Employees. For example, many schemes offer 0.25% extra for senior citizens. Always check these benefits before investing.

- Premature Withdrawal Rules: Most company FDs come with a lock-in period (usually 3–6 months). If you withdraw early, there may be penalty charges or reduced interest. These details are clearly mentioned in the application form, so don’t skip reading them.

- Interest Rate vs Actual Returns: Companies often highlight “effective annualised yield”, which can look attractive. But it’s important to understand the difference between: Nominal interest rate & Effective yield, especially in cumulative schemes. Don’t decide only based on big numbers shown in Ads.

- Example: Let’s assume that below are the interest rates offered by a FD scheme (Cumulative). They display Effective yields on deposits. If you observe the effective yield rates are higher than the interest rates. Lets us understand this concept. As per this scheme, a Deposit of Rs 10k becomes Rs 15,742 after 60 months (5 years). It’s s a gain of Rs 5,742 (Rs 15,752 -Rs 10,000). One year gain is Rs 1148 (5742/5). In percentage term it is 11.48%, which is shown as EFFECTIVE YIELD.

- Always compare two Company FD schemes in terms of nominal interest rates. Do not go by effective yields. Also, these yields are not tax adjusted.

- Taxation – No Special Benefits Here: Company FD interest is fully taxable.. There are no tax-saving benefits like some bank FDs. Interest earned is treated as “Income from Other Sources” and must be declared while filing your income tax return. (TDS rules apply as per prevailing limits.)

- Cumulative vs Non-Cumulative Schemes: There are two types of company FD options: Cumulative – Interest is paid along with principal at maturity. Non-cumulative – Interest is paid monthly / quarterly / yearly. If you need regular income, choose non-cumulative. If you don’t need cash flow and want compounding, cumulative can work.

- Remember: Most Company FDs Are Unsecured– Most corporate FDs are unsecured investments. If the company defaults, there is no collateral you can fall back on. Unlike bank FDs, company FDs do NOT have DICGC insurance protection. So, while returns may be higher, the risk is also higher.

- Some of the entities are genuine and whereas some entities collect monies from the public without getting the necessary approvals from the Regulators. So, it is prudent to first check whether a company that you are intending to invest your hard-earned money has got necessary approvals or not.

Related Article : Corporate Fixed Deposits & Collective Investment Schemes – What precautions should you take as an Investor?

Should you invest in Company FD Schemes? – My Opinion

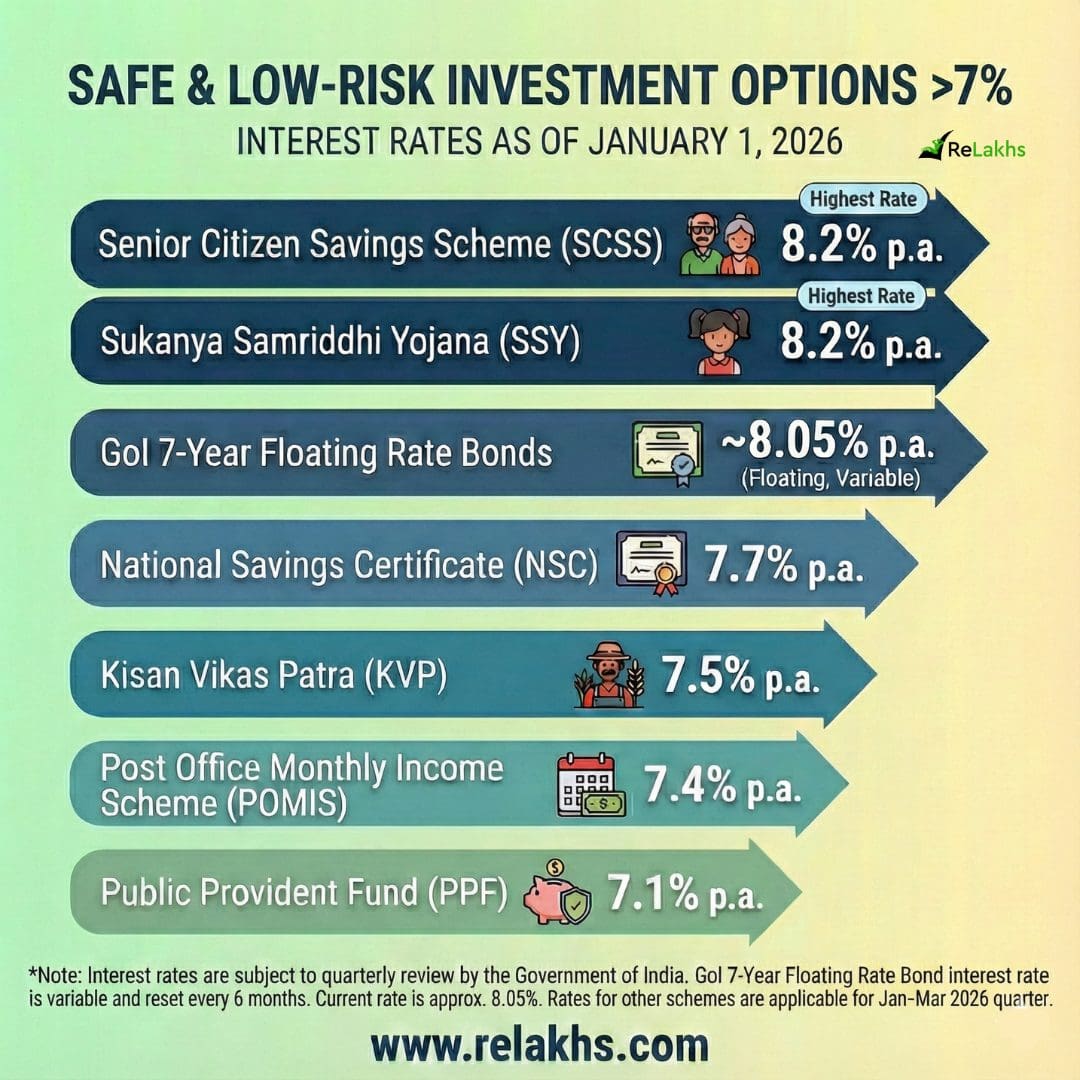

Personally, I feel investors should first explore safer fixed-income options such as PPF, Sukanya Samriddhi, Post Office schemes, Senior Citizen Savings Scheme, Government bonds, secured NCDs, or debt mutual funds, before opting for company fixed deposits. Debt mutual funds are managed by professionals who do the credit research on your behalf, and some of these funds also invest in company deposits.

Avoid investing in FDs offered by companies you are not familiar with, or schemes that do not have a credit rating. And most importantly, never put your entire savings into a single company FD. Always spread your investments.

Company Fixed Deposits can offer better returns than bank FDs, but they demand careful selection, diversification, and a clear understanding of risks.

Have you invested in any company fixed deposit schemes before? Did you face any issues with interest or maturity payments? Are you considering investing in one now?

Do share your experience and thoughts in the comments.

Continue reading:

- LIC Fixed Deposit Scheme? Does LIC offer FD Scheme?

- Corporate Fixed Deposits – What precautions should you take as an Investor?

- Do Small Savings Schemes Interest Rates Change Every Quarter? Fixed vs Variable Explained

(Post first published on : 27-Jan-2026)

Join our channels