It has become almost next to impossible to live Debt-free. Most of us cannot buy homes or fund kids’ education or buy a car by paying up-front in cash.

As a thumb rule, 30 to 40% of your income can be used to pay long-term debts (loans). This is one of the metric that most of the lending institutions consider while assessing the creditworthiness of a loan applicant (borrower).

Sometimes avoiding debt totally may not be a smart idea, as you may end up using your cash reserves which are otherwise can be used to meet any unforeseen emergencies.

So, Is there a Good Debt? Or All debts are bad? When should I go for loans?

Debt is not always a negative thing. If managed well, it helps to leverage your future income to build assets and reach your financial goals. Debt can be good or bad , depending on how it is being used. The most important consideration when buying on credit or taking out a loan is whether the debt incurred is good debt or bad debt.

What is Good Debt?

If you take a loan to build assets (or) use it to make more money then those loans can be termed as GOOD DEBT. It includes anything that you NEED to buy but cannot afford to pay for up-front in cash.

Here, affordability is also important. You may NEED to buy house, but if you cannot afford to pay EMIs then do not go for debt (even if it is a good debt).

If a loan has any or all of the following features then it can be termed as a good debt.

- Good Debt should generate value and create more wealth for you

- It should create a positive stream of cash flows for you

- If it can offer a tax advantage then it is well and good

Examples:

- Home Loans

- Education Loans

- Business Loans

- Vehicle Loans ( this can be both good or bad debt)

One of my friend’s brother had purchased a property in United States. He had taken a home loan (though he can afford to pay for in cash). Reason being, the rate of interest on loan is 4%. The important point here is “Opportunity Cost” (if you chose one alternative over another, then the cost of choosing that alternative is an opportunity cost.)

He is very confident that he can invest his cash reserves in some other investment avenues, which may generate returns that are more than 4%.

What is Bad Debt?

Bad debt includes debt you have taken on for things you don’t need or can’t afford. These type of loans are generally used to buy ‘consumption’ or depreciating assets.

Examples:

- Credit card rollover

- Personal Loans

- Vehicle Loans

- Vacation loans

How to manage my Debt – Putting it into Practice

- Do not repay part of your debt by taking some more debt. Do not take new loans to close existing loans

- If you receive a windfall or bonus then try to close high-cost debts first. High-cost loans (bad debt) can be personal loans or Credit card dues

- These days it’s far too easy to spend more than you can afford, especially when you pay by credit card. Five digit incomes and easy access to loans/plastic money may induce you to splurge or go for loans. But, be prudent in using your credit cards.

- Take loans when you want to buy something ESSENTIAL and can afford to pay EMIs

- Acquire loans when you are confident of receiving future income. Example can be – Business loans

- Invest in yourself in order to increase your earnings potential. Example- Education loans.

- Do not take high-cost loans from money-lenders and finance companies

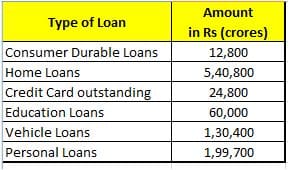

RBI’s data on Total Outstanding Loans

Below is the data on Total retail credit (loans) extended by banks as of March 2014.

(You may like visiting my post on “RBI’s data on Financial Savings of the Households.“)

Think twice before opting for any kind of loans. Analyze if they are good debt or bad debt for you? Too much debt (even if it is GOOD DEBT) can hurt your overall financial health.

(Image courtesy of iosphere at FreeDigitalPhotos.net)

Join our channels

Good one. Can you please share your contact details on – 8978544550. i need your help.

Dear Adinarayana,

You may contact me @ sreekanth [at] relakhs.com

Good one 🙂

Thank you Sulatha.

Hi Sri,

Nice information u had shared.

Thnx

Thank you Santhosh.