Many retirees in India face a simple problem: they may own a house worth ₹50 lakh, ₹1 crore, or even more, but still struggle to pay their monthly bills after retirement. In other words, they are asset rich but cash poor.

A reverse mortgage is made for this exact situation. It lets senior citizens turn part of their home’s value into regular income without selling the house or moving out. In simple terms, the house keeps working for you while you continue living in it.

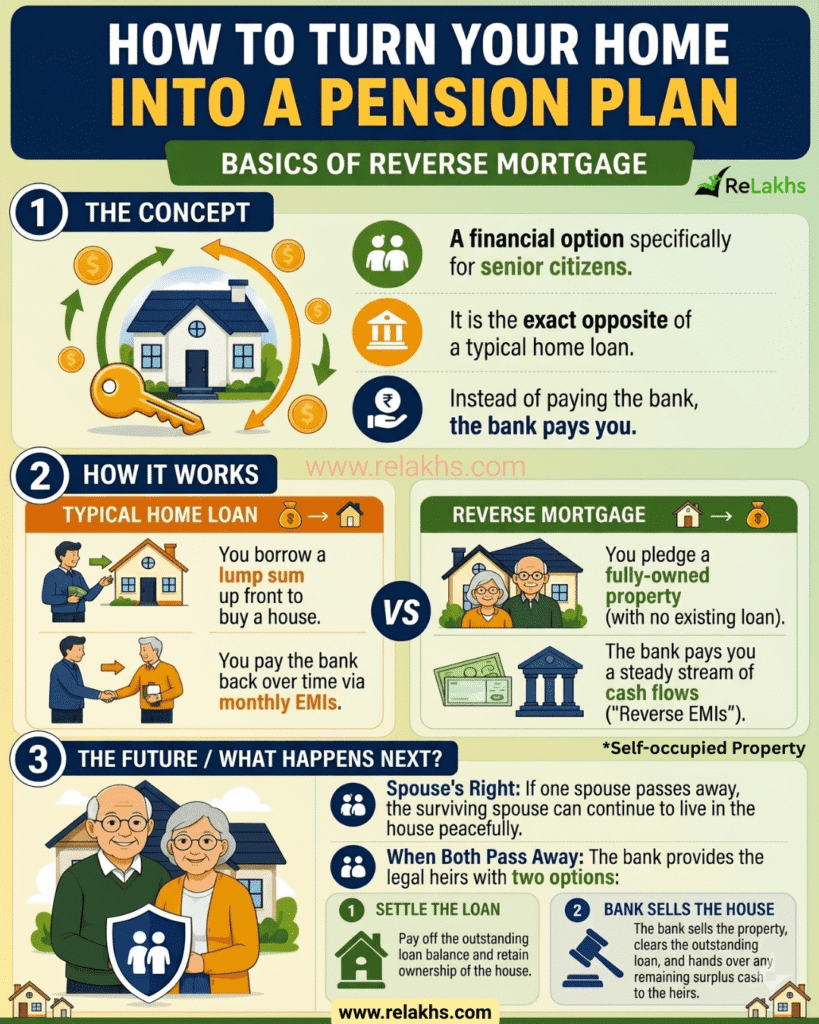

Although Reverse Mortgages have been available in India for several years, very few people understand how they work, and adoption remains extremely low compared to Western countries. Let us understand the concept in simple terms.

What is a Mortgage?

To understand a reverse mortgage, start with a normal mortgage. A mortgage is simply when you pledge your property (like a house) as security for a loan.

Example:

Mr. A wants to buy a house worth ₹60 lakh. He puts ₹10 lakh from his savings and takes ₹50 lakh from a bank. The bank keeps the house as collateral until he repays the loan. This is called a mortgage.

In a normal home loan:

- The bank gives you money.

- You repay through EMIs.

- The loan balance goes down over time and your equity (ownership share) in the house goes up.

What is a Reverse Mortgage?

A reverse mortgage works in the opposite direction of a normal home loan. Instead of you paying EMIs to the bank, the bank pays you.

In this arrangement, a senior citizen pledges their self-occupied home (residential) and receives regular payments, a lump sum, or a combination of both. The homeowner continues living in the house for life, and there is usually no need to make monthly repayments during the loan tenure.

Reverse Mortgage | Simple Illustration

Assume:

- Age of homeowner: 65 years

- Residential Self-occupied Property value: ₹1 crore

- House fully owned and free from existing loans

The bank may offer a reverse mortgage, but usually not the full ₹1 crore. It considers only a portion of the property value based on its internal valuation (Loan to Value Ratio).

The bank may provide:

- Monthly income

- Quarterly income

- Annual income

- Partial lump-sum for specific needs

The homeowner continues living in the house, and unlike a regular home loan, no EMI is required.

Example : Meet Mr. Ramesh, a retiree who owns a ₹1 crore flat in Mumbai but has a tiny pension and high medical bills. Instead of selling his home, he gets a reverse mortgage from a bank. The bank agrees to pay him ₹20,000 every month for the next 15 years, and Mr. Ramesh never has to pay a single monthly EMI. He and his wife continue living in their home peacefully with their expenses fully covered.

Years later, after both pass away, the total loan balance (with accumulated interest) stands at ₹85 lakh. The bank sells the flat at its current market value of ₹1.5 crore, recovers the ₹85 lakh debt, and legally hands over the remaining ₹65 lakh in cash straight to their daughter.

Traditional Home Loan Vs Reverse Mortgage

| Particulars | Traditional Home Loan | Reverse Mortgage |

|---|---|---|

| Purpose | To purchase or construct a house | To generate income from an already owned house |

| Who Receives Money? | Borrower receives a lump-sum loan from the bank | Homeowner receives periodic payments from the bank |

| Monthly Payments | Borrower pays EMIs to the bank | Bank pays income to the homeowner |

| Property as Security | House is mortgaged to the bank | House is mortgaged to the bank |

| Outstanding Loan Balance | Decreases over time as EMIs are paid | Increases over time as payments and interest accumulate |

| Ownership of Property | Remains with the borrower | Remains with the homeowner during his/her lifetime |

| Right to Stay in the House | Borrower continues to live in the house | Homeowner continues to live in the house |

| Target Audience | Individuals looking to buy a home | Senior citizens seeking additional retirement income |

| Repayment During Lifetime | Mandatory EMI payments | Generally, no EMI payments required |

| What Happens After Death? | Loan is usually repaid by legal heirs or from insurance proceeds | Heirs may repay the outstanding loan and retain the property, or the property may be sold by the bank to recover dues |

Eligibility Criteria for Reverse Mortgage in India

While specific terms vary slightly by bank, the Reserve Bank of India (RBI) sets down these standard criteria:

- Age Requirement: The primary homeowner must be 60 years or older. If applying jointly with a spouse, the spouse must typically be at least 55 years old.

- Property Type: The property must be residential and self-occupied (you must actually live there, not rent it out).

- Clear Title: The property must be legally owned by you with a clear, marketable title free from existing loans or legal disputes.

- Property Life: The house must have a reasonable remaining lifespan (usually a minimum of 20–25 years) determined by a bank valuer.

What Happens After the Borrower’s Lifetime?

This is one of the most misunderstood parts of a reverse mortgage. After the borrower (or the surviving spouse, in a joint loan) passes away, the legal heirs have two main options:

Option 1: Repay the loan and keep the property – The heirs can repay the outstanding amount along with accumulated interest and retain ownership of the house.

Option 2: Let the property be sold – If the heirs do not want to repay, the lender can sell the property. The bank recovers its dues, and the remaining balance goes to the legal heirs. So, the bank does not automatically become the owner. The legal heirs continue to have rights and choices.

Banks Offering Reverse Mortgage in India

Several public sector banks and housing finance companies offer reverse mortgage products, including:

- State Bank of India (SBI)

- Punjab National Bank (PNB)

- Bank of Baroda

- Central Bank of India

- Union Bank of India

- IDBI Bank

- Axis Bank

- Various Housing Finance Companies (like LIC Housing Finance)

However, availability, eligibility norms, and product features can change over time. So, if you are interested, check the latest terms directly with the respective lender.

Taxation of Reverse Mortgage

Under Section 10(43) of the Income Tax Act, the periodic amounts received by a senior citizen under a reverse mortgage scheme are treated as a loan loan receipt, not income. Therefore, they are 100% exempt from income tax.

Also, simply mortgaging your property under a reverse mortgage does not trigger capital gains tax. Capital gains may come into the picture only if the property is eventually sold.

Why Is Reverse Mortgage Not Popular in India?

Even though reverse mortgage has been available for many years, it has not gained much traction in India. Several key factors explain this.

1. Emotional attachment to property: For many Indian families, a house is not just an asset. It is seen as a legacy for children and grandchildren. Many retirees hesitate to use their home to generate retirement income.

2. Desire to leave inheritance: Indian parents often prioritize passing property to their children. Reducing the value available to heirs is usually viewed negatively.

3. Lack of awareness: Many people simply do not know that this product exists. Even financially educated individuals may not understand how a reverse mortgage works.

4. Misconceptions: Common myths include-

- The bank will take the house immediately.

- The borrower loses ownership rights.

- Children permanently lose inheritance rights.

These beliefs discourage people from trying it.

5. Lower loan-to-value ratios: Banks do not lend the full market value of the property. As a result, expected monthly payouts may be lower than what homeowners expect. Sometimes, the monthly payout can be capped.

6. Family and social factors: In India, elderly parents often live with children or expect family support. This reduces the demand for independent retirement income solutions like reverse mortgage.

Final Thoughts

A reverse mortgage is a highly practical, secure financial tool—but it is not a one-size-fits-all miracle. For some retirees, it can significantly improve financial independence and quality of life after retirement. For others, the desire to preserve the property for future generations may be more important than the income it provides.

The key is to understand the concept clearly and check whether it fits your retirement goals, family situation, and financial needs.

A home is not just a place to live—it can also be a valuable financial asset when used wisely.

Continue reading:

- Best Pension Schemes in India (2026) – EPS, NPS, APY Explained

- Lump sum Investment options for Retirees/Senior Citizens | Where to invest my Retiral benefits to get Regular Income?

(Post first published on : 08-June-2026)

Join our channels