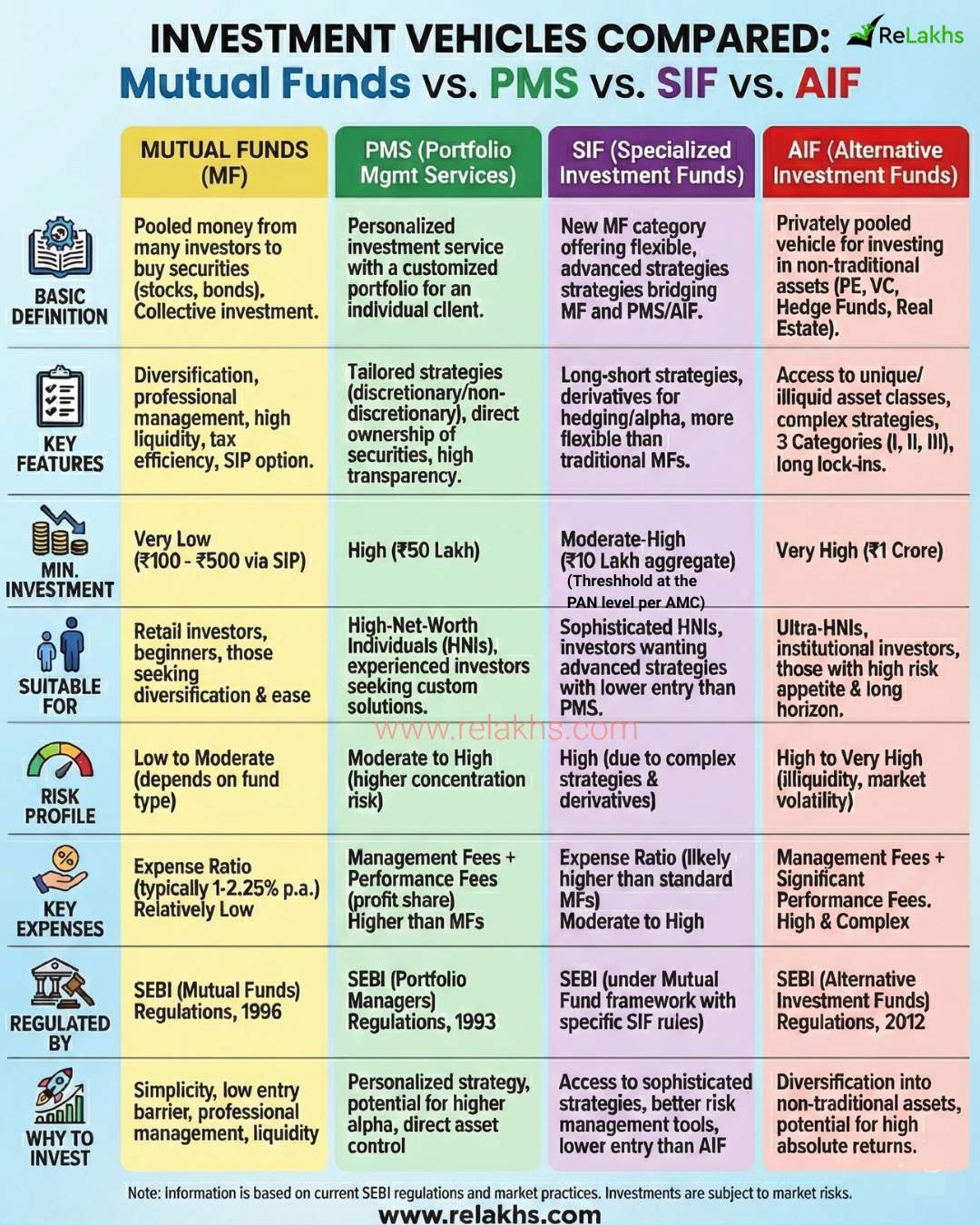

India’s investment world has changed a lot in the last ten years. For a long time, most retail investors depended on Mutual Funds to grow their money, while High Net Worth Individuals (HNIs) usually jumped straight to Portfolio Management Services (PMS) or more advanced Alternative Investment Funds (AIFs).

But there was always a big gap in between — ordinary retail limits on one side, and very high entry barriers for the ultra-wealthy on the other. To fill that space, SEBI introduced a new bridge category: Specialised Investment Funds (SIFs), which many people are now calling the “new asset class.”

Now, with Mutual Funds, PMS, SIFs, and AIFs all in play, things are a bit more layered. The real question is: which one actually fits your situation? Picking the right option comes down to understanding how much you want to invest, how much flexibility you need, how much risk you’re comfortable with, and how transparent you expect the structure to be.

Should you invest through Mutual Funds, PMS, SIF or AIF?

India’s investment world isn’t just about Mutual Funds anymore. Today, you have four main professionally managed options:

- Mutual Funds (MF) – The retail cornerstone

- PMS (Portfolio Management Services) – Personalized customization

- SIF (Specialised Investment Funds) – The modern hybrid asset class

- AIF (Alternative Investment Funds) – The ultra-HNI playground

Each one serves a different type of investor, based on your capital, risk appetite, and how much customization you want.

1. What is a Mutual Fund?

Definition: A Mutual Fund pools money from many investors and invests in securities like:

- Equities

- Bonds

- Money market instruments

- Gold ETFs

- REITs / InvITs

Key Characteristics:

- Diversified portfolio

- Professionally managed

- High liquidity

- Low minimum investment

- Ideal for retail investors

Minimum Investment: You can start with SIPs as low as ₹100 or ₹500.

Why it works for most people: Mutual Funds let lakhs of investors collectively buy a diversified portfolio of stocks, bonds, or money-market instruments. Regulated under SEBI (Mutual Funds) Regulations, 1996, they offer daily liquidity, strict expense caps, and a very democratic way to build long-term wealth through SIPs. For most retail investors, this remains the most practical way to invest systematically for goals like retirement, children’s education, or long-term wealth creation.

2. What is PMS (Portfolio Management Services)?

Definition: PMS offers customized portfolio management for individual investors. Unlike Mutual Funds, where assets are pooled into a single corporate structure, in a PMS the securities are owned directly by you. Your money goes into an isolated demat account, and stocks are bought and sold directly on your behalf under SEBI (Portfolio Managers) Regulations, 1993.

Types of PMS:

- Discretionary PMS: The portfolio manager makes and executes investment decisions on your behalf without needing your prior approval for each trade.

- Non-discretionary PMS: The manager suggests investment ideas, but you must approve and execute each trade before it happens.

- Advisory PMS: The manager only provides investment recommendations and analysis, without executing any trades for you.

Minimum Investment: ₹50 lakh (SEBI-mandated).

Suitable For:

- HNIs

- Investors who want customized portfolios

- Investors comfortable with concentrated bets

Why PMS? You get direct ownership, tailored themes, and full transparency. But you also take on higher stock concentration risk compared to diversified Mutual Funds. PMS is ideal if you have enough capital and want a portfolio built specifically around your preferences.

What is SIF (Specialised Investment Fund)?

Definition: SIF is a new category introduced by SEBI under the Mutual Fund framework. It allows fund houses to offer sophisticated strategies that aren’t usually available in regular mutual funds, such as:

- Long-short equity: A strategy that buys (goes long on) stocks expected to rise while simultaneously selling short (going short on) stocks expected to fall.

- Market neutral: A strategy designed to eliminate exposure to overall market movements, aiming to profit from stock-specific gains regardless of whether the market goes up or down.

- Hedging strategies: Techniques used to reduce or offset potential losses in an investment by taking an opposite position in a related asset.

- Derivative-based strategies: Investment approaches that use financial derivatives like futures, options, or swaps to gain exposure, manage risk, or speculate on price movements.

Minimum Investment: ₹10 lakh aggregate investment (this ₹10 Lakh threshold at the PAN level per AMC)

Suitable For:

- Experienced investors

- Sophisticated HNIs

- Investors looking for advanced strategies

Why SIFs? SIFs bridge the gap between Mutual Funds and PMS/AIF. Think of SIFs as a middle lane for affluent investors who don’t meet the ₹50 Lakh PMS threshold but want more edge than standard long-only funds. They get access to advanced risk-management tools and alpha opportunities, including tactical strategies like long-short equity and unhedged derivative positioning (up to 25% of the portfolio).

What is AIF (Alternative Investment Fund)?

Definition: AIFs are privately pooled investment vehicles that invest in alternative assets. They are regulated under SEBI (Alternative Investment Funds) Regulations, 2012 and are divided into three categories:

- Category I: Venture Capital Funds, Angel Funds, Social Venture Funds

- Category II: Private Equity Funds, Debt Funds

- Category III: Hedge Funds and complex trading strategies

Minimum Investment: ₹1 Crore.

Suitable For:

- Ultra-HNIs

- Institutional investors

- Investors with high risk appetite

Why AIFs? AIFs are private structures built for ultra-HNIs, family offices, and institutional capital. They chase alpha in non-traditional, illiquid, and unlisted spaces, often using structural leverage and complex shorting setups.

Key Risks Investors Must Understand

Every investment vehicle comes with its own set of risks.

| Investment Vehicle | Key Risks |

|---|---|

| Mutual Funds | Market risk, fund manager risk, sector concentration risk (for thematic funds) |

| PMS | Concentration risk, stock selection risk, manager risk, liquidity risk |

| SIF | Derivatives risk, leverage risk, strategy execution risk, market volatility risk |

| AIF | Illiquidity risk, valuation risk, leverage risk, manager risk, regulatory risk |

“Think of taxation like this: Mutual Funds and SIFs give you a ‘tax shield’—the fund trades freely, and you only pay capital gains when you exit. PMS is more direct—every trade your manager makes hits your tax record as a realized gain or loss. AIF Categories I & II act as a pass-through, so the tax flows to you based on the asset. But AIF Category III is different—the fund itself gets taxed at the highest level, which can eat into returns before they even reach you.”

So, Which One Should You Choose?

- Mutual Funds – If you’re a retail investor, want simplicity, low entry, and daily liquidity.

- SIFs – If you’re experienced, have ₹10 lakh+, and want advanced strategies without jumping to PMS/AIF.

- PMS – If you’re an HNI with ₹50 lakh+ and want a customized, directly owned portfolio.

- AIFs – If you’re an ultra-HNI or institution with ₹1 crore+, high risk tolerance, and can handle lower liquidity and more complexity.

The right choice depends on your capital, risk appetite, and how much customization and sophistication you actually need.

Final Thoughts:

Mutual Funds remain the most suitable option for the vast majority of investors. PMS, SIF and AIF are specialized solutions designed for investors with larger portfolios, higher risk tolerance and a deeper understanding of financial markets. Investors should choose an investment vehicle based on suitability, not exclusivity.

Continue reading:

- Best Mutual Funds for 2026: Picking “Consistency Kings” Over Performance

- Best Pension Schemes in India (2026)

(Post first published on : 11-June-2026)

Join our channels