Joint bank accounts are often opened by spouses, parents and children, or business partners. But many people assume that the first account holder automatically gets the tax benefit, or that the TDS deducted by the bank decides who should report the income.

In reality, taxation depends on who actually owns the money, not just on whose name appears first in the account.

So before we look at the rules, let’s clear one common myth: just because it’s a joint account does not mean money, taxes, or benefits are split equally. The Income Tax Department looks at the source of funds and the actual contributor of the capital. That is what determines ownership, and in turn, the tax liability.

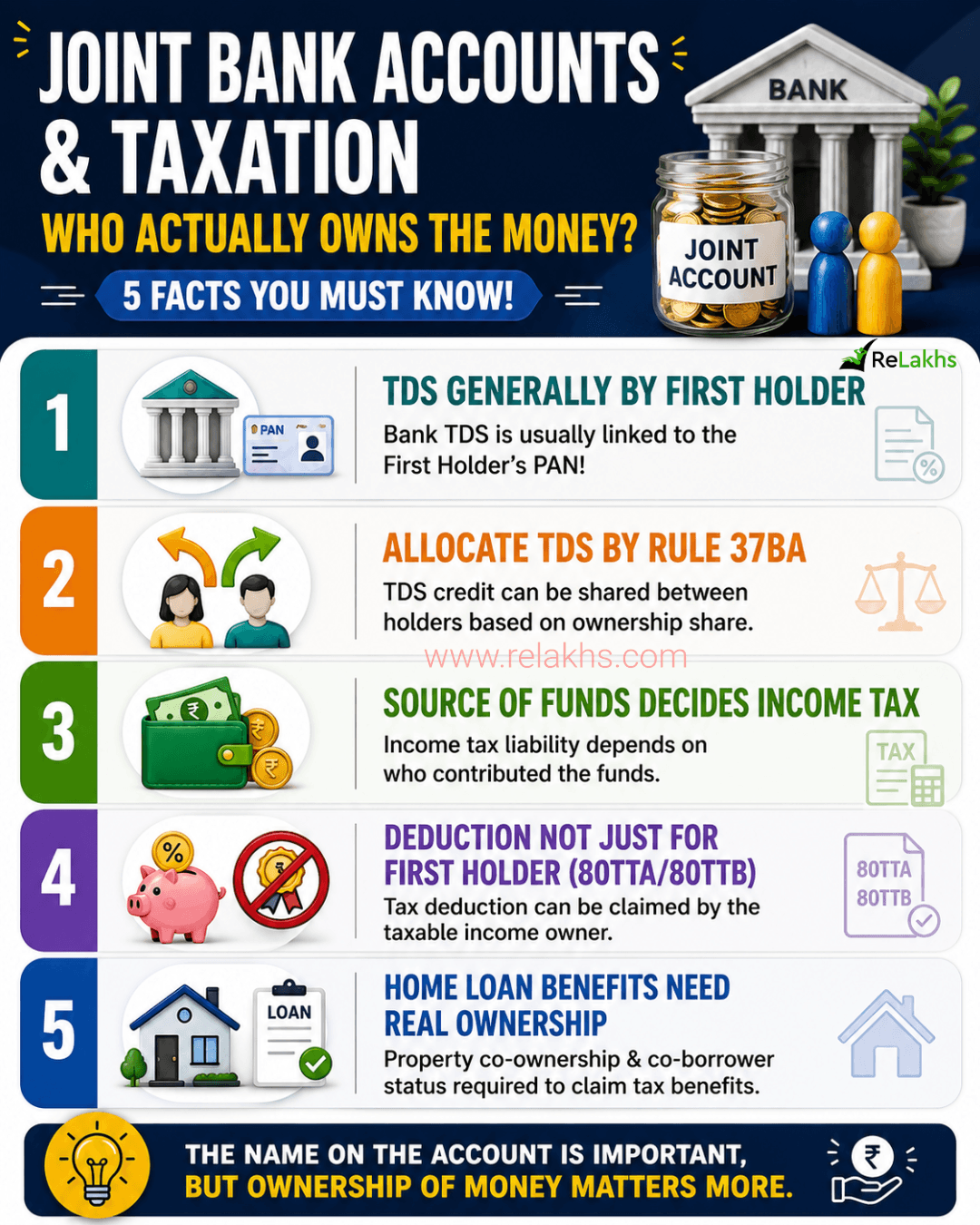

Let us understand five important tax and home-loan-related rules applicable to joint bank accounts.

Rule #1 – TDS is generally deducted in the name of the First Account Holder

If a bank deducts TDS on the interest earned from a joint fixed deposit or other interest-bearing deposit, the TDS is generally deducted against the PAN of the first (primary) account holder.

For example, let us assume a husband and wife have a joint FD that earns interest of ₹60,000 during a financial year. If the husband is the first holder, the bank will generally report the interest income and TDS against his PAN.

As a result:

- The TDS credit will usually appear in the husband’s Form 26AS and AIS.

- The wife may not see this TDS credit in her tax records.

Many taxpayers wrongly assume that because the TDS appears in the first holder’s PAN, the entire interest income must also be taxed in that person’s hands. This is not necessarily correct. TDS reporting and taxation of income are two different things.

Did You Know?

Most joint FD holders assume TDS must always be deducted in the first holder’s PAN. However, under Rule 37BA, joint holders can request the bank to allocate TDS credit according to their actual ownership/share in the deposit, subject to the bank’s procedures and documentation requirements

Rule #2 – TDS Credit Can Be Allocated Based on Actual Ownership (Rule 37BA)

The Income-tax Rules provide a solution when the income from a joint deposit belongs to more than one person.

Under Rule 37BA, TDS credit can be claimed by the person who is actually taxable on the income, subject to prescribed conditions.

For example:

- Husband contributes ₹6 lakh (60%)

- Wife contributes ₹4 lakh (40%)

- Interest earned during the year is ₹10,000 on a Rs 10 Lakh joint deposit

In this case, the interest income belongs to both account holders in the ratio of 60:40. Accordingly, the husband’s share of interest is ₹6,000 and the wife’s share is ₹4,000.

To ensure that the corresponding TDS is also allocated in the same ratio, the joint account holders may submit a declaration to the bank before TDS is deducted, requesting the bank to split the interest income and TDS credit based on their actual contribution ratio.

| Scenario (60:40 Contribution) | First Holder (Husband) | Second Holder (Wife) |

| Capital Contributed | ₹6,00,000 (60%) | ₹4,00,000 (40%) |

| Interest Income Earned | ₹6,000 | ₹4,000 |

| Default Bank Reporting (No Rule 37BA) | 100% Interest & TDS reflects in AIS/26AS | 0% reflects in AIS/26AS |

| After Rule 37BA Declaration | 60% TDS credited | 40% TDS credited |

It is advisable to submit this declaration at the time of opening the deposit or well before the end of the financial year and maintain records of the source of funds and contribution ratio. Do note that the operational process and documentation requirements may vary from one bank to another.

Rule #3 – Interest Income Depends on the Source of Funds

This is one of the most misunderstood parts of joint bank accounts. Just because someone’s name is added to the account does not mean the interest income automatically becomes taxable in that person’s hands.

The real question is simple: who actually contributed the money? In most cases, interest income follows the ownership of the funds, not the order of names on the account.

For example, if the husband put in the full deposit amount, the interest may be taxable in his hands even if the account is joint with his wife. If the wife contributed the full amount, then the interest may be taxable in her hands instead. And if both contributed equally, the interest can generally be divided equally for tax purposes.

So when you file your income tax return, the focus should be on the source of funds and beneficial ownership, not just whose name comes first in the bank account.

Rule #4 – Who Can Claim Deduction Under Section 80TTA or 80TTB?

A common myth is that only the first account holder can claim the tax deduction on interest income, but that is not always true. The deduction should generally go to the person who is actually taxed on that interest income.

Section 80TTA is available to eligible individuals and HUFs on savings account interest, within the prescribed limit. Section 80TTB is available to eligible senior citizens on specified interest income, also subject to the prescribed limit.

For example, if a joint savings account earns ₹15,000 in interest and the wife is the real owner of the funds, then the interest may be taxable in her hands. In that case, she may be able to claim the deduction even if she is not the first account holder.

So the simple rule is this: the deduction follows the taxable income, not just the order of names in the account.

Key Takeaway: Tax deductions follow the taxable income, not the banking sequence. If you are reporting the interest income in your ITR, you are the one eligible to claim the Section 80TTA/80TTB deduction.

Note: Deductions under Section 80TTA and 80TTB are available only if you choose the Old Tax Regime. If you opt for the New Tax Regime, these deductions cannot be claimed.

Rule #5 – A Joint Bank Account Does Not Automatically Create Home Loan Tax Benefits

Many couples pay their home loan EMIs from a joint bank account, and it is easy to assume that both account holders can automatically claim the tax benefit. But that is not how it works.

The tax department looks at three things: who owns the property, who is the borrower, and who actually repays the loan. In other words, the joint account is only the payment route — it does not decide the tax benefit by itself.

For example, if husband and wife are both co-owners and co-borrowers, they may be able to claim benefits based on their respective contributions, subject to the law. But if the EMI is paid from a joint account and only one person owns the property, the other account holder does not automatically get the deduction. Similarly, if only one person is the borrower and eligible owner, the other person cannot claim the benefit just because the money is flowing through a joint account.

So the simple rule is: a joint bank account does not decide home loan tax eligibility — ownership and borrowing status do.

To claim Home Loan Tax Benefits (Principal/Interest), ensure you tick all 3 boxes:

- [ ] Co-Owner: Your name must be on the Property Title Deed.

- [ ] Co-Borrower: Your name must be on the Bank Loan Sanction Letter.

- [ ] Contributor: You must be funding the Joint Account for EMIs in proportion to your ownership share.

Conclusion

Many taxpayers assume that the first account holder automatically gets the TDS credit, tax benefits, or even home loan deductions associated with a joint bank account. However, tax laws look beyond the order of names in the account.

In most cases, what matters is the actual ownership of funds, the source of investment, property ownership, borrower status, and the individual’s contribution towards repayment.

A joint bank account may make banking operations convenient, but it does not automatically determine who is taxable on the income or who is eligible to claim tax benefits.

Therefore, before opening a joint deposit, claiming interest deductions, or servicing a home loan through a joint account, it is worth taking a few minutes to understand the tax implications. A small oversight today can lead to unnecessary tax notices, disputes over TDS credits, or loss of legitimate tax benefits tomorrow.

Remember, in taxation, the name on the account is important, but the ownership of money is often even more important.

Continue reading:

- Who gets the Joint Bank Account Monies if one Account Holder dies?.

- Types of Joint Accounts in Banks

- 6 Banking Rules Every Bank Customer Should Know in 2026

(Post first published on : 24-June-2026)

Join our channels