A lot of taxpayers assume that agricultural income is fully tax-free in India. Well… that’s only partly true!

Agricultural income is indeed exempt from income tax under Section 10(1) of the Income-tax Act, 1961. But here’s the twist—there are certain situations where it can still sneak in and affect your overall tax liability, even though it isn’t taxed directly.

If you earn Salary, Business Income, or Professional Income alongside Agricultural Income, there’s an important concept you should know about: the Partial Integration Rule. This is exactly what decides whether—and how—your agricultural income quietly influences the tax you pay on your other income.

In this article, we’ll break down:

- Is agricultural income always tax-free?

- When does the Partial Integration Rule kick in?

- How is income tax actually calculated in such cases?

- A simple calculation example to make it click

- Frequently asked questions

Is Agricultural Income Taxable?

Generally, no—agricultural income isn’t taxed on its own, but that doesn’t mean it’s completely off the radar either.

Agricultural income is exempt from income tax under Section 10(1) of the Income-tax Act. However, “exempt” doesn’t mean “irrelevant.” In certain cases, your agricultural income still gets factored in—not to tax it directly, but to determine the tax rate that applies to your other taxable (non-agricultural) income. So while the amount itself stays untaxed, it can quietly push you into a higher tax bracket for the income you do pay tax on.

When does Partial Integration Rule apply?

The Partial Integration Rule doesn’t apply automatically to everyone—it only kicks in when both of these conditions are met at the same time:

- Your agricultural income exceeds ₹5,000 during the financial year, AND

- Taxable non-agricultural income exceeds the applicable Basic Exemption Limit.

If even one of these two conditions isn’t satisfied, the Partial Integration provisions simply don’t apply, and your agricultural income has no bearing on the tax rate for your other income.

| Condition | Applicable? |

|---|---|

| Agricultural Income above ₹5,000 | ✔ Required |

| Other taxable income exceeds Basic Exemption Limit | ✔ Required |

| Both conditions satisfied | Partial Integration applies |

The Government introduced Partial Integration mainly to ensure that taxpayers with substantial agricultural income and taxable non-agricultural income do not end up paying tax at a lower slab rate merely because agricultural income is exempt.

How is Income Tax calculated?

The formula behind this might sound technical, but it’s actually pretty straightforward once you break it down.

Here’s how it works:

Income Tax Payable =

Tax on (Other Income + Agricultural Income)

Minus

Tax on (Basic Exemption Limit + Agricultural Income)

In simple terms, you first calculate tax as if your agricultural income were added to your other income—this gives you tax at a higher slab rate. Then, you calculate tax on just the exemption limit plus the agricultural income, and subtract that from the first figure. What you’re left with is the actual tax you owe on your non-agricultural income, just calculated at a rate that reflects your total income level.

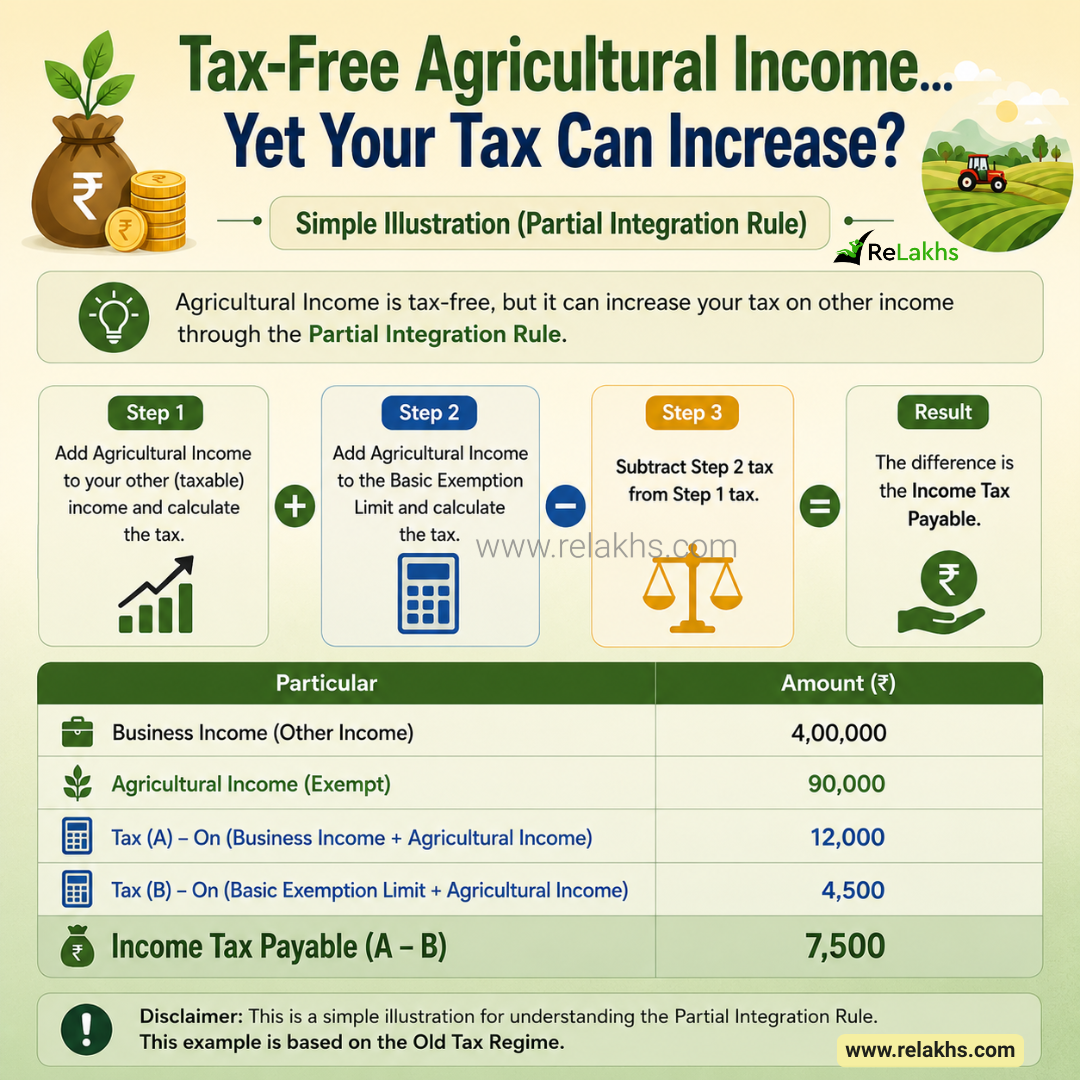

Partial Integration Rule – Example (Old Tax Regime)

Let’s put the formula into action with a simple example under the Old Tax Regime.

Assume Mr. Reddy has the following income for the year:

- Business Income: ₹4,00,000

- Agricultural Income: ₹90,000

Since his agricultural income is above ₹5,000, and his business income already exceeds the Basic Exemption Limit, the Partial Integration Rule kicks in here.

Step 1: Tax on total income (Business + Agricultural)

We first add both incomes together: ₹4,00,000 + ₹90,000 = ₹4,90,000.

- First ₹2,50,000 → Nil

- Remaining ₹2,40,000 @ 5% → ₹12,000

- Tax (A) = ₹12,000

Step 2: Tax on Basic Exemption Limit + Agricultural Income

Next, we add the Basic Exemption Limit and agricultural income: ₹2,50,000 + ₹90,000 = ₹3,40,000.

- First ₹2,50,000 → Nil

- Remaining ₹90,000 @ 5% → ₹4,500

- Tax (B) = ₹4,500

Step 3: Final tax payable

Now we simply subtract Step 2 from Step 1:

₹12,000 − ₹4,500 = ₹7,500

So, Mr. Reddy’s actual tax payable on his business income works out to ₹7,500—not the full ₹12,000 you’d get by just taxing his income at the slab rate, and not zero either, since his agricultural income still nudged him into a higher rate. Do note, this example skips Health & Education Cess, surcharge, and the Section 87A rebate to keep the calculation simple and easy to follow.

Key Takeaway: Agricultural Income continues to remain exempt. However, it can indirectly increase your income tax liability by influencing the tax slab or tax rate applicable to your taxable income. Proper records should be maintained to substantiate Agricultural Income if required by the Income Tax Department.

Frequently Asked Questions (FAQs)

Is Agricultural Income always tax-free? – Generally yes. However, it may affect the tax calculation on your non-agricultural income through Partial Integration.

Does Agricultural Income become taxable if it exceeds ₹5,000? – No. The ₹5,000 limit is only one of the conditions for applying Partial Integration.

Can salaried employees also have Agricultural Income? – Yes. If a salaried individual also earns agricultural income, Partial Integration provisions may apply if the prescribed conditions are satisfied.

Should agricultural income be reported in your Income Tax Return? – Absolutely! If your agricultural income exceeds ₹5,000, report it under Schedule EI (Exempt Income) of your Income Tax Return. While agricultural income is generally tax-exempt, disclosing it correctly is important and may be relevant for tax computation where the Partial Integration Rule applies.

Conclusion

Agricultural Income is one of the most misunderstood areas of income tax law. While it enjoys tax exemption under Section 10(1), taxpayers having both agricultural and non-agricultural income should clearly understand the Partial Integration provisions to avoid confusion while computing their tax liability.

Understanding these rules can also help you file your Income Tax Return correctly and avoid unnecessary notices or mistakes.

Continue reading:

- Capital Gains Tax Exemption Options on Sale of House or Plot | Latest Rules

- Income Tax Deductions FY 2026-27: Complete Guide to Old vs New Tax Regime

(Post first published on : 15-July-2026)

Join our channels