Life is full of if’s and but’s. None of us know what might happen even the next minute. If your child, life partner or your parent(s) depend on your income then you need to have a Life Insurance plan with adequate life cover.

Term insurance is the simplest and the most fundamental insurance product. Term insurance plans are designed to ensure that in the event of the policyholder’s death, the family gets the sum assured (the cover amount).

Term plan provides risk coverage for a certain period of time (policy term/duration). If the insured dies during the time period specified in the policy and the policy is active – or in force – then a death benefit will be paid. It is the cheapest form of Life insurance in terms of premium.

Online Term insurance Plans are,

- Cheaper than conventional plans like money back life insurance or endowment plans (or) offline term plans. Online term insurance plans can be 20-40% cheaper than the offline plans.

- The entire application submission process happens online through the company’s website. So, it is hassle free.

- You may not be influenced by an agent/advisor during the buying process.

Ashish Shrivastava, one of my Blog readers have shared his perspective on Aegon Life iTerm Insurance Plan, an online Term Insurance Plan. The views expressed here, are purely his own, and do not reflect the views of ReLakhs. Thank you dear Ashish for sharing your viewpoint.

Key Features of Aegon Life iTerm Insurance Plan

- Inbuilt Terminal Illness Benefit. On diagnosis of any Terminal Illness, 25% of the base sum assured will be paid (max.of Rs 1 Crore) & the base sum assured will be reduced by an amount equal to the benefit paid under this clause. (Definition of Terminal Illness : Terminal Illness is defined as an advanced or rapidly progressing incurable & uncorrectable medical condition, which in the opinion of the treating physician is highly likely to lead to death within the next six months.)

- Covers all forms of death, even terrorist attacks. Exclusion : In case of death by suicide during the first policy year, or within one year from the date of reinstatement, no death benefit is payable.

- Life cover till the age of 75 years.

iTerm Plan Riders

You can make your plan more comprehensive by choosing any of the following suitable riders:

Aegon Life AD Rider: This Rider covers accidental death. In case of death due to accident, the cover amount (Sum Assured) under the rider will be paid.

Aegon Life WOP Rider on CI: This Rider covers 4 critical illness conditions : Cancer, Open Chest CABG, first Heart Attack and Stroke. On being diagnosed with any of these 4 critical illnesses, future premiums payable under the plan and riders (if any) are waived while the life cover and other rider cover continue.

Aegon Life iCI Rider: This rider covers 4 critical illness conditions: Cancer, Open Chest CABG, First Heart Attack and Stroke. The cover amount (Sum Assured) under this rider will be paid on diagnosis of any of these 4 critical illnesses.

Aegon Life Women CI Rider: Rider covers critical illnesses pertaining to women. On being diagnosed with any of the covered illnesses, a certain percentage of the base plan cover amount (Sum Assured) will be paid. The medical conditions that are covered under this rider are – i) Malignant Cancer of the Female Organs & ii) Birth of child with Congenital Disorders / Surgeries and Pregnancy Complications.

Aegon Life iDisability Rider: This rider pays lump-sum benefit under the rider and also waives off the future premiums payable under the base plan upon permanent disability of the Life Assured due to accident or sickness.

These riders can be attached to a base plan on policy commencement or at any time during the term of the base plan. Please refer to the sales brochure of these riders to understand the terms & conditions before concluding a sale.

Personal buying experience

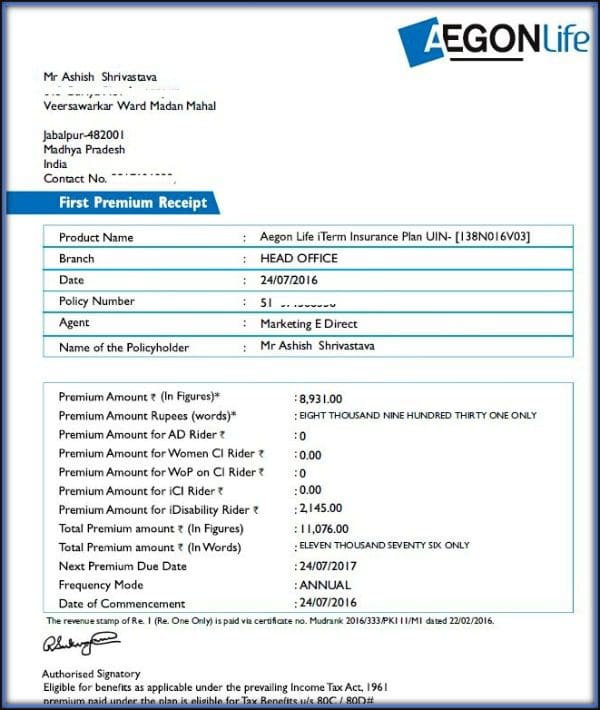

After doing research for almost 1 year and 3 months, I decided to buy Aegon iTerm plan of Sum assured of Rs 1 crore. The policy tenure is till 75 years. I have also opted for iDisability Rider with Sum Assured of Rs 40 Lakh.

Why I chose Aegon

I preferred Aegon as it is offering the longest policy tenure and free inbuilt terminal illness benefit. Aegon premium is one of the cheapest. Their claim settlement ratio is decent. They are the Winner of E–Business Leader for last 3 years and are the pioneers in the life insurance online space by launching India’s first online term plan.

Read: IRDA’s latest Claim Settlement Ratio 2014-15 data

Why I took risk coverage till 75 years

Though many of my friends (including Sreekanth) suggested to buy a term plan till retirement age, I took term plan till 75 years of my age because:-

1) If I need a Term plan even after 50 or 60 years of my age then buying a new term plan will prove very costly at that point of time.

2) If I take this plan with maximum offered tenure then control will be in my hand to continue or discontinue the policy. If I do not need life cover after my retirement, I can just discontinue paying the policy premiums.

3) If I opt for maximum policy term is also very cheap and there is hardly difference of Rs 800 to Rs 1,000 (which is affordable to me) so it is WIN-WIN condition for me to go with policy tenure of up to 75 years.

Why I opted for iDisability Rider

One of the good things about iDisability rider of Aegon is that it covers disability due to Sickness and Accident. If an insured person suffers from stroke or due to any sickness, and if he/she becomes disable (permanent disability) then the company will pay the rider sum assured amount. It covers both total and partial permanent disability and waives off all the future premiums in case of permanent disability. The policyholder can claim for a maximum of two contingent events and the total payout will be limited to 100% of the Lump-sum Rider Sum Assured chosen at inception.

Premium amount of this rider is very cheap. So for me it’s like an alternate to personal accidental insurance. (I’ll buy PA plan of 10 Lakh to cover my other financial obligations like children education, hospitalization so by doing this I’ll be covering myself for higher amount with lesser premium).

My Buying experience

I started filling up proposal form with the help of Aegon customer support on 15th July 2016 and it took nearly 30 minute to carefully filling up form and before making payment I received proposal form which I filled in my email ID for verifying details of what I filled.

After making the premium payment, the customer dashboard was created automatically. The dashboard has proposal form, payment receipt and benefit illustration.

Dashboard has a provision for scheduling the medicals and uploading the self-attested documents. I scheduled medicals on 17th July 2016 and my medical tests completed on 17th July 2016 by 10:30 AM, which is super impressive.

Then I uploaded self-attested documents along with KYC details by 18th July 2016. Aegon took 13 days for issuing the policy.

Disclaimer: Ashish works as a Team Leader at Persistent Systems Ltd. Neither he nor his family members are associated with Aegon Life.

ReLakhs.com is not biased towards any insurance company. This post is for information purposes only. This is not a sponsored or paid post. We have not received any monetary benefit for sharing this article.

We suggest our readers to go through our article ”Comparison of Online Term insurance plans” to have a better understanding about other Term plans as well. You may buy a term plan from any life insurance company that you are comfortable with. Do disclose the required information in the proposal form honestly and accurately. Kindly read and understand the details given in the product brochures, Riders brochures, policy wordings documents etc., before you buy a term plan.

(Image courtesy of fantasista at FreeDigitalPhotos.net. Reference : Plan brochures) (Post published on : 03-August-2016)

Join our channels

I checked iterm plus plan from Aegonlife but I didn’t see any Disability rider on the website? How to get it?

Dear Ram,

You got to opt for iDisability rider along with basic cover.

Kindly go through the below links;

Link – 1

Link – 2

I talked to Aegon. They say these are old plans.

Dear Ram,

Yes, they have launched a new Term plan.

But ITerm plan is still shown on their portal with applicable Riders (optional).

Nice article and good question answer…..I had just finalized aogin life iterm and was finding reviews online and found on this page

….nice knowledge sharing.

Thank you dear Deval ..Keep visiting ReLakhs.com !

Hi ,

on the iDisability Rider:

1) If this amount is claimed for relevant reasons during the policy tenure, will the final sum assured get reduced accordingly when a death benefit claim comes up?

2) Also it says that, this isn’t available for housewives. What if my spouse is working currently, say after 5-6 years quits her job? Would the eligibility still apply then?

Dear phani,

1 – No, the base policy sum assured wont be reduced. You may kindly go through the product brochure..click here.

2 – While taking the policy if she is a non-earning individual, insurer may reject the proposal. In case, she takes it when she is working, insurer may accept the proposal.

Thanks for your response. Customer care rep clarified that, if my spouse is working while taking the policy -> it should be fine. Even after few years, if not working but are paying premium -> we should be fine.

This is the cheapest term insurance policy available in the market. Its USP is that it has disability rider for higher sum assured for a minimum premium.

Only worry I have is that this company is mostly online and they just have one branch in a city like hyderabad. I’ve already read several negative reviews on Aegon company customer service, once a policy is taken.

Premium in other companies like HDFC, ICICI, MAX etc, are so high compared to Aegon. Just confused now.

On another note, after going thru the product brochure – the rider for disability is only for accident / sickness. This doesn’t include natural calamity, terrorist attack etc.,

I’m not sure if its the same case for death benefit on Sum Assured, couldn’t find that in the brochure. In the review, its mentioned that it covers natural calamities / terrorist attacks as well.

Went thru the entire brochure and couldn’t find that death due to terrorism / natural calamities are covered as well. At the same time, its not mentioned that they are excluded either. Does this mean, its covered? 🙂 .

Also read that the SA paid to the beneficiary is taxable. So in 1 CR SA, the beneficiary only gets 70 Lakhs is it? (going by 30% tax bracket and lump sum payment).

Dear Phani,

SA under iDisabiility rider is not payable in case of Terrorist Acts/War ..Kindly go through this link ..(page no 6)

Regarding SA death benefit (basic cover) availability on death due to terrorist attacks, I believe you can get an email confirmation from the insurer (I do remember that I have read it somewhere in Policy wordings document, but unable to trace it now).

Thanks for your reply. The SA in case of an unfortunate event, are they non taxable?

Dear Phani ..Yes, death benefit amount is tax-exempted.

Excellent article, though I found it a bit late. It would anyway have helped me to reach the same conclusion that I had come to already – “AegonLife iTerm plan is one of the best term plan (on paper) out there”. Combine this with the recent amendment to Section 45 of the Insurance Act, and in 2 years (after you have purchased it) it easily becomes the best insurance plan in deed.

Its biggest USP, IMHO and as mentioned above, is the most unique ‘iDisability rider’. As of today, no other insurance provider is offering cover for ‘disability due to natural sickness’ either as a rider or stand alone plan (Personal accident/ health insurance). Therefore, it covers almost all the contingencies for which one buys an insurance plan. Combined with proper PA cover and Health insurance as per individual’s requirements, it allows you to create a truly comprehensive insurance cover. Term plans of all other insurance provider will leave that big hole ( disability due to natural sickness) in your contingency plan.

Dear Anuj .. Thank you for sharing your views!

Hi Sreekanth,

1) Today, I was trying to buy an Online Aegon eTerm Life Policy (Regular) for 2 Crores SA, but the Premium calculated on their website, when i filled in my requested details, is almost around 3K+ per month (over 36K per year). Is this normal?

Am i missing out on anything, or have the Premium rates gone up, since the time you wrote the article giving details of this policy, back in Feb 2017, i believe?

Also, in the above post also from Ashish, he mentions paying 11K for a year, then how come so high Premium? Please share your thoughts.

Secondly, I have a TATA AIA Life Insurance policy which i took in May 2016, where I have to pay a yearly premium of 1 Lakh for ONLY 5 years, and the policy states that after 10 years, I will be entitled for a SUM Assured of 10 lakhs. Should I keep this or surrender? Also, the amount paid of 1 lakh last year, will it be paid back to me, atleast some SUM of it? My next Premium date is May 2017, hence wanted to know.

thanks and regards,

J.D

Dear Jovy,

1 – Have you opted for any Optional rider(s) along with Basic life cover? When I checked, for a 30 year old male, for a term of 30 year with Rs 2 Cr SA, the premium is coming around Rs 1,016 only. This is iTerm plan.

2 – May I now the Plan name??

Hi Sreekanth,

Their official website never gave me an option to choose any Riders. When i filled in my requested generic details, and the SA, it simply gave the Premium amount. Plan name is iTERM. By the way, I am 35 yrs old, Male. Would have opted ONLY for the Premium Waiver Rider, as I will be taking a stand alone PA Insurance, based on your insightful posts.

Secondly, I have a TATA AIA Life Insurance policy which i took in May 2016, where I have to pay a yearly premium of 1 Lakh for ONLY 5 years, and the policy states that after 10 years, I will be entitled for a SUM Assured of 10 lakhs. Should I keep this policy or surrender? Also, the amount paid of 1 lakh last year, will it be paid back to me, atleast some SUM of it? My next Premium date is May 2017, hence wanted to know.

regards,

J.D.

Dear Jovy,

2- I have asked for the Plan name ???

Had already mentioned in my earlier comment as; Plan name is iTERM.

thanks and regards,

J.D

Dear Jovy,

Regarding Aegon Plan, I have already provided the required details, you may contact their customer care if you need more details on premium calculation.

I have asked for the plan name of TATA LI policy.

My bad Sreekanth, thought you asked about Aegon.

The other plan is TATA AIA Life Insurance Fortune PRO (110L112V01).

thanks and regards,

J.D

Dear Jovy,

TATA AIA Life Insurance Fortune is Unit linked plan. The minimum premium payment term is 15 years.

5 year is the minimum lock-in period for any type of ULIP plan.

Generally, the charges of ULIP plan will be more than mutual funds, over a long-term period.

If you surrender the policy now, the surrender value of the ULIP fund is kept for 4 more years in Discontinued fund, and nominal interest (can be around 4%) will be paid on this and you can withdraw the amount after 5 policy years only.

Dear Jovy,

TATA AIA Life Insurance Fortune is Unit linked plan. The minimum premium payment term is 15 years.

5 year is the minimum lock-in period for any type of ULIP plan.

Generally, the charges of ULIP plan will be more than mutual funds, over a long-term period.

If you surrender the policy now, the surrender value of the ULIP fund is kept for 4 more years in Discontinued fund, and nominal interest (can be around 4%) will be paid on this and you can withdraw the amount after 5 policy years only.

Thank you Sreekanth, my apologies for the delayed response. God Bless.

regards,

J.D

You are welcome dear Jovy ..

Keep visiting ReLakhs and kindly share the articles with your friends. Thanks!

certai9nly man. I have already shared it with many of my friends, to use your site as a guide for learning or investing.

regards,

J.D.

Hi Shree,

I started reading your blogs from few days and finding it very helpful. I have commited some blunders in my financial planning and insurance. Have opted for traditional life insurance from LIC. Want to surrender the same. But before that want to take term insurance.

My current professional status is like I recently quit my job and currently not working. I have applied for the work visa of South Africa on my own and would be flying there probably next month and my plan is to work there for at least 5 years. But since I am not working currently would I be eligible for taking a term plan? What would be your suggestion to go at this?

Dear Dipak,

You can surely apply for a term plan based on your past ITRs or income proofs but company may or may not issue you a policy.

Kindly try with an Life insurance company of your choice.

Else, you can apply for term plan after getting a job.

Dear Readers,

Even I searched a lot and bit worried of CSR and after doing lots of research on this I came to following conclusion

1) Any company can reject your claim if you were not authentic and honest during policy purchase, no matter company CSR is 95% or 65% , if you were not true with you proposal form you claim would get rejected.

2) If company A with CSR 95% is ready to pay the claim then obviously company B with CSR 65% will also be ready to pay the claim same is true for rejection too.

3) And after all you’ll have to trust on any insurance company and you can’t do much. What you can do is to provide best and correct information of you to insurance company and undergo medical test.

4) Lastly I got a strength to go with company of my choice even with comparatively low CSR because of following clause.

“As per the recent amendment to Section 45 of the Insurance Act, If your policy is 3 yrs old, no matter what happens, the life insurance company will not be able to deny the claims. So, your life insurance company has only 3 years in hand to reject the policy based on any mis-representation or mis-statement. Once 3 policy years are completed then the life insurance company has to settle the claims and can not reject them.”

Thanks

Ashish

As per the amendment to section 45, your policy becomes incontestable after paying 3 annual premiums, i.e. only 2 years (and not 3 years) after you took the policy. So the insurer has only 2 years to reject the policy that too due to only any proven fraudulent action of the insured.

Dear Anuj ..Kindly go through this link (IRDA)..

Although I think CSR is not clear by IRDA yet but we can go by data available and so many others online Term plans are available of others companies so right plan taking consideration of of available facts must be taken in point.

I took online term plan of Bajaj Allianz

It has low claim settlement ratio, one should know before even thinking about this policy

Dear suresh,

Though claim ratio is important but it is not THE DECIDING FACTOR.

Not prudent to say to stay away.

(Note that I am not recommending any ONE term plan).

With the insurance amendment act making it difficult to reject claims after 3 years, I feel claim settlement ratio shouldn’t be as big an issue.

Of course, insurance companies can’t be expected to give everything on the platter. Nominees will have to fight.

But yes, it begins with making adequate disclosures at the time of policy purchase.

Dear Deepesh,

Agree with you.

“As per the recent amendment to Section 45 of the Insurance Act, If your policy is 3 yrs old, no matter what happens, the life insurance company will not be able to deny the claims. So, your life insurance company has only 3 years in hand to reject the policy based on any mis-representation or mis-statement. Once 3 policy years are completed then the life insurance company has to settle the claims and can not reject them.”

Hi,

can companies reject the Term insurance if we have Diabetics or BP and is it make sense to take term plan at the age of 40 and what is the best term insurance plan now?

Iam looking for aegon life- with cover of 1CR…please suggest on this and also I do have traditional LIC (Jeevan anand)do you want me to surrender that policy.

Dear Naveen..It depends on insurer’s underwriting policies, they may also charge extra premium (loading) for high risk profiles and issue policies.