We interact with banks almost every day — from managing our savings accounts and fixed deposits to taking loans or making digital payments. But many of us don’t really know some key banking rules that could impact how we handle our money and make financial decisions.

In fact, some of the most common banking assumptions people have are actually misconceptions.

With the landmark RBI Responsible Business Conduct (RBC) Directions 2026 set to kick in this July, the rules of the game are changing in favor of the customer. Here are 6 critical banking facts you need to know to protect your hard-earned money and stop being “sold” products you don’t need.

6 Banking Rules Every Bank Customer Should Be Aware Of

Let’s look at six important banking facts every bank customer should know.

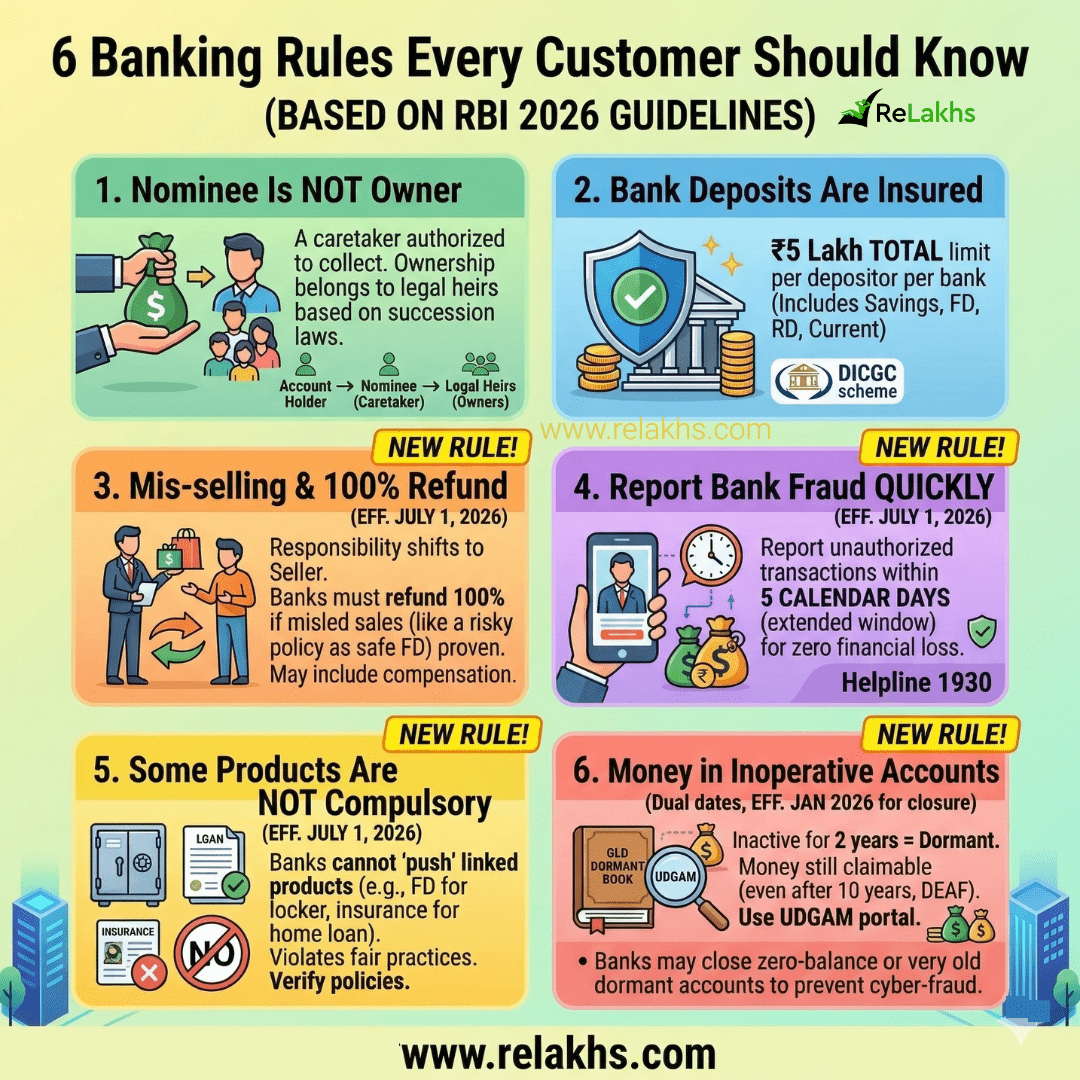

1. A Nominee Is Not the Owner of the Money

Many people believe that if they add a nominee to their bank account, the nominee automatically becomes the owner of the money in that account.

But that’s not how it works.

A nominee is essentially a caretaker of the money, not the legal owner. If the account holder passes away, the bank may release the funds to the nominee. However, the nominee does not automatically get ownership rights over that money.

The actual ownership of the funds belongs to the legal heirs of the deceased account holder, as per applicable succession laws. Any further dispute over that money will be a private matter between the nominee and the legal heirs, not the bank.

In simple terms, the nominee only collects the money from the bank and is responsible for passing it on to the rightful legal heirs (if the nominee is not one of them).

| Scenario | Bank’s Status | Nominee’s Status |

| Money is in the Account | Liable to the account holder. | No rights yet. |

| Account Holder Passes Away | Obligated to pay Nominee | Authorized to collect. |

| Bank pays the Nominee | Account Closed/Settled. | Liability to Heirs Begins. |

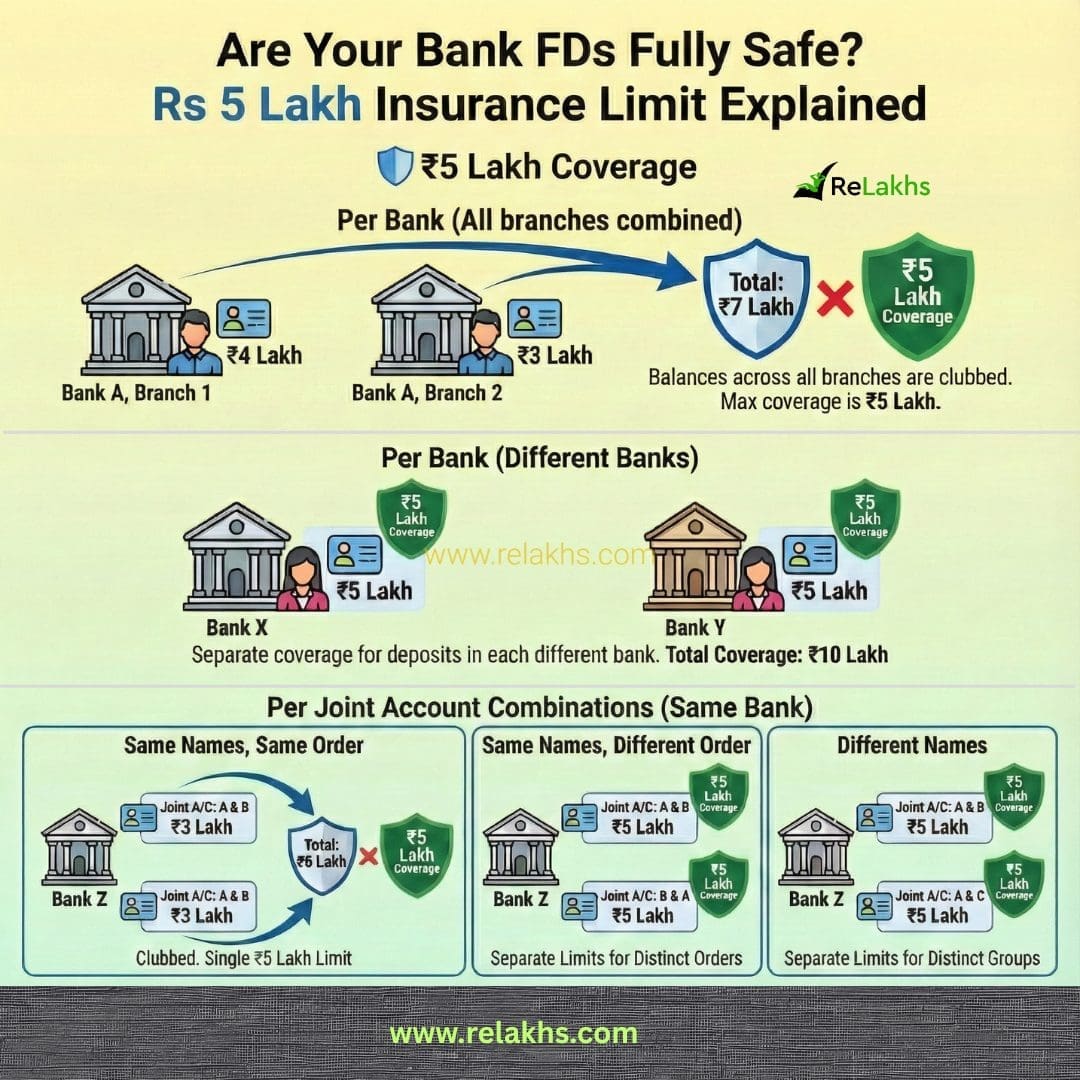

2. Bank Deposits Are Insured Only Up to ₹5 Lakh

Here’s another important banking rule that many people are not fully aware of.

Deposits in Indian banks are insured under the Deposit Insurance and Credit Guarantee Corporation (DICGC) scheme. Currently, bank deposits are insured up to ₹5 lakh per depositor per bank.

This includes all types of deposits such as:

- Savings accounts

- Fixed deposits (FDs)

- Recurring deposits (RDs)

- Current accounts

One important point to remember is that the ₹5 lakh limit applies to the total deposits in one bank, not to each individual account.

So if you have multiple accounts like savings accounts and fixed deposits in the same bank, the combined insurance protection will still be limited to ₹5 lakh.

3. Mis-selling & 100% Refund Rule

When you visit a bank branch, you might sometimes be offered various financial products like insurance policies or investment plans. In some cases, these products are presented in a way that makes them sound similar to fixed deposits or safe investment products.

The RBI’s new Responsible Business Conduct (RBC) Directions, 2026, completely change the rules for how banks sell insurance and other products. Starting July 1, 2026, the responsibility shifts from “buyer beware” to “seller responsible.”

If a bank employee misleads you—for example, by selling a risky insurance policy as a “safe FD”—and mis-selling is proven, the bank is legally mandated to refund 100% of your money and may even have to pay additional compensation for your losses.

If a bank insists an insurance policy is mandatory for an FD, ask them to show you the ‘Product Suitability’ document required under the 2026 RBC rules.

4. What to Do If Bank Fraud Happens

Cyber frauds and online banking scams have risen sharply in recent years. If you ever spot an unauthorized transaction or fraudulent withdrawal from your account, report it to your bank immediately.

As per RBI guidelines, if the fraud is reported within three days, you may not have to bear any financial loss—provided the fraud didn’t happen due to your negligence. That’s why quick reporting is crucial in such cases.

Starting from 1 July 2026, the new guideline extends this window to five calendar days to report the scam to your bank and the National Cyber Crime Helpline (1930).

5. Some Banking Products Are Not Compulsory

Many bank customers believe certain banking requirements are mandatory, even when they are not. Banks have long used high-demand services like lockers or home loans to “push” other products, but the new rules (effective July 2026) make it clear that this is a violation of fair practices.

For example:

- A minimum deposit is not always mandatory to open a bank account. Many banks offer zero-balance accounts.

- A huge fixed deposit is not compulsory to obtain a bank locker. (However, banks can mandate a small “Caution Deposit” (FD) covering 3 years of rent plus break-open charges for new customers to ensure rent recovery.)

- Home loan insurance is not mandatory when taking a housing loan.

However, customers are sometimes told that these are compulsory, which may lead to unnecessary financial commitments. It is always advisable to ask questions and verify the bank’s policies before agreeing to such conditions.

6. Money in Inoperative Bank Accounts Is Not Lost

If a bank account remains inactive for 2 years, banks usually classify it as an inoperative or dormant account. This simply means there have been no customer-initiated transactions during that period.

If the money in such accounts remains unclaimed for 10 years, the balance may be transferred to the Depositor Education and Awareness Fund (DEAF) maintained by the RBI. Even after the transfer, the account holder or the legal heirs can still claim the funds anytime by approaching the bank and completing the required process.

The best practice is to use the UDGAM portal to locate any forgotten funds and initiate a claim immediately, as the government is currently running a high-priority campaign called “Aapki Poonji, Aapka Adhikar” to fast-track these payouts. The RBI has however warned that starting January 2026, banks may move to close or restrict access on zero-balance or dormant accounts that remain inactive for extended periods to prevent them from being used for cyber-fraud.

We use banking services almost every day, but many of these simple rules are not widely known. Understanding them can help you avoid confusion, ask the right questions at the bank, and make smarter financial decisions. After all, when it comes to money matters, a little awareness can go a long way.

Continue reading:

- ₹4 Crore Gold Locker Fraud: Are Your Bank Locker Valuables Really Safe?

- Latest TDS Rates Tax Year 2026-27 – Complete Chart

(Post first published on : 09-Mar-2026)

Join our channels

Good information