Buying insurance is easy. Getting your claim settled—that’s where the real test begins. For any policyholder, one of the biggest fears is having a claim rejected after years of paying premiums faithfully.

Most people don’t realize that after a certain period, the insurer loses the right to question old non-disclosures or misstatements. That cutoff is called the moratorium period. Let’s understand this clearly.

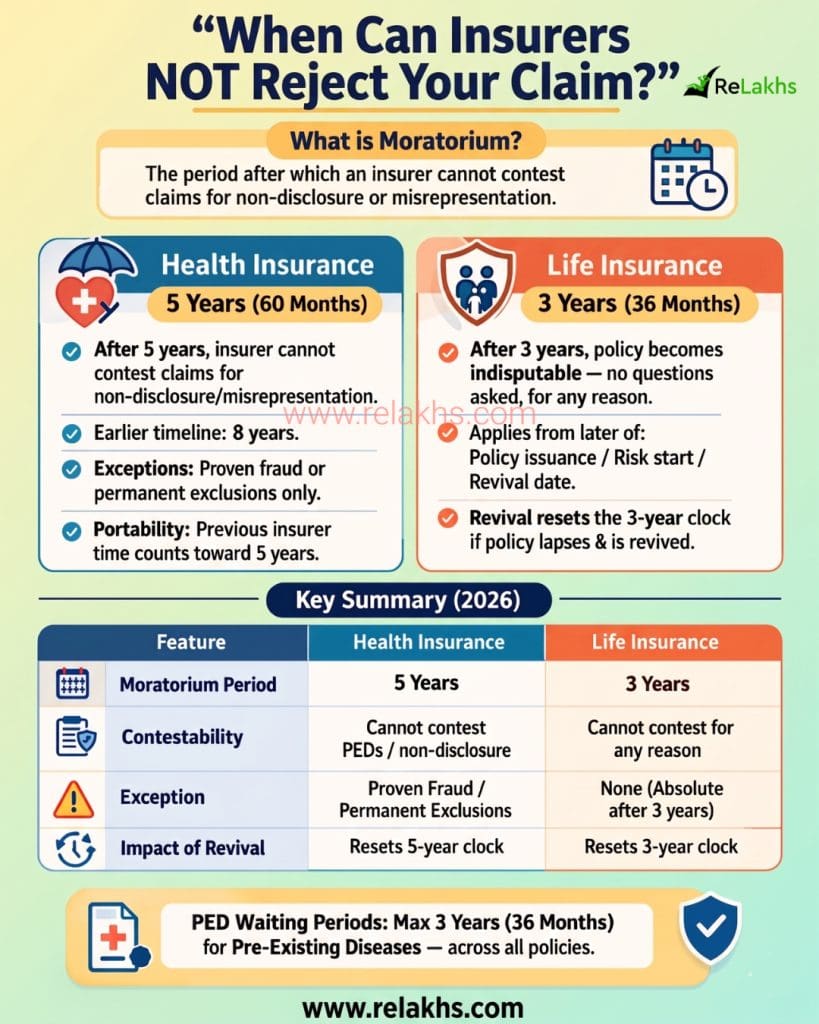

What is Moratorium Period in Insurance?

In simple terms, the Moratorium Period is like a “waiting period for the insurer.” It’s the time after which they can’t reject your claim based on non-disclosure or misrepresentation (except proven fraud in health insurance).

Once over, your policy becomes “indisputable” for info given at purchase.

Health Insurance Moratorium Period

Previously, the moratorium period for health insurance was 8 years. Under the newly implemented guidelines, this has been significantly reduced to 5 years (60 months).

- The Rule: After 5 years of continuous coverage, the insurer cannot reject a claim based on non-disclosure or misrepresentation.

- Exceptions: Claims can still be contested if there is proven fraud or if the claim falls under permanent exclusions mentioned in the policy.

- Portability Benefit: If you switch (port) your policy from one insurer to another, the time spent with the previous insurer counts toward this 5-year window.

- The Catch: If the policy lapses and you revive it, the 5-year clock resets from the date of revival.

- Sum Insured Hikes: If you increased your sum insured recently, remember that the “moratorium clock” for the additional amount started fresh on the day of the upgrade.

What is “Proven Fraud”? (Simple Explanation)

Proven Fraud, in simple terms: Insurers must prove all three elements at once:

- Intent to deceive: You knew the truth but hid it deliberately to get policy/claim.

- Active concealment: You actively hid facts (e.g., fake clean medical report from another lab).

- Financial gain: Done specifically to trick insurer into paying what they wouldn’t.

Simple Difference:

Non-disclosure (genuine mistake): Forgot a small surgery from 10 years ago? Protected after moratorium period.

Proven Fraud (intentional cheating): Buy policy while already hospitalized for serious illness? Never protected—especially in health insurance.

Mistakes may be forgiven after a few years. But intentional fraud is never protected!

Health Insurance | Reduction in PED Waiting Period

In another major win for policyholders, the maximum waiting period for Pre-Existing Diseases (PED) has been capped at 3 years (36 months) across all health insurance products. Earlier, many insurers had a 4-year waiting period.

Now, no one can make you wait longer than 3 years for coverage on diseases you had before buying the policy.

Life Insurance Moratorium Rule

Life insurance offers even stronger protection under Section 45 of the Insurance Act.

- The Rule: A life insurance policy becomes absolutely indisputable after 3 years (36 months).

- No Questions Asked: After this period, the insurer cannot call the policy into question for any reason—including fraud or misstatement.

- Timeline: The 3-year period starts from the later of:

- Policy Issuance

- Commencement of Risk

- Revival of the Policy

- Impact of Revival: Just like health insurance, if the policy is revived after a lapse, the 3-year clock starts all over again.

Key Summary

| Feature | Health Insurance | Life Insurance |

| Moratorium Period | 5 Years | 3 Years |

| Contestability | Cannot contest PEDs / Non-disclosure | Cannot contest for any reason |

| Exceptions | Proven Fraud / Permanent Exclusions | None (Absolute after 3 years) |

| Impact of Revival | Resets 5-year clock | Resets 3-year clock |

Final Thoughts

The IRDAI has made the rules “Pro-Consumer,” but they are also giving insurers better tools (like the National Insurance Claims Registry) to spot fraudsters.

- For Health: Don’t hide anything. Even after 5 years, a “Fraud” tag can wipe out your entire safety net.

- For Life: The 3-year window is your ultimate protection, but don’t test it. The insurer has 3 years to investigate you thoroughly; if they find a lie during a death claim in Year 2, your family gets nothing.

The golden rule remains: It is better to pay a 15% higher premium today by disclosing a disease than to have a 100% claim rejection tomorrow.

Continue reading:

- LIC Policy Returns in 2026: How Much Do LIC Policies Really Return?

- Latest Health Insurance Incurred Claim Ratio 2025-26 | Top Health Insurance Companies List

(Post first published on : 15-April-2026)

Join our channels