Each one of us has financial needs and goals. Once the goals are identified, we need to set goal values (targets). This means that we should be in a position to convert the needs / goals into financial terms. To do this, we should be aware of and understand the most important aspect of ‘Financial Planning’ i.e., Time Value of Money (TVM).

Money has TIME value. A rupee today is more valuable than it will be a year hence or two years hence. Do you agree with me?

In this post let us understand the importance of Time value of money and basics of TVM.

Why Money Has Time Value

Suppose you were given the choice between receiving Rs 100,000 today or Rs 100,000 in 10 years. Which option would you rather select? Clearly the first option is more valuable for the following reasons:

- Purchasing power: Because of inflation, Rs 100,000 can be used to buy more goods and services today than Rs 100,000 in 10 years from now. Put another way, just think back to what Rs 100,000 could buy you 10 years ago. For example : 10 years back the cost of one litre milk would have been say Rs 5, now its Rs 30 and after 10 years, it could be Rs 100.

- Opportunity Cost: A rupee received today can be invested now to earn interest, this can result in a higher value in the future. Sooner is better than later.

- Risk Vs Return: If you are giving your money to be used by another person / company, that means you are taking the risk associated with it, which is known as ‘default risk’ (you may or may not get back your payments). So, you expect return / interest to compensate the risk.

Time Value of Money : Compounding & Discounting

The basic principles of TVM are compounding and discounting methods.

Compounding : When we hear the word ‘compounds’, the first thing that comes to mind is GROWTH. That means we expect our investment to grow and yield some return (or interest).

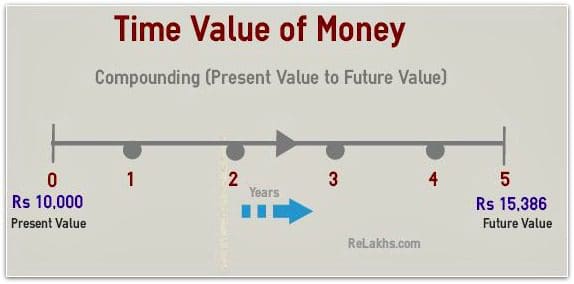

For example – Rs 10,000 invested today in a bank fixed deposit at 9% pa interest rate for 5 years can fetch you Rs 15,386 (let’s ignore taxation part). So Rs 5,386 is the accumulation of the interest and also interest on the interest.

Discounting : Compounding is about the future value of today’s investment, where as discounting is the today’ value (PV) of money to be received in the future (FV – Future Value). Present value is calculated by applying a discount rate (opportunity cost) to the sums of money to be received in the future.

For example – You want Rs 15,386 in five years from now and the prevailing bank rates are around 9%. What is the amount that you need to invest now to receive Rs 15,386 after five years?

The value of Rs 15,386 is equal to Rs 10,000 in today’s value at a discounting rate of 9%.

Five components of Time Value of Money

Based on the above examples, we can say that the components of any TVM problems or calculations are;

- Tenure (The total number of compounding or discounting periods)

- Rate of Interest

- Present Value (PV) or Today’s value

- Future Value (FV)

The fifth component is Periodic Payments (Pmt).

For example : If you acquire a home loan of Rs50 Lakh @ 10% pa for a period of 20 years, your EMI (Equated Monthly Installments) would be around Rs 48,000.

So, Payments (pmt) represents equal periodic payments received or paid each period. When payments are received they are positive, when payments are made they are negative.

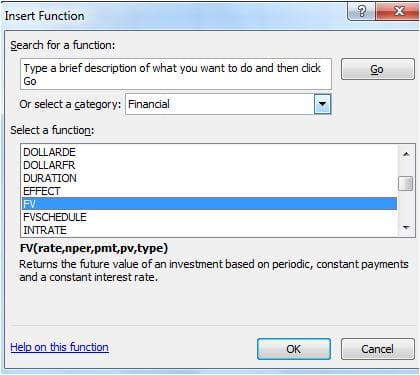

You can use Microsoft Excel to calculate TVM based problems. Use FV, PV, PMT etc., to calculate you financial goal amounts and also to analyze your investments.

You can also use regular or financial calculators to solve your Time Value of Money problems.

Kindly go through the below articles to understand the importance of TVM. I have used TVM calculations (using MS Excel functions) in these articles.

- Calculate Future Value of your Investments or Project Future Value of your expenses

- Retirement Planning in 3 easy steps

- Kid’s Education Goal Planning

- Calculate Home Loan EMI payments, total principal repayment / interest amount

- The importance of numeracy in becoming Financially Literate!

Next time, when your insurance agent / financial adviser says that you will receive Rs 50 Lakh when you retire, do not just blindly believe it and sign the proposal form, instead calculate the present value of the maturity benefit in today’s value 🙂

These Time Value of Money calculations demonstrate that time literally is money. The value of the money you have now is not the same as it will be in the future and vice verse. So, it is very important to know how to calculate the time value of money so that you can distinguish between the worth of investments that offer you returns at different times.

Time is money – Benjamin Franklin

Time is money – Benjamin Franklin

Continue reading :

- The importance of numeracy in becoming Financially Literate!

- Investment Planning : How to calculate the Future Value of investments using MS Excel

- Personal Financial Calculators – Tools to manage your Finances more easily!

(Image courtesy of Stuart Miles at FreeDigitalPhotos.net)

Join our channels

cyber security

Time Value of Money : Importance & Examples

Can you describe the formulaes made to find out the pv and fv without going to the excel????

Dear Suchismita ..You may kindly visit Wiki page for this, very well explained..click here to read..

Hi Sreekanth sir. I found your blog useful. Actually I’m a 1st year student of BBA LLB. So, i was trying to find out some numericals based on discounting technique and compounding technique for calculating annuity and present value. If you colud help me provide some numericals plzz mail it to me.

thank you.

Dear Raghav..You may buy books on ‘Financial management’ (or) ‘financial planning – a ready reckoner’ by Madhu Sinha.

Thank you for sharing the article. It’s very useful. Hope to hear more from you.

Keep visiting dear Erick 🙂

Hi Sreekanth Reddy,

Very nicely witten article, I love your blog.

You always right very useful and informative articles, keep writing.

Thanks for sharing.

Thank you dear Pannkaj..Keep visiting 🙂

Check out the Tata aia life’s money back insurance plan.The plan gives you the flexibility to choose from various term options to meet your financial commitments with the advantage of paying for only half the term.

Dear Dhananjaya,

What is the expected return on this plan? Did you calculate it?

It is advisable to avoid money-back plans.

Read my review on LIC New money back plans – Reveiw on Returns calculation.

Hi Sreekanth Reddy,

Very well written article, thanks for the information and keep writing such amazing articles.

I am great fan of your blog, thanks.

Thank you Akash..keep visiting 🙂